The Market Gets a One-Two Punch; I Get More AMD

Let's check the hit from the ISM numbers -- ouch -- and the India tariffs; also, I chart the market, look at the Fed Chair ... options ... and Advanced Micro Devices.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Financial markets started out strong enough on Tuesday morning. Then came the selloff, followed by a little bit of a rotation out of growth and into smaller cap stocks. Catalysts? There were a couple. For one, the ISM Non-Manufacturing or "Services" PMI for July disappointed. The headline print hit the tape at a barely expansionary 50.1. Remember, the ISM Manufacturing survey for July had already printed in a state of contraction, at 48.0, so this release was where economists expected to see some strength.

Within the services survey, New orders dropped to 50.3, employment dropped to a deeply contractionary 46.4, and backlog of orders printed even further in the hole at 44.3. For new orders, July was a second straight month in contraction. For backlog of orders, July was a fifth consecutive month in contraction. I remind readers that this was the service sector survey. Not good.

Wasn't anything strong? You bet there was some strength. In pricing, also known as inflation. That component landed at a very strong 69.9, accelerating from June and a jaw-dropping 98th consecutive month of expansion. Ninety-eight months is more than eight years, gang. That covers this presidency, all of Biden, and most of Trump 1. Yikes.

There's More to the Story...

Equity market weakness on Tuesday was not all on the ISM survey. Investors were in a good mood after Palantir Technologies PLTR had posted a strong quartet and issued strong guidance on Monday evening. The ISM Services PMI was a gut punch, but that gut punch was followed up by an uppercut and a right cross.

Speaking to the media on Tuesday morning, Pres. Trump mentioned that he'd be increasing tariffs on India "very substantially over the next 24 hours" due to that nation's purchases of crude from Russia and its "fueling the war machine." This counteracted, to a degree, the trade deal that the president apparently feels that he is close to with mainland China.

That elusive deal has become more of a "show me" event as the current "trade truce" seems far more sustainable than actually making the progress necessary to reach a trade deal with China that benefits the U.S. The president also announced that new, increased tariffs on semiconductor chips and pharmaceuticals would be coming "within the next week or so."

It's pretty clear that this administration wants both the physical infrastructure for the development of the burgeoning industry for generative artificial intelligence and key pharmaceuticals manufactured domestically. This is probably correctly considered to be a matter of national security. But getting there from here will be painful. Margins will contract for those companies spending huge capex dollars on chips such as Microsoft MSFT, Amazon AMZN, Meta Platforms META and others.

As far as tariffs on pharmaceuticals manufactured elsewhere are concerned, the president mentioned starting out with small tariffs that will grow to as much as 150% and even 250% if the desired results are not achieved. Merck MRK, Eli Lilly LLY and other big pharma firms would be considered to be particularly vulnerable to such a policy.

Marketplace

Ugly? Not especially. Unsettled might be a better word. U.S. Treasury debt securities were sold, but not heavily. That pressure continued overnight ahead of this afternoon's auction of $42 billion worth of new Ten-Year Notes. Yields are up moderately across the entire curve over the past 30 to 32 hours or so.

On Tuesday, the S&P 500 gave back 0.49% coming off of Monday's rally that came on light trading volume. The Nasdaq Composite gave up 0.65% for the day. Obviously, the semis were slapped around a bit. The Philadelphia Semiconductor Index surrendered 1.12%, led lower by GlobalFoundries GFS. That stock was off 9.34% on weak guidance. It wasn't all bad though. The Dow Transports were up 1.12%, as the Russell 2000 gained 0.6%. This kept breadth close.

Breadth

Seven of the 11 S&P sector SPDR exchange-traded funds closed out the Tuesday session in the red, led lower by the Utilities XLU with both "growthy" sectors close behind. The day's winners were led by the Materials XLB as that group continues to benefit this week from dollar weakness.

Interestingly, winners beat losers at the NYSE by a rough 4-to-3 margin, while losers beat winners by just a smidgen at the Nasdaq. Advancing volume took a 53.7% share across Nasdaq-listings and a 50.8% share across NYSE-listings.

This kind of breadth makes it very difficult to draw any seriously negative conclusions from Tuesday's headline-level sell-off. Trading volume was higher, but what does that mean? At the headline level, stocks were lower, but the majority of stocks were higher, and the majority of trades were positive in direction. Check this out...

The Charts

Want some positivity? Here's some:

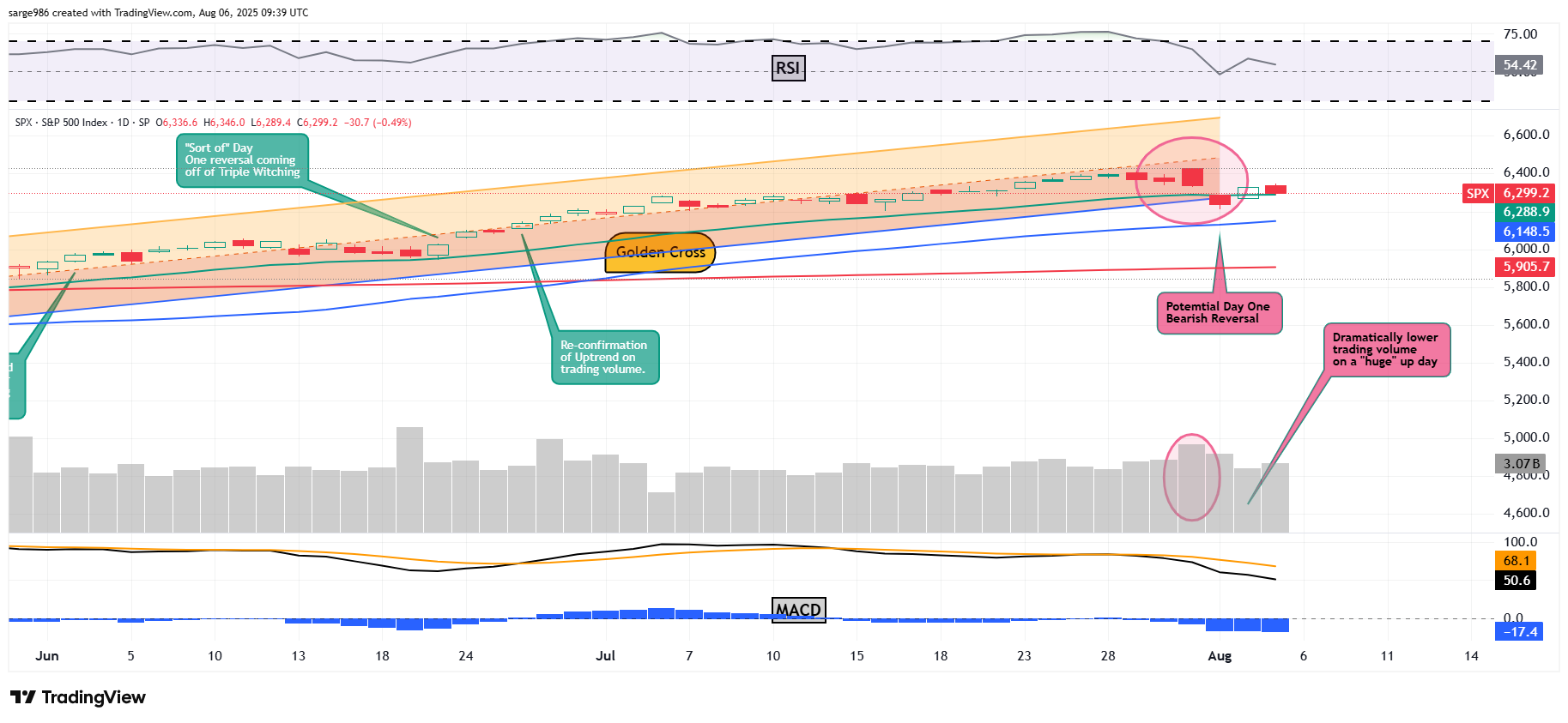

Take a look at Tuesday's candlestick. The index sold off coming off of Monday's strength right down took its 21-day exponential moving average. At that level, the index hit a solid wall and found support after having regained the level the day prior. This suggests a willingness by professional managers to test the level technically and an interest by swing traders in buying that dip. Yes, the daily Moving Average Convergence Divergence still has a bearish look to it, so the S&P 500 is not out of the woods, but that could be interesting as we proceed. I do see that equity index futures are trading higher as I work my way through the time of raccoons and sanitation workers. Now, take a look at this:

This is the S&P SmallCap 600. Wonder why there was some rotation out of the big names on Tuesday and into small stocks? This index saw its 50-day simple moving average pierced to the downside on Monday. The professional managers stepped in and defended that level. Losing that level without anything resembling a fight could have been catastrophic and resulted with managers taking profits where they had them in accelerated fashion as momentum-prioritizing algorithms tried to force the issue. This is why moving capital into smaller stocks was prioritized on Tuesday. The action was more a technical act of self-defense than anything else. The markets are still facing some adversity this week. Tuesday was not the start of anything big and was definitely not any confirmation of a bearish reversal of trend.

So Many Choices

On Tuesday, Pres. Trump ruled out current Treasury Sec. Scott Bessent as the heir apparent to Jerome Powell as Fed Chair, largely because Bessent does not want the job and would like to remain where he is. The president did mention that he has four candidates in mind and mentioned that "both Kevins" are "very good." That would lead outside speculators such as myself to consider that former Fed Gov. Kevin Warsh and current director of the National Economic Council Kevin Hassett might be the front-runners.

Fed Gov Adriana Kugler abruptly and unexpectedly resigned her position last week after being absent and abstaining from last week's FOMC policy vote. The president has said that he will soon nominate someone to Kugler's post. If his choice for the seat at the Board of Governors is indeed someone not currently at the Fed, this will be an opportunity to get them there. Current Fed Governors Christopher Waller and Michelle Bowman are also considered potential candidates.

My personal choice, though I have not been asked for input, would be Judy Shelton, whom I have not heard mentioned as a candidate, but whose ideas on sound money I am a fan of. Shelton was nominated to the board by Pres. Trump during his first term, but she was unable to get through the Senate confirmation process at that time.

Mail Call

In answer to an emailed question... Yes, I have added to my long position in Advanced Micro Devices AMD on overnight weakness, despite the stock trading well above net basis. I had wanted to be longer than it was. AMD met expectations for adjusted Q2 earnings while posting 31.7% revenue growth. The stock is selling off, because data center sales growth was not what some were looking for, and CEO Lisa Su was tight-lipped last night in regard to what investors can expect in regard to AMD's future sales in China. There is also a new tariff-related industry overhang. AMD had been a top ten (number nine) position of mine coming in. I would like to part the stock at number six, just outside of my top five.

Economics

(All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.83%.

07:00 - MBA Mortgage Applications (Weekly): Last -3.8% w/w.

10:30 - Oil Inventories (Weekly): Last +7.698M.

10:30 - Gasoline Stocks (Weekly): Last -2.725M.

1:00 p.m. - Ten-Year Note Auction: $42B.

The Fed

(All Times Eastern)

2:00 p.m. - Speaker: Reserve Board Gov. Lisa Cook.

2:00 - Speaker: Boston Fed Pres. Susan Collins.

4:10 - Speaker: San Francisco Fed Pres. Mary Daly.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: MCD (3.15), PLNT (.79), SHOP (.29), DIS (1.45)

After the Close: APP (2.32), DASH (1.07), BROS (.18), ELF (.83), FTNT (.59), IONQ (-.14), LYFT (.28), MCK (8.15), UBER (.82)

At the time of publication, Guilfoyle was long MSFT, AMD equity.