The Magnificent 7 Really Are the Index Movers

When the Mag 7 are up, everybody else is down. When the Mag 7 are down, everybody else is up. Maybe the FOMC meeting will change things.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

And just like that, the semis and beloved NVDA get bought and stay right in the range. Also, just like that, as soon as folks start buying NVDA and Apple the rest of the market is sent to the woodshed.

By that, I mean that Monday’s market saw breadth positive and Tuesday’s market saw breadth negative, thus proving that the Mag 7, or whatever you want to call them, should really be called the index movers.

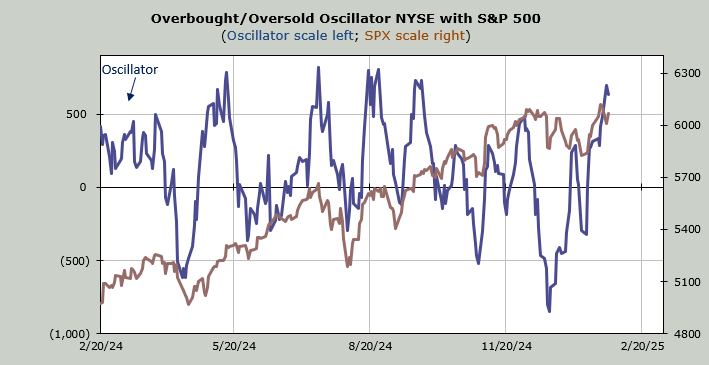

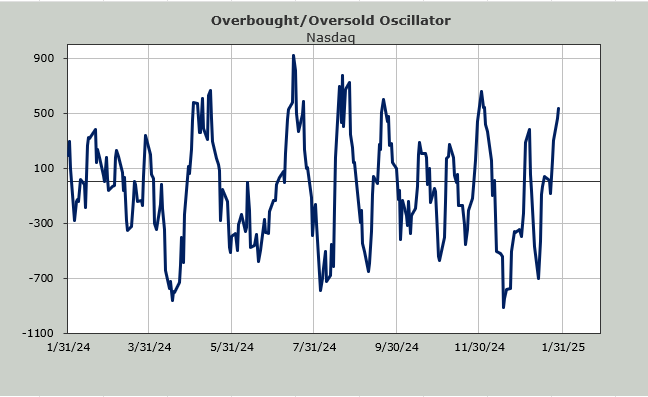

It is not surprising, though, because the market is short-term overbought. And we know that since my Overbought/Oversold Oscillator is based on breadth, it ought to manifest itself in the 493 since they have been positive for eight of the last ten trading days (which is what makes it overbought).

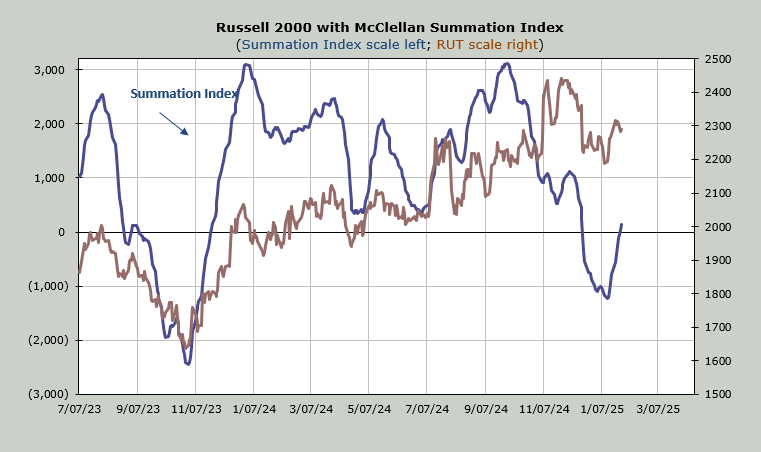

The intermediate-term indicators are still rising. Most are not yet overbought; I expect they will get there sometime in early February. For now the McClellan Summation Index is still rising and did manage to get itself up and over the zero line.

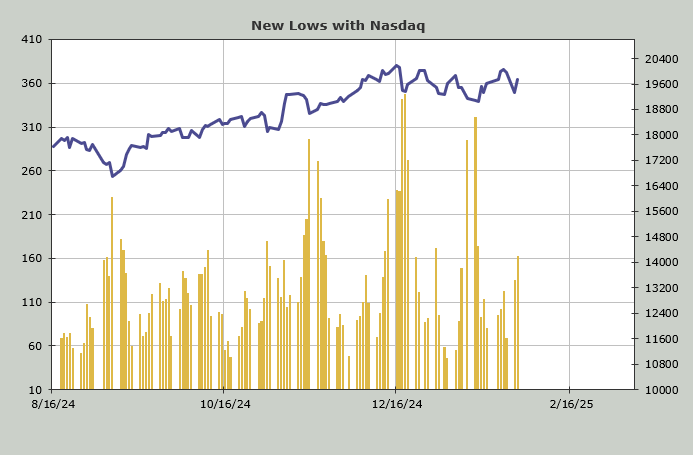

In terms of indicators that have changed this week, the number of stocks making new lows on Nasdaq expanded quite a bit on Tuesday. Tuesday marked the most new lows since January 14th, essentially the low for this recent push upward. We don’t want to see that, especially on a day the index gained two percent.

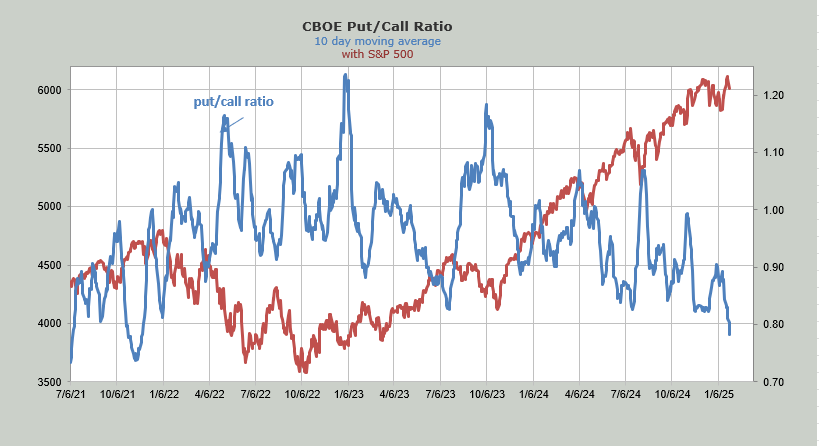

The other indicator that changed is the ten-day moving average of the put/call ratio. Last week folks were a bit hysterical over it and my sense was that there would be time to get hysterical. In fact I even noted that I expected it would be lower this week. And it has gone lower this week.

The ten-day moving average of the put/call ratio now stands at .78. That is the lowest since November 2021 when it was .74. In the last ten days of trading, this metric has not seen one reading over .90. It came close on Monday with a reading of .89 but we haven’t had a reading over .90 since the lows two weeks ago.

You might recall last week the Investors Intelligence bulls had only notched up two and the bears down two. I expected that it would be this week we’d see a bigger shift. This survey will be released early Wednesday morning so we should be able to see if there was a shift worth noting.

Finally, there are the Utes. I thought when they traded up to 1028 (and thus over 1020) I was wrong and that they were out of the woods. They have barely had an uptick since I got sucked in. There is support at 960 from these two prior lows and the uptrend line. I believe that area will hold on this trip down, but I need to acknowledge that it hasn’t mapped out as I thought it would.

We’ll see if the FOMC meeting changes anything.