The Sector Most Vulnerable to Higher Energy Prices Is Ignoring Higher Energy Prices

As this sector runs into resistance, here's what I think will happen.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

US-STOCKS-MARKETS-OPEN

US-STOCKS-MARKETS-OPEN

Monday, I was amazed that so many strategists were lowering all the inputs one could use to calculate the year-end S&P target, and yet they refused to take their S&P targets lower. Then on Tuesday, one of the Wall Street firms added to my amazement when they not only did not lower their S&P target for this year, they raised it!

I suppose part of it is because no one has lowered their earnings for the year, and until earnings are lowered—if they are lowered—we are unlikely to see any action on that front.

Tuesday saw the 493/Russell 2000 outperform again. As I have noted, the put/call ratio for the Russell 2000 in the first few weeks of March was so high almost daily that I believe this is the unwind of that.

While many will opt to focus on the IWM to the S&P chart, most of you know that lately I prefer the chart of the S&P to Nasdaq. I believe it captures where folks are in terms of preferring growth over value. As long as this blue line remains intact, folks will prefer value. Should the ratio fail to get up and over those late February highs, I would say that’s a change, but for now, we can see the preference.

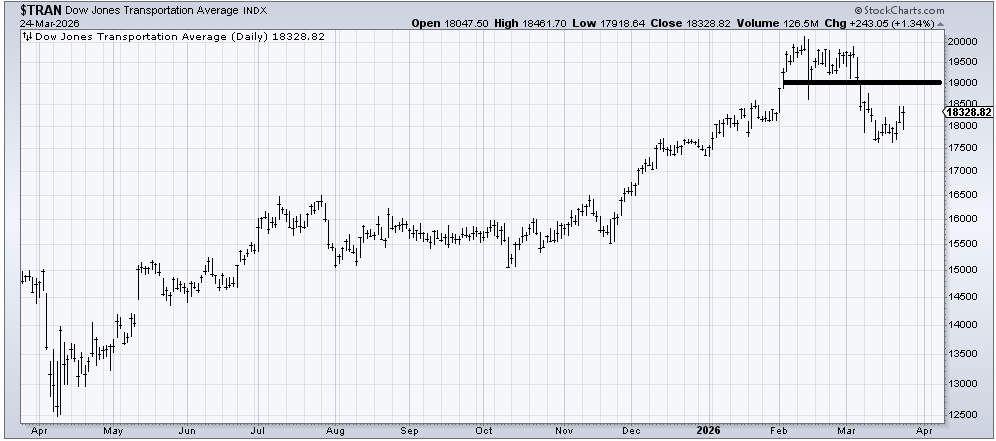

The market is being pushed around by headlines about the war in the Middle East, but under the surface, we find that the Transports, as I noted two days ago, were up on the week last week. Now I can report that they have been up six of the last eight trading days. In fact, they are trading where they were on March 6th, which was one week into the war. So the group most vulnerable to higher energy prices is currently ignoring the higher energy prices.

I expect resistance in that 19000 area.

On the sentiment front, Tuesday’s retreat in the big cap indexes pushed the S&P’s Daily Sentiment Index (DSI) back down to 24 (it was 22 after Friday), and Nasdaq’s is down to 26 (it was 25 after Friday). With the market still not yet short-term overbought, I would expect another rally this week, and these DSI readings ought to lift along with said rally. We’ll see where they are after a lift (if we get the lift I expect)

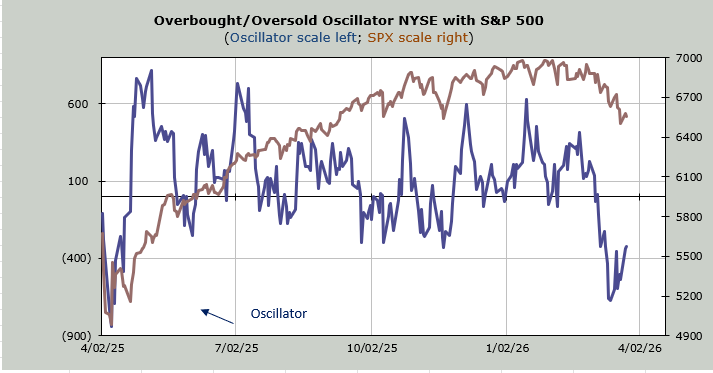

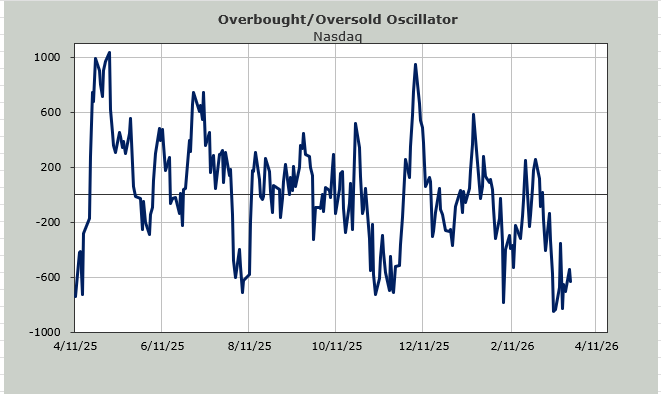

You can see the Overbought/Oversold Oscillator is still well below the zero line. The next three trading days, this ten-day moving average will drop red numbers. After that, we go back to some red, some green/black, so the window is open until Friday.

I want to end with a comment on Gold. I have not been a fan of the yellow metal since January. I am still not a fan. However, it is getting very oversold, and it has some support in this 400 area on GLD. The DSI got to 15 on Monday, so I think it’s due a bounce.

Related: The Biggest Trading Mistake You Can Make in This Difficult Market