The Timing of the Occidental-Berkshire Hathaway Deal Wasn’t Random

Here's what opened the door for a cash-rich firm to negotiate a stellar deal to acquire distressed assets.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Commodity producers have been put into a vice. Their input costs have soared while most commodity prices have been under significant price pressure due to oversupply and slack demand. As is par for the course, the energy sector is at the top of the list of those in misery.

As I mentioned on the Schwab Network earlier last week, it wasn’t a coincidence that Occidental Petroleum (OXY) opted to sell its chemical division to Berkshire Hathaway (BRK.A) (BRK.B) at this moment (click here to see the clip).

Commodity traders receive margin calls issued by their brokerage, requiring them to liquidate holdings to de-lever and lessen risk, particularly ahead of a perceived risk event. On the other hand, when commodity producers overextend themselves, they receive what is essentially a margin call in the form of pressure from banks and shareholders to de-risk. In short, Occidental experienced a friendly margin call from investors and lenders, enticing them to streamline operations and improve their balance sheet.

Why Now?

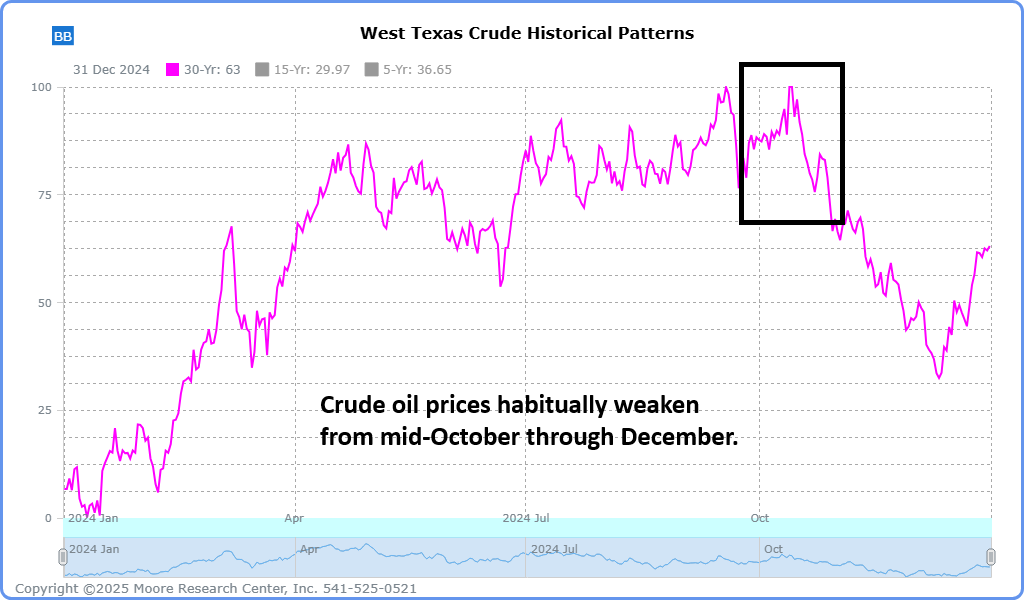

This isn’t Occidental’s first rodeo. They know the price of crude oil often experiences sharp seasonal weakness from mid-October through the remainder of the year.

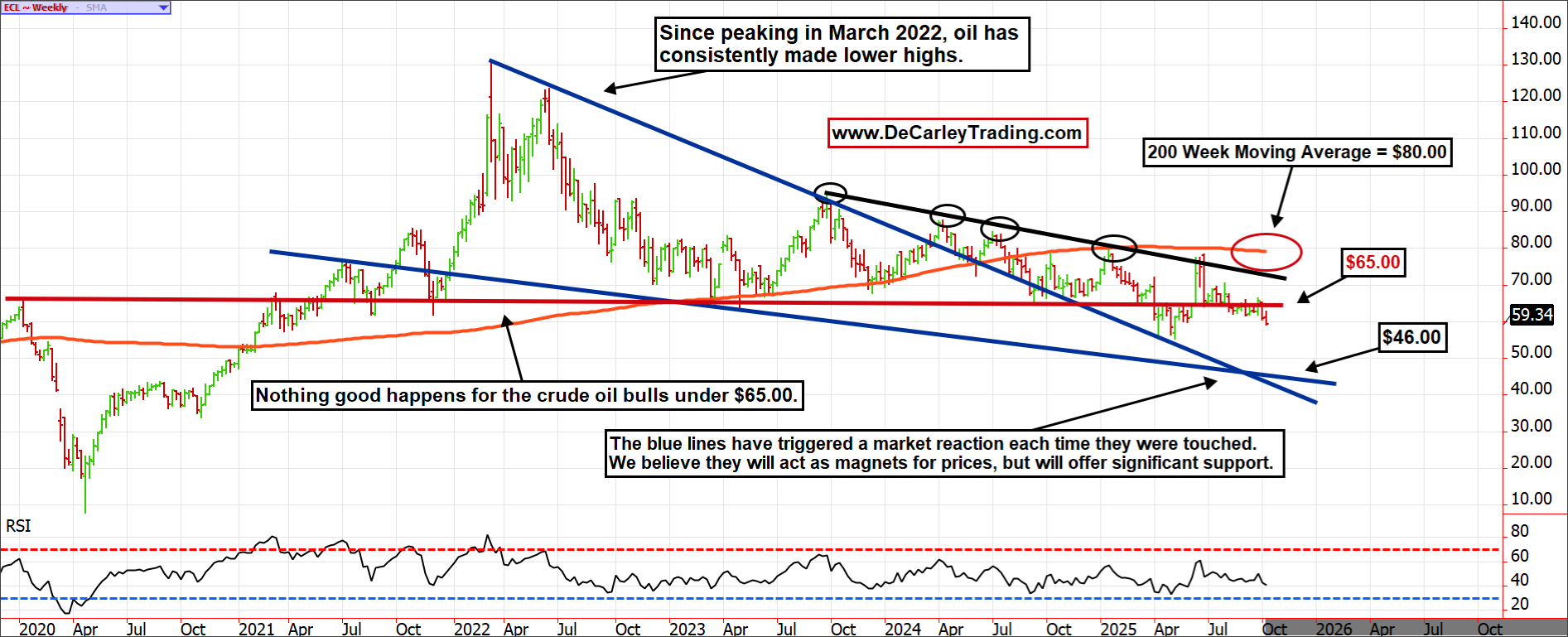

The brainpower of Occidental also recognizes that the crude oil market has entered what has historically been a slippery slope. Over the past two decades, when oil has fallen below $65.00 per barrel, selling has triggered further selling, until reaching a $30.00 handle or even lower, as seen during the pandemic energy market crash.

U.S. shale producers face a cost of production of roughly $65.00 per barrel for newly drilled wells; thus, this price has behaved as a significant historical pivot point in the oil market. However, the breakeven point for most OPEC producers is much lower; new wells are probably near $40.00, and existing wells are $15.00 or below — some might even be well under $10. Thus, there is no incentive for OPEC to cut production under $65.00. In fact, they have historically increased production in such a scenario to ensure they maintain, or even increase, their market share.

The monthly chart of crude oil futures, above, simplifies analysis; the market is bullish above $65.00 and bearish below. Throughout the last 25 years, oil has only spent a lasting time below $65.00 on three other occasions: the global financial crisis, the 2016 commodity bear market, and the pandemic. The price action suggests that the fourth washout could be in play. Will there be a significant historical event accompanying it, similar to 2008 and 2020? Or will it just be a good old-fashioned bear market like in 2016?

Since the euphoric high in oil prices in 2022, the market has been perpetually bearish. We have witnessed several rallies in the last two years occurring over Middle East violence, but each of those has proven temporary. Even so, we estimate that $5.00 to $10.00 per barrel in risk premium has been priced into the market to account for the ongoing conflict between Israel and Hamas. If Monday’s peace deal proceeds as expected, it will be difficult for oil to maintain its composure.

Using the weekly oil chart, above, we can gain a better understanding of how pivotal $65.00 has been in recent years (red line in the center of the chart). The RSI (Relative Strength Index) is far from being oversold on the weekly or monthly charts. Accordingly, we believe the next significant pivot price, near $46.00, will act as a magnet.

If Occidental Petroleum’s financial health was distressed by $65.00 oil, they would be desperate in the $40.00s or lower. This opened the door for a cash-rich firm like Berkshire Hathaway to negotiate a stellar deal to acquire distressed assets.

For those wondering why Berkshire would buy an asset that relies on a commodity that seems prime for a haircut, they aren’t running the same race. While most are running a 50-yard dash, Berkshire is slow jogging a marathon.

We view the buyout of Occidental’s chemical operations by Berkshire as a win-win; it reduces OXY’s risk and allows it to streamline its operations.

As a small business owner, I can attest that it is better to attempt to excel at a few products or services rather than trying to do it all at a mediocre quality. If we want to compete with OPEC's low production costs, we will need to see more of this.