The Market's Wildcard Is Now in Play

We now know what financial markets had been struggling to price in: war with Iran. Let's tackle the latest news and brace for what's to come.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Good morning. Let's get to work. Zero dark-thirty. Asian stock markets opened and traded lower. European markets just opened lower as well. U.S. equity index futures are also trading sharply lower. At least now we know precisely, without speculation, what financial markets had been struggling to price in, on top of AI-focused industry-wide disruptions, over the past three-plus weeks. We knew that a strike on Iran was likely. I think the scale is probably a surprise.

U.S. Treasury debt securities remain strong. The U.S. Ten-Year Note pays a rough 3.97% as the wee hours roll by, after topping out around 3.93%. The U.S. Dollar Index has benefited to a degree from its reserve currency / safe haven status. Gold and silver have rallied as well as investors seek haven as well, despite that stronger dollar. Bitcoin looks like it does not know what to do.

In addition, crude oil has rallied sharply, which may seem counterintuitive as the U.S. dollar strengthens, as it does appear that both production and transport will suffer. The advent of this war also takes inexpensive / semi-illegal Iranian oil out of circulation. While that provides an upside catalyst for energy prices, this will both slow Chinese economic activity while putting a crimp in Russia's military aggression in eastern Europe.

Latest Headlines

- The armed forces of the U.S. and Israel have now struck more than 2,000 targets in Iran, causing widespread military and government-focused damage, taking out multiple levels of regime leadership.

- Iran's military has launched a broad, but somewhat chaotic and mostly ineffective response.

- Iran's security chief says that Iran "will not negotiate" with the U.S.

- U.S. Secretary of War / Defense Pete Hegseth will hold an 8 a.m. press conference this (Monday) morning.

- At least one, and likely more U.S. aircraft were destroyed in Kuwait (no casualties in that event), according to CENTCOM.

- Saudi oil refinery at Ras Tanura has halted operations after a suicide drone attack.

- Israeli armed forces have simultaneously launched an offensive against Hezbollah in Lebanon.

Focus Now ...

Maintain a level head. The situation in the Middle East is and will remain fluid for quite some time. Pres. Trump has addressed the U.S. public more than once now to brace the people for what is to come. Three U.S. servicemen are already confirmed to have been killed in action with five others possibly seriously wounded. The president has inferred that offensive operations in the region could continue for as long as four to five weeks or until the mission's objectives are achieved. Rumor has it (no confirmation that I can find) that a new supreme leader had been named overnight in Iran and U.S. or Israeli forces had already killed that individual.

As we head toward the opening bells down at 11 Wall St. and up at Times Square, I would think that in addition to the U.S. dollar itself and U.S. Treasuries, that the stocks of Energy companies and defense contractors will be most likely to experience an increased level of volatility. Analysts at Wells Fargo (WFC) wrote "In the event of prolonged Hormuz closure and an oil shock to $100+ per barrel, we forecast 6,000 (-12.8%) on the S&P 500 as the worst-case scenario" Analysts at Goldman Sachs (GS) added "In equities, the impact of a risk and growth shock is clearly negative, but only a severe and sustained oil price disruption would have large effects on the global growth picture."

"And the rocket's red glare, the bombs bursting in air

Gave proof through the night that our flag was still there."

- Francis Scott key, 1814

... For those unaware or maybe just don't care, that flag, our beautiful flag, the same one that brings a tear to your eye every single time you come to attention and snap your very sharpest salute, is still there and always will be. Always Faithful.

Key U.S. Munitions Being Deployed Offensively

- GBU-57A/B Massive Ordnance Penetrator (30K pound bunker busters)... is a Boeing (BA) product delivered via the B-2 Spirit Bomber, which is a Northrop Grumman (NOC) designed aircraft.

- Tomahawk Land Attack Missiles (TLAM)... is produced by RTX Corp (RTX) , formerly known as Raytheon Technologies.

- LUCAS "One-Way" Attack Drones... is designed by SpektreWorks and is a reverse-engineered clone of Iran's very similar Shahed-136. This is a very low cost ($3K per) method for delivery.

- Precision Strike Missile (PrSM)... This "next-generation" long-range SAM (surface to air) missile is designed and produced by Lockheed Martin (LMT) .

- AGM-158 JASSM/JASSM-ER ... This family of stealth long-range cruise missiles is also primarily a product of Lockheed Martin and can be delivered via B1B and B-52H bomber aircraft as well as via F-15E, F-16, F/A-18 and F-35 Lightning fighter aircraft. The B-1B (Boeing) has been retired and will be replaced by the B-21 (Northrop). The B-52H is primarily a Boeing craft. The F-15H and F/A-18 are Boeing products. The F-16 and F-35 are manufactured primarily by Lockheed.

- HIMARS (High Mobility Artillery Rocket System) ... Five-ton truck mounted with a lightweight rocket launcher designed by Lockheed Martin.

Key U.S. Munitions Being Deployed Defensively

- Patriot (MIM-104) Interceptors... Primary US mobile surface to air, anti-ballistic missile system, developed by RTX Corp.

- THAAD (Terminal High Altitude Area Defense)... Mobile, rapidly deployable unit unique for its ability to neutralize threats both inside and outside the Earth's atmosphere designed by Lockheed.

- Standard Missile (SM-2/3/6)... Cornerstone of the US Navy's on-board anti-air and missile capabilities, designed by RTX Corp.

The Week That Was...

As U.S. financial markets focused on AI disruption ahead of the hostilities that began this weekend...

- The S&P 500 gave up 0.43% on Friday and just 0.44% for the week.

- The Nasdaq Composite lost 0.92% on Friday, and 0.95% for the week.

- The Nasdaq 100 gave back just 0.3% on Friday and just 0.21% for the week.

- The Russell 2000 surrendered 1.68% on Friday but gained 0.65% for the week.

- The S&P Small Cap 600 added 0.53% on Friday and 1.18% for the week.

- The S&P Midcap 400 gave up 0.81% on Friday and 0.88% for the week.

- The Dow Transports lost just 0.23% on Friday and 0.77% for the week.

- The Philly Semis backed up 1.21% on Friday and lost 1.96% for the week.

- The KBW Bank Index was punished for a loss of 4.85% on Friday and 5.91% for the week.

On Friday, surprisingly, eight of the eleven S&P sector SPDR ETFs closed out the session in the green, led by Health Care (XLV) as defensive sectors outperformed the broader marketplace. The Financials (XLF) and Technology (XLK) suffered the brunt of the selloff.

For the week, seven of the 11 S&P sector SPDR ETFs traded higher, with defensive sectors taking the top three slots on the weekly performance table, led by the Utilities (XLU) . Again, he Financials and Technology took the largest losses.

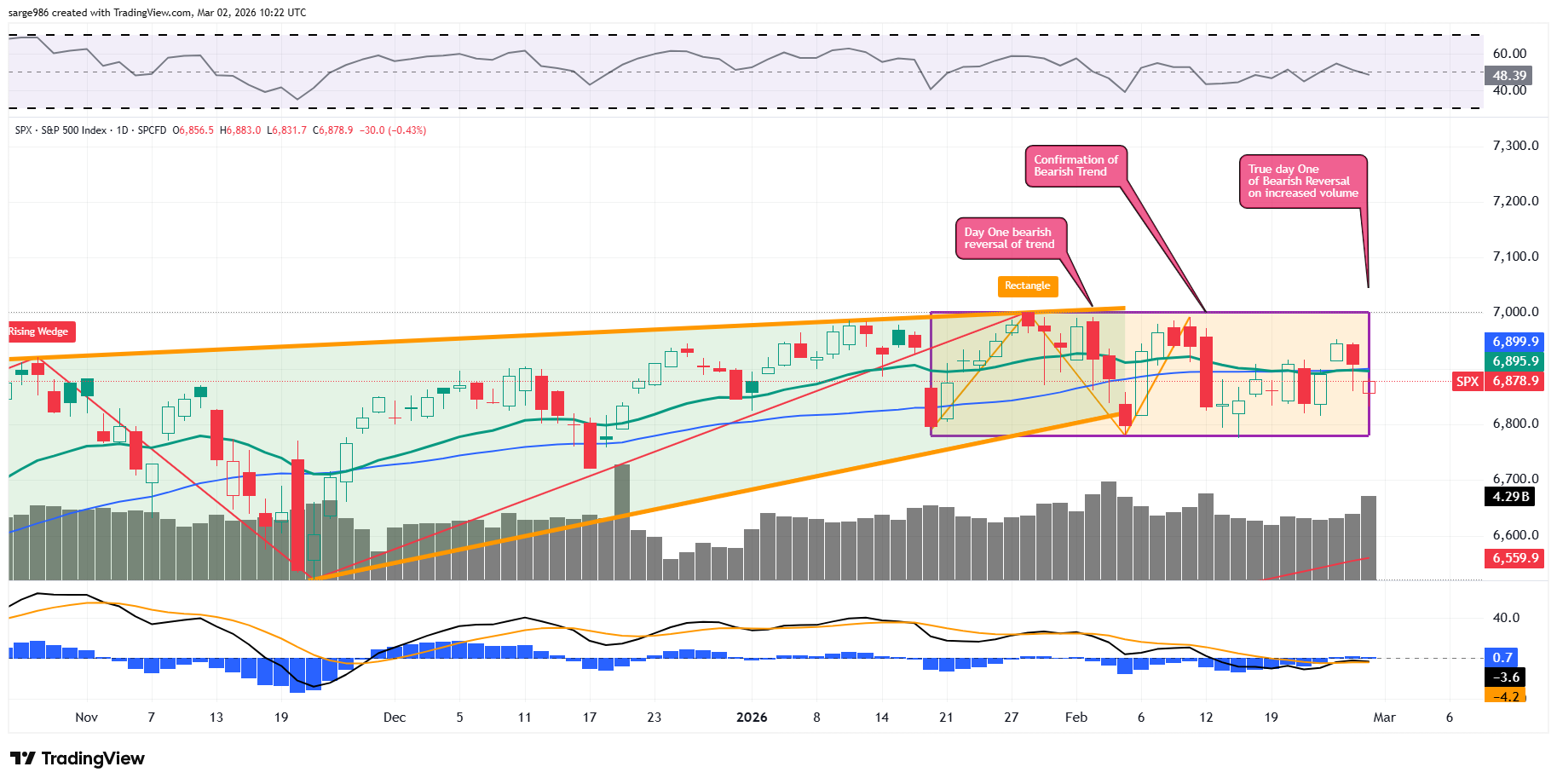

The Chart

Readers will see the Rising Wedge Pattern of bearish reversal that we showed you last week led into a basing period or rectangle of consolidation. Though it is quite clear that on Friday, the S&P 500 suffered a Day One Reversal of Trend to the downside (though it was the second day of the sell-off). This action was punctuated by the increase in trading volume.

The index gave up both its 21-day exponential moving average and 50-day simple moving average on Friday and lost contact with both lines as well. This is adding to the technical weakness seen across U.S. stock markets on Monday morning. Neither Relative Strength nor the daily moving average convergence divergence showed an overt increase in bearish signaling on Friday. That will change this morning.

Earnings

As of Feb. 27, according to FactSet, for the fourth quarter, Wall St. sees a year-over-year blended (results and projections) earnings growth for the S&P 500 of 14.2%, up from 13.2% two week ago and up sharply from 8.2% just a few weeks prior. Wall St. also sees revenue growth of 9.4%, up from 8.2% several weeks ago. Simply put, as mentioned here for weeks now, despite the recent stock market volatility, corporate execution has been beyond excellent.

With 96% of the S&P 500 having reported, 73% of S&P 500 member firms have reported earnings beats while a like 73% have beaten consensus for revenue generation. For the full year (2025), the street now sees earnings growth of 13.6% on revenue growth of 7.7%. For the full year 2026, the street looks for earnings growth of 14.7% on revenue growth of 7.7%.

At the moment, technology, at earnings growth of 33.4% and the industrials at growth of 26.7% as well as communication services (+13.1%) are the only sectors projected to experience double-digit bottom-line growth for the fourth quarter. Presently, no sectors are projected to suffer a year over year earnings contraction as both Energy and the Discretionaries have moved into the win column in recent weeks.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 21.6-times twelve months' forward-looking earnings, up from 21.5-times two weeks prior. This is well above the five-year average of 20.0 times for the index as well as well above its 10-year average of 18.8 times.

The S&P 500 also ended last week trading at 27.8-times trailing 12 months' earnings, down from 28-times two weeks back. That also stands well above the five-year (24.9-times) and 10-year (23.1-times) averages for the index.

Ten of the 11 sectors are now trading above their five-year average valuations, led by consumer discretionaries (27.3-times), the industrials (26.5-times) and tech (24-times). Only the REITs (at 18.6 times) are not historically overvalued relative to their five-year averages. The utilities escaped this distinction just last week.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in a 5% probability for a quarter point rate cut at the next Federal Open Market Committee policy meeting on March 18, up from 4% a week ago. The next rate cut is priced in for July 29 at this point (68% likelihood, down from 69% a week ago). At present, there is still a half point worth of additional rate cuts fully priced in (75% chance, up from 72%) for all of calendar 2026.

On The Docket...

This will likely be a highly volatile week for U.S. financial markets....

.... First and foremost, the military activity in the Middle East continues to expand. What's left of the regime in Iran is attempting to respond with great volumes of fire at U.S. and allied military bases as well as population centers in the region. While Israel has easily attracted much of Iran's return fire, Gulf nations friendly to the U.S. have also been targeted.

.... Our central bankers will not be very active early this week. While the Federal Reserve will release its Beige Book this Wednesday afternoon, I only have three fed speakers on my radar for the week. That said, all three, New York, John Williams, Cleveland's Beth Hammack and Neel Kashkari of Indianapolis all hold policy voting rights for 2026.

.... The macroeconomic calendar will be hot and get hotter as the week progresses. This is February jobs week, and Friday will be February jobs day. In addition, Friday will be January Retail Sales Day.

.... The earnings calendar will slow down a bit this week. That said, there will be a few headliners that will post their quarterly financial results this week. Tuesday leads things off when AutoZone (AZO) , Best Buy (BBY) , Target (TGT) and CrowdStrike (CRWD) all report. We'll hear from Broadcom (AVGO) on Wednesday evening, followed by Kroger (KR) , Costco (COST) and Marvell Technology (MRVL) on Thursday.

Economics

(All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Feb-F): Flashed 51.2.

10:00 - ISM Manufacturing Index (Feb): Expecting 52.3, Last 52.6.

The Fed

(All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long RTX, CRWD equity.