The Market's Not Done Correcting Yet: Here's What Investors Should Do Now

If my recession thesis proves accurate, the Dow could decline another 21% from here. It's time to sharpen your pencil.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

With the Dow tracking close to my initial downside projections, here's an update on my overall market views.

Back on March 10, in my article "How Low Can the Dow Go? Let's Forecast the Dow's Downside," I shared my downside scenarios for the Dow Jones Industrial Average. At the time, the Dow was trading at 41,904. Based on a detailed analysis, I projected a normal correction would take the index down to 36,592. What happened? The Dow dropped to 37,645 — within just 2.8% of that target.

That was the “normal correction” case. But I also outlined a deeper recession-driven target of 31,281. Based on current economic data, that more severe scenario is now coming into view.

The latest GDPNow forecast is showing a -2% contraction in Q1 GDP. While it takes two consecutive negative quarters to formally declare a recession, markets typically peak well before an official announcement — and bottom *before or right around* that confirmation.

If the recession thesis proves accurate, the Dow could fall from its recent level of around 39,657 to 31,281 — a decline of another 21% from here.

What That Means for Your Portfolio

Now is the time to reassess your equity exposure. If you’re 50% in stocks and the market falls another 21%, that translates into a 10.5% hit from here — assuming your portfolio mirrors market volatility.

Reassess your risk tolerance. Do you have enough dry powder? Do you have too much invested in stocks at nose-bleed valuations?

This is when investors should sharpen their pencils and start identifying companies that make economic sense in this environment. Fear tends to overshoot. That’s when smart capital goes to work.

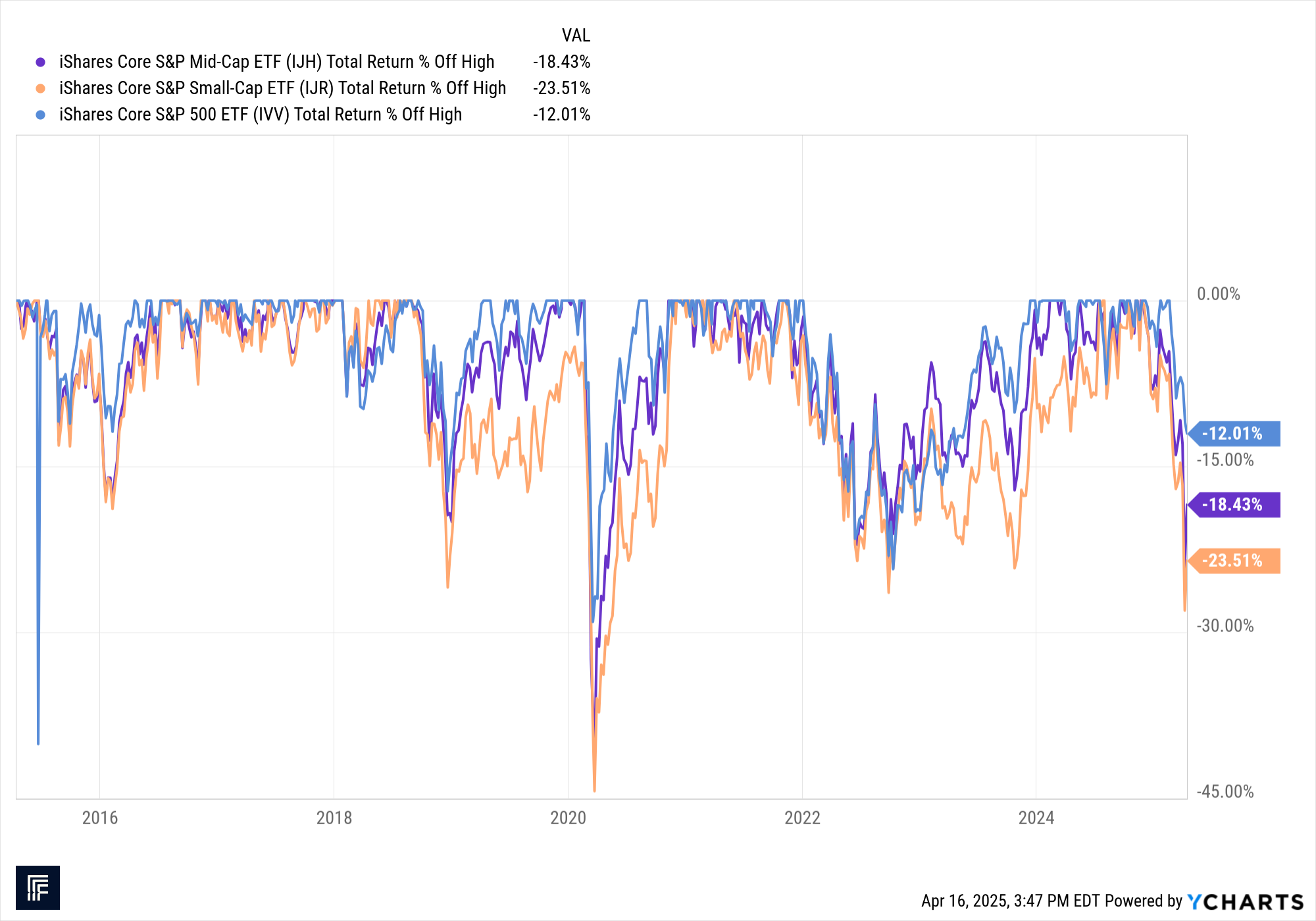

Large-Caps Are Still Lagging the Selloff

Not all parts of the market have corrected equally. The S&P 500 is down just 12% from its peak. By contrast, the iShares Core S&P Small-Cap ETF IJR is down 23.51% and the S&P Mid-Cap 400 Index is down 18.43% from their respective peaks.

Large-caps — many of which are still richly valued — haven’t broken down the way small- and mid-caps have. This is normal because smaller companies tend to be more volatile. These big names are often the last to fall, and their outsized weight in indexes can drag markets sharply lower once they crack.

The Indexing Dilemma

There’s another structural issue at play: the widespread reliance on indexing. 401(k)s, 403(b)s, IRAs, and government retirement plans funnel massive amounts of money into market-cap weighted strategies. That’s created distortions.

Indexing works well in efficient markets. But when valuations get stretched, these flows become blind to risk. Investors are buying more of what’s expensive — just because it’s big. That’s not investing. That’s autopilot.

If we hit a real downturn, passive investors could lose faith, triggering a feedback loop of selling.

What to Do Now

If you’re managing your money well, you probably own some solid companies already. But major market dislocations offer the chance to trade good for great. This is when you want to buy quality businesses at prices that will look like bargains in hindsight. In market corrections you could upgrade your portfolio into higher quality names at good prices and possibly have great performance over time.

Remember: Investing is about owning pieces of real businesses. Focus on fundamentals — cash flows, growth rates, durable competitive advantages. Be diversified, but not overdiversified. Keep some dry powder ready. And while it makes sense to hold some fixed income, be cautious on long-duration bonds given the macro backdrop.

We may see the Fed cut rates, but long-term yields might not follow. Fiscal deficits, debt refinancing, and a steepening yield curve could all limit upside for long bonds.

Final Thought

Just before I wrote this today, a client who's wife is about to retire called me. While we were on the phone, he said, “The market’s down over 2% today, but my portfolio is barely down. That gives me comfort.”

That’s what proper positioning hopefully can look like. If your portfolio isn’t aligned with your risk profile, it might be time to rethink your allocation.

Let me know your thoughts — and follow me on X (Twitter) @louisllanes for more updates as this unfolds.