The Party at Wall Street

Let's revel in the rally, revisit the CPI, request some rate-cut commonsense, and recheck the Meta chart.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Rock! Rock! (Till You Drop)

Hold on to your hat, hold on to your heart

Ready, get set to tear this place apart

Don't need a ticket, only place in town

Anything goes!

Anything goes!

- Lange, Clark, Allen, Savage, Elliott, Willis (Def Leppard), 1983

Tuesday

Equity markets roared on Tuesday. Markets were pushed on by a July consumer price index report that while somewhat inflationary at the core on an annual basis and a little hot in services as well, was lacking in evidence that tariffs were having much of an impact on consumer prices. We covered this in a featured piece at The Street Pro late Tuesday morning, so I'll try not to bore regular readers too much. The gist of the story was this: Core July CPI hit the tape at growth of 3.1%, a bit warmer than the 3% growth we were looking for, but headline CPI printed at growth of 2.7%, which was below the 2.8% professional consensus.

Areas where tariffs would have been expected to have pushed prices higher, for the most part, did just the opposite. Apparel prices were actually lower on a month-over-month basis, across nearly all demographics. Appliances, to include major appliances and items categorized under the "home decor" category, were lower as well. Not part of core inflation and not impacted by tariffs, so adjacent to the story, both food and energy prices were also overtly weak in July.

This is why traders were able to place bets on a Fed rate cut in September. Yields dropped at the short end of the Treasury curve, stocks soared and Fed Funds futures trading Chicago heated up with excitement. In my piece on Tuesday, I explained the math behind why I feel that the target range for the Fed Funds rate might be something close to full percentage point too high. Apparently, I have allies in high places....

Bessent Speaks

After the report, Pres. Trump criticized the Fed's lack of action on interest rate policy. This has happened often and is not unexpected when it happens. Fed Chair Powell has been resistant to reducing short-term interest rates despite that had he been "data-dependent," I believe, rates would have been reduced earlier this year. This has forced the slope of the Treasury yield curve to take on an unnatural shape that drags on both credit creation and economic activity.

The more potent words were spoken later on Tuesday, by Treasury Sec. Scott Bessent, who is very highly respected both inside the administration and across business and economic circles. Appearing on the Fox Business Network, Bessent said, "Everyone was expecting that there would -- as you said -- that there would be goods inflation, but there was actually this very odd service inflation." Bessent also commented that the Fed "could have been cutting in June, July" had the Bureau of Labor Statistics been more accurate in their methods for data collection and reporting. (I'd argue the the Fed should have been cutting....)

I think the most important thing that Bessent said during the interview was this: "The real thing now to think about is should we get a 50-basis point rate cut in September." As readers know, I think the Fed is about 100-basis points behind. My opinion is worthless on the matter. Jerome Powell's opinion is the one that matters, at least for now, and he will have the perfect opportunity to set up a September rate cut late next week from Jackson Hole, Wyoming. The theme of this year's symposium is "Labor Markets in Transition." Given recent developments at the Bureau of Labor Statistics, that gives him an easy way to deflect some blame for his inaction on policy.

Fed Funds Futures

Glancing at Fed Funds Futures markets trading in Chicago on Wednesday morning, a 96% probability for a quarter-percentage point rate cut is now being priced in for Sept. 17, up from 92% late Tuesday morning and 82% just ahead of Tuesday's release. A 64% likelihood is now being priced in for a second quarter-point rate cut on Oct. 29, up from 61% late Tuesday morning and up from 53% ahead of the CPI.

There is now a 53% probability being priced in for a third quarter point rate cut in calendar year 2025, up from 50% late Tuesday morning and up from 42% ahead of the July CPI release. These markets are also pricing in a half-point worth of additional rate cuts for 2026 at this time.

Marketplace

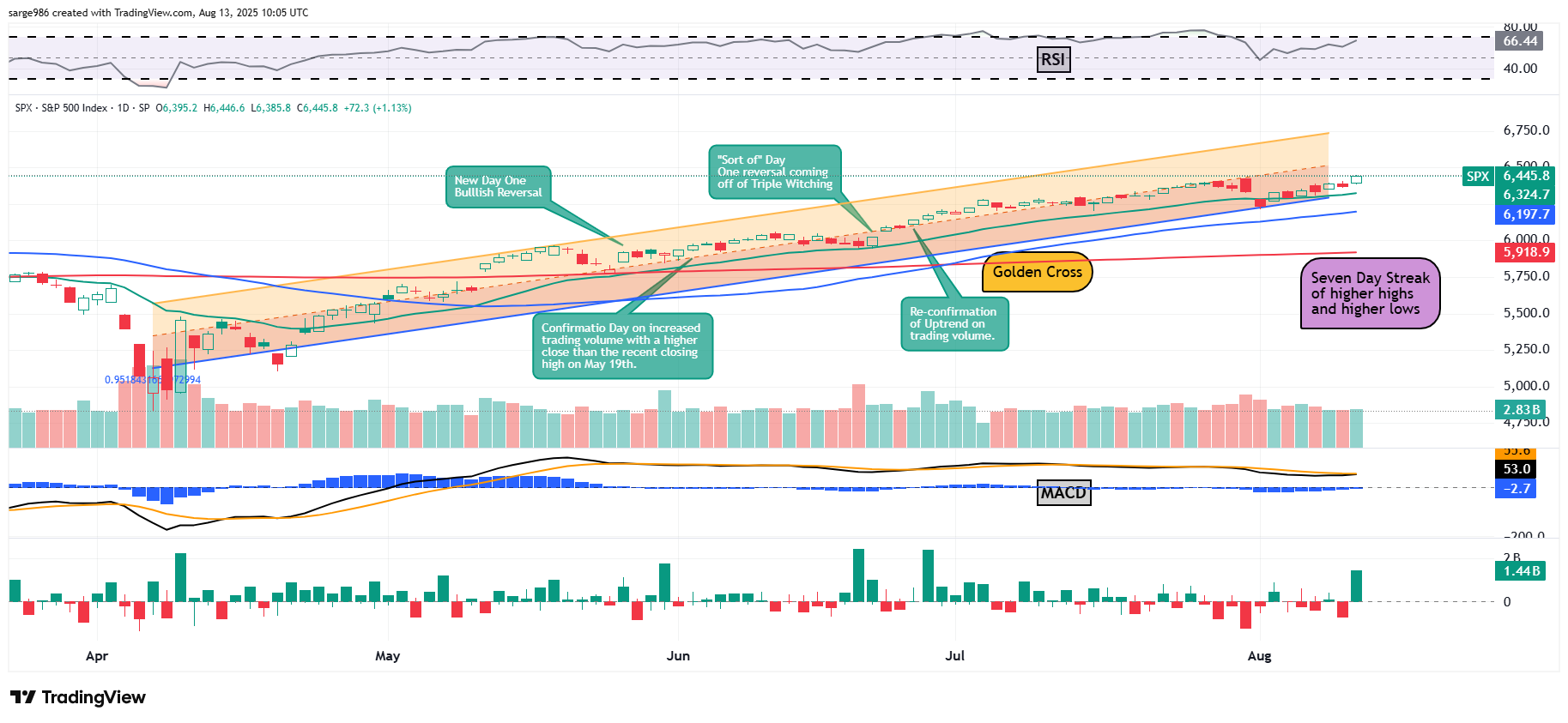

The Tuesday rally was quite broad and I must admit, very exciting. It's been a while since I had that much fun simply doing my job. I guess that's how baseball players feel. Ah... maybe not. The S&P 500 gained 1.13% for the session, closing at a new all-time record high and scoring a higher high and a higher low for a seventh consecutive trading session. Those same things can be said about the Nasdaq Composite after that index tacked on a cool 1.39%.

You know what's good for economic growth? Lower short-term interest rates. You know what groups of stocks react more than visibly to improved prospects for economic growth? That's right, the transports and the small caps. On that note, the Dow Transports screamed 2.99% higher on Tuesday, as did the Russell 2000. The transports were led by the airlines, as American Airlines AAL ran 12% followed by a 10% gain by United Airlines UAL.

Beyond those groups, the Philadelphia Semiconductor Index also popped for a 2.99% gain, led by NXP Semiconductor NXPI and ON Semiconductor ON. That's right. three of our mid-major indices gained exactly 2.99% for the day. Just an FYI... That's almost statistically impossible to do. The KBW Banks also gained 2.54%.

Breadth

Al 11 S&P sector SPDR ETFs closed out the Tuesday session in the green. Growth sectors led the way with Communication Services XLC on top followed by Technology XLK. Not surprisingly, the three bottom slots on the daily performance tables were occupied by defensive sectors with the REITs XLRE, still up on the day, in last place.

Winners beat losers by more than 4 to 1 at the NYSE and by more than 5 to 2 at the Nasdaq on Tuesday. Advancing volume took a 78.5% share of composite NYSE-listed trade and a 78.1% share of composite Nasdaq-listed activity. So, did we confirm anything on Tuesday? Close, but not really. We'll have to take what we can get. Aggregate trading volume was higher on a day over day basis across NYSE-listings and across the membership of the S&P 500. However, volume ebbed just a bit across Nasdaq-listed securities, so it was not an all-green sweep on broadly expressed higher volume. There is something I want to show you though. take a look at this...

The Chart

This is the same chart that I usually update for you on Monday mornings. Readers will see that within the daily Moving Average Convergence Divergence, the 12-day exponential moving average is very close to crossing over the 26-day EMA. That would be a bullish signal. The histogram of the 9-day EMA is not quite there yet, but it is getting close to reaching the "zero-bound." That would be bullish as well.

Now, I added what we call a "Volume Delta" indicator at the bottom of the chart. This is not an indicator that I attach to every chart, but it is in my tool kit. Volume Delta uses intra-bar volume and price fluctuations to estimate the gap between upward and downward pressure within the time frame of the candle, which on this chart is a full day. Take a look at Tuesday's Volume Delta. Tuesday sent the strongest positive signal since June 25th. The S&P 500, just as an FYI, is up 5.8% since the closing bell on June 25th.

Antoni to BLS

On Monday, Pres. Trump announced that he would nominate EJ Antoni, chief economist at the Heritage Foundation to head the BLS. In an interview at Fox News Digital, Antoni said, "Until it is corrected, the BLS should suspend issuing the monthly jobs reports but keep publishing the more accurate, though less timely quarterly data." Antoni added, "Major decision makers from Wall Street to DC rely on these numbers, and a lack of confidence in the data has far-reaching consequences."

Finally, someone potentially in a position of authority has said exactly what I have been encouraging since the summer of 2022. Readers will recall that back in mid-2022, the ADP Employment Report had gotten rather wonky.

ADP had the temerity and decency to take its model off line for several months until it had regained confidence in its ability to report accurate data. At the time and several times since, I have encouraged the BLS to do the same as it had become quite obvious that the agency's methods for data collection had become antiquated and that their adjustments for seasonality and birth / death modeling had become no better than wild guesses.

Question?

Is Meta Platforms META still breaking out from the Cup With Handle pattern that developed this past winter into spring, or is the stock developing a Rising Wedge pattern of bearish reversal?

Good question. I haven't decided. I'd be slow to buy it here, unless it cracks that upper trendline though.

Economics

(All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.77%.

07:00 - MBA Mortgage Applications (Weekly): Last 3.1% w/w.

10:30 - Oil Inventories (Weekly): Last -3.029M.

10:30 - Gasoline Stocks (Weekly): Last -1.323M.

The Fed

(All Times Eastern)

08:00 - Speaker: Richmond Fed Pres. Tom Barkin.

1:00 p.m. - Speaker: Chicago Fed Pres. Austan Goolsbee.

1:30 - Speaker: Atlanta Fed Pres. Raphael Bostic.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: EAT (2.47)

After the Close: CSCO (.98)

At the time of publication,, Guilfoyle was long CSCO equity.