The Mar-a-Lago Accord

Let's see how military contractors appear to be stabilizing amid Trump-style diplomacy and why the debt security marketplace has a mind of its own; also, we chart the sloppy markets and yield curve.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Some very recent trends across financial markets continued on Monday. Demand for U.S. Treasury debt securities continues to increase, as equity markets continue to have a heavy feel. For the regular Monday trading session, the yield for the benchmark U.S. Ten Year Note dropped three basis points to 4.4%. As I write through the zero-dark hours on Tuesday morning, that yield has dropped further, all the way to 4.33% overnight. The U.S. Two Year Note paid 4.17% late Monday (-2 bps). I now see that product yielding 4.12%. At least we know where some of the capital leaving equity markets and cryptocurrencies is heading.

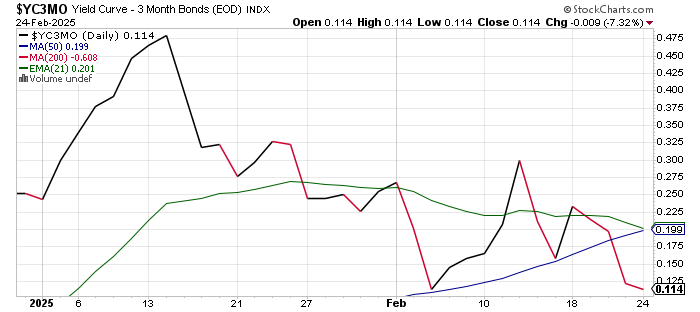

This surge in demand for American sovereign debt is not born of healthy conditions, though. For if the expectations for accelerated consumer-level inflation seen in the recent University of Michigan Sentiment survey and the sudden weakness in the macroeconomic data were to be taken seriously by bond traders, yields would certainly be headed in the other direction. The slope of the yield curve is flattening faster than I would normally be comfortable with.

I know the Trump administration has openly campaigned for lower interest rates, but the market is doing this, not the Federal Reserve. The Fed can only impact short-term rates. The forces of free market price discovery still reign over the belly of said curve out to the deep end of the pool. Just look at the spread between the yields of the U.S. Ten Year Note and the U.S. Three Month T-Bill since the start of the year. This is quite dramatic.

Clearly, the debt security marketplace is not buying the whole "inflation is going much higher" story. Is this market buying the "economic slowdown" story? Not if left to its own devices. Unless one of two items are expected. One, are these markets expecting the central bank to implement some kind of "operation twist" where short-term debt is swapped out for longer-term debt? That would certainly impact the slope of the curve, compressing spreads, while leaving the total federal debt load roughly where it was. Or two, are these markets expecting a surge in foreign demand for U.S. national debt? Food for thought there.

A Mar-a-Lago Accord?

Is there even such an officially unspoken accord under negotiation? Or already being implemented? The chatter among economists and on Wall Street (which is sort of in Miami at least as much as it is in NYC these days) concerns the nation's foreign investors buying or converting U.S. Treasury holdings into zero-coupon bonds that will not trade in the public marketplace. This would be done in exchange for national security defense needs to be provided by and already having been provided by the United States.

Obviously, many traditional U.S. allies will have to provide for more of their own national security than they have in the past. We have already seen European defense stocks take off, while U.S. defense and aerospace stocks such as Lockheed Martin LMT, Northrop Grumman NOC, General Dynamics GD and RTX RTX, which is the old Raytheon Technologies have all found recent support after suffering 2025 declines in value.

Keep In Mind...

The DOGE cuts being implemented amid the ongoing investigations into federal fraud and fiscal recklessness is finding both at incredible and unexpected levels. In addition, we've seen a recent spate of corporate layoff announcements. Even if it takes time for the unemployment and underemployment rates to move higher, which is not immediately clear, the weekly report on initial and continuing jobless claims compiled from state-level data and provided by the Department of Labor is going to show an upward move. That will create at least an algorithmic market response, that in turn could force portfolio managers to defend themselves as soon as this Thursday.

Equities

Stocks have certainly stumbled of late, as a risk-off sentiment has stretched across our marketplace. This has added some safe-haven value to both the above-mentioned Treasury debt securities and gold. Somewhat surprisingly, silver has moved lower of late while bitcoin has simply collapsed, as the definitions of what qualifies as either a safe haven or a "store of value" type asset seems to be narrowing rather quickly.

Stocks opened at higher prices on Monday morning and then sold off, which is somewhat worse than simply opening at lower prices. This shows a lack of confidence by those who were willing to "buy the dip." The issues of the day? There were two. The AI trade continues to melt. Palantir Technologies PLTR continues to slide, heading towards our $84 sweet spot.

Additionally, an analyst report published by TD Cowen implied that Microsoft MSFT was reducing its spending on the buildout of its corporate data centers. Microsoft denied this, but it was enough to rattle markets with high-end chip designer Nvidia NVDA set to report fourth-quarter financial results on Wednesday evening. On top of all of that, President Trump mentioned that tariffs on both Mexico and Canada, which had been postponed, will go into effect next week.

Performance

The S&P 500 gave up 0.5% on Monday as the Nasdaq Composite surrendered 1.21% on weakness across the tech space. Yes, the Dow Jones industrial average managed to keep its head above water (+0.08%), but nobody on Wall Street has considered the Dow Industrials a major equity index since the early 1990s. The Dow Transports (-0.74%) and the Russell 2000 (small caps) at -0.78% also had rough days on Monday.

Surprisingly, six of the 11 S&P sector SPDR ETFs closed in the green for the session, again led by those with defensive characteristics such as Health Care XLV and the REITs XLRE. Technology XLK was slapped around for a loss of 1.43%. Within tech, the Philadelphia Semiconductor Index took a 2.59% beating as Marvell Technology MRVL and Broadcom AVGO gave back 5.9% and 4.91% respectively.

The Dow Jones U.S. Software Index gave up 1.17% for the day, but that was skewed by oversized losses for the stocks of Palantir and MicroStrategy MSTR. The beat-down for MSTR is Bitcoin-related and not related to its commercial environment. Market breadth was weak, but not as bad as it can be.

Losers beat winners by a 5-to-4 margin at the NYSE and a little less than a 2-to-1 margin at the Nasdaq. Advancing volume took a 44.3% share of composite NYSE-listed trade and a 31.6% share of composite Nasdaq-activity. Aggregate trade contracted sharply, however, on a day-over-day basis, across those names domiciled at both the NYSE and the Nasdaq, as well as across the membership of the S&P 500.

Implications of the Selloff

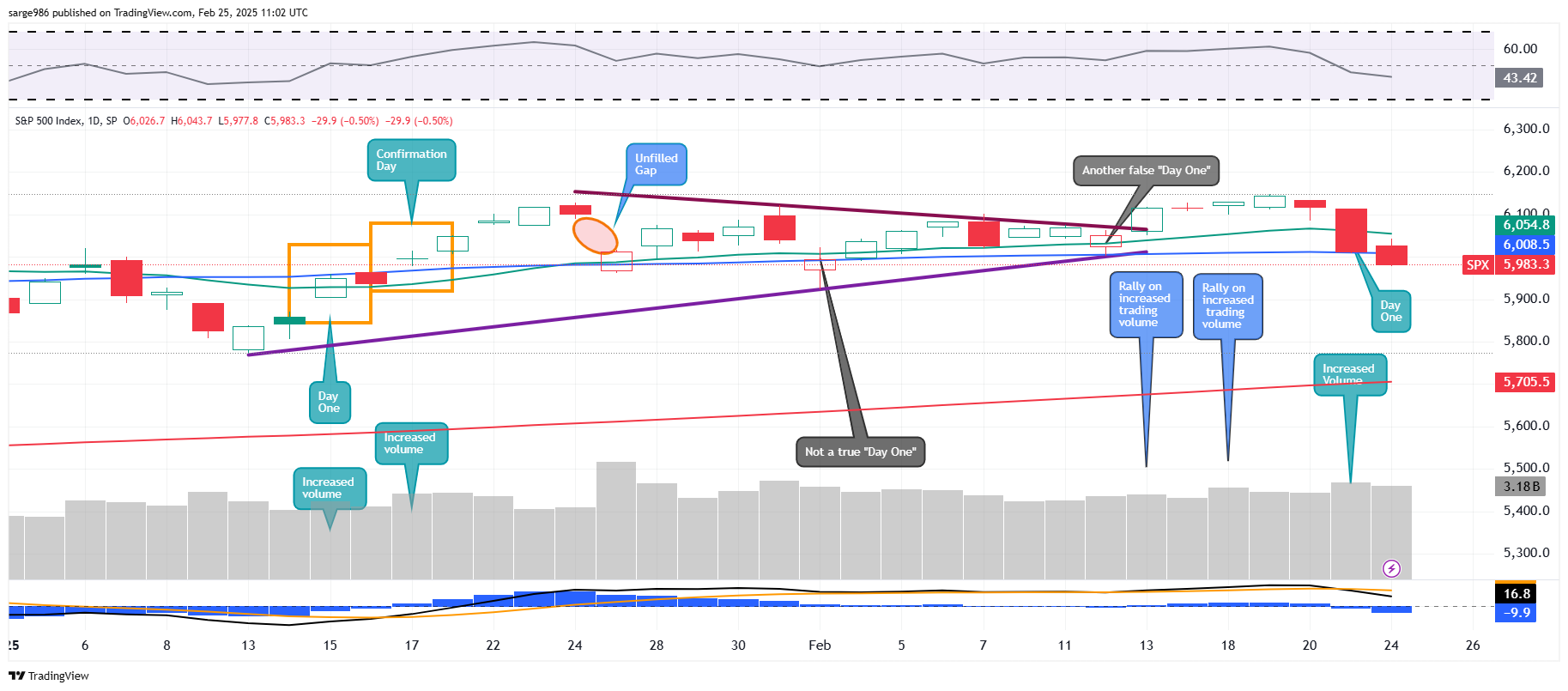

The continuance of the selloff across equities on reduced volume does not constitute a confirmation of Friday's potential "Day One" bearish change in trend, but really presents as part of the same move, and a move that may possibly be growing exhausted. Either that, or timid in front of Nvidia's numbers.

Readers will see that on Monday, the S&P 500 lost the support of its 50-day simple moving average. That said, contact with that line has not been broken and a line of support is not considered lost until said contact is lost. Hence, today (Tuesday) could be a fairly important trading day. Note that the Nasdaq Composite did indeed lose contact with that blue line on Monday. This could very well force portfolio managers to reduce long-side exposure under pressure from the risk managers. How lucky am I that for most of my career, risk managers held a lot less authority than they do in 2025. Then again, I left corporate culture in 2016 to work for myself because I could no longer stand the persistent inanity and lack of freedom in decision making for those still reliant upon Wall Street.

Economics (All Times Eastern)

08:55 - Redbook (Weekly): Last 6.3% y/y.

09:00 - Case-Shiller HPI (Dec): Expecting 4.4% y/y, Last 4.3% y/y.

09:00 - FHFA HPI (Dec): Expecting 0.2% m/m, Last 0.3% m/m.

10:00 - CB Consumer Confidence (Feb): Expecting 102.7, Last 104.1.

10:00 - Richmond Fed Manufacturing Index (Feb): Expecting -2, Last -4.

4:30 p.m. - API Oil Inventories (Weekly): Last +3.34M.

The Fed (All Times Eastern)

04:20 - Speaker: Dallas Fed Pres. Lorie Logan.

11:45 - Speaker: Reserve Board Gov. Michael Barr.

1:00 p.m. - Speaker: Richmond Fed Pres. Tom Barkin.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: HD (3.04), PLNT (.62)

After the Close: AMC (-.16), LMND (-.56)

At the time of publication, Guilfoyle was long LMT, NOC, GD, RTX, PLTR, NVDA, MSFT equity.