The Fed Says It Like It Is

Let's discuss the two big takeaways from the FOMC on Wednesday, check out the rally that followed and look at inflation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The takeaway from Wednesday's Federal Reserve policy decision might just be that the Fed took action. Actually, there are probably two key takeaways. The first would be that this version of the Federal Open Market Committee appears not to have its head in the sand. It is cognizant, if not all that proactive, of the issues currently facing the nation's economy.

There were no changes made to the target range for the Fed Funds Rate, though in the quarterly economic projections, the group still expects to shave a half percentage point off of that overnight benchmark interest rate, despite that the group increased its median expectations for both headline- and core-level consumer inflation. Financial markets reacted well to that, despite that the group also reduced its outlook for economic growth this year.

Financial markets also reacted well to the fact that the FOMC took action to significantly slow the pace of its "quantitative tightening" program. As we all know, this balance sheet management program has been working methodically for more than two years in the background of the real economy to draw down on and counter the excess liquidity created going into, during and after the pandemic period.

No, quantitative tightening is not dead. That said, taken straight from the official statement... "Beginning in April, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $25 billion to $5 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion."

This subtle acknowledgement by the Fed that as the economy struggles to adjust to a more protectionist environment that could slow activity, that it is ready should a scarcity of liquidity become an issue, spoke volumes. Markets reacted.

Powell at the Podium

Financial markets also liked this version of Jerome Powell very much, who appeared calm, cool, and almost unconcerned as the economy encounters these issues. What's clear is that while Powell and his central bankers see upward pressure on consumer-level inflation and a slowdown in the pace of activity from tariffs, he and they are downplaying the possibility of a recession.

I just wish that the Fed Chair had not used the term "transitory" in describing his thoughts on any inflation created by said tariffs. One would think that Powell would know better than to go back to that word when discussing inflation. Perhaps the most important item outside of the reduction in the pace of the balance sheet management program was the fact that the FOMC had not changed its median expectation for where the Fed Funds Rate will end 2025, despite the fac that they adjusted their outlook somewhat for literally everything else.

A Breath of Fresh Air

During the press conference, Powell admitted that the environment is uncertain and that he doesn't know anyone who has a lot of confidence in their economic forecasts. I found that comment brutally honest in nature and quite refreshing. We all know "they" don't know. Much better when "they" level with us.

We Know What the President Wants

After the FOMC's actions, Pres. Trump took to social media (Truth Social) and posted, "The Fed would be MUCH better off CUTTING RATES as U.S. tariffs start to transition (ease!) their way into the economy. Do the right thing. April 2nd is Liberation Day in America!!!"

April 2nd is the day when the Trump administration is expected to implement the new reciprocal schedule of tariffs on imports from many nations dependent upon the tariffs those nations place on U.S. exports. The size and scope of this belated U.S. response to what these other nations have been doing all along remains unclear for now.

Rock & Roll

Markets roared on Wednesday afternoon. As the U.S. Dollar Index fell hard on Wednesday, capital poured into U.S. Treasury debt securities, gold, Bitcoin and of course ... equities. The rally has appeared to extend into the overnight session, though it has waned a bit as late night melted into early morning. The U.S. Dollar Index has regained virtually all of what it lost on Wednesday, but Treasuries are still in rally mode. The yield for the U.S. Ten Year Note dropped from 4.32% ahead of the FOMC release to 4.26% afterwards. Overnight, I have seen the Ten Year pay as little as 4.22%.

For the Wednesday session, the S&P 500 gained 1.08% as the Nasdaq Composite popped for a run of 1.41%. Smaller caps performed in line with the big kids as the Russell 2000 and S&P Mid Cap 400 gained 1.57% and 1.23% respectively. Note that the Dow Transports, which are highly dependent upon a healthy environment for economic activity underperformed for the day, gaining just 0.49%.

Ten of the 11 S&P sector SPDR ETFs closed out the day in the green, led by the Discretionaries XLY and Energy XLE as cyclicals led growth. Defensive sectors took the bottom three slots on the daily performance tables and four of the bottom five as the Staples XLP closed unchanged.

Now For Something "Iffy"

The Wednesday session was strong. No doubt about it. Winners beat losers by an 8-to-3 margin at my old home, the New York Stock Exchange, and by a rough 5-to- margin at the Nasdaq Market Site. Advancing volume took a commanding 74.2% share of composite Nasdaq-listed trade and a 73.7% share of composite NYSE-listed activity.

What's so "iffy?" Aggregate trade was not what we needed to see. Composite Nasdaq-listed trade contracted 0.2% on a day-over-day basis from Tuesday, while composite NYSE-listed trade contracted by just a smidgen. You understand what that means, right?

That means that Wednesday's rally was not enough to convince portfolio managers to get off of their tails and chase the market. Granted, the markets were quiet until the FOMC release at 2 p.m. ET. Still, we have often seen markets more than make up for that morning and early afternoon stillness late on Fed Days.

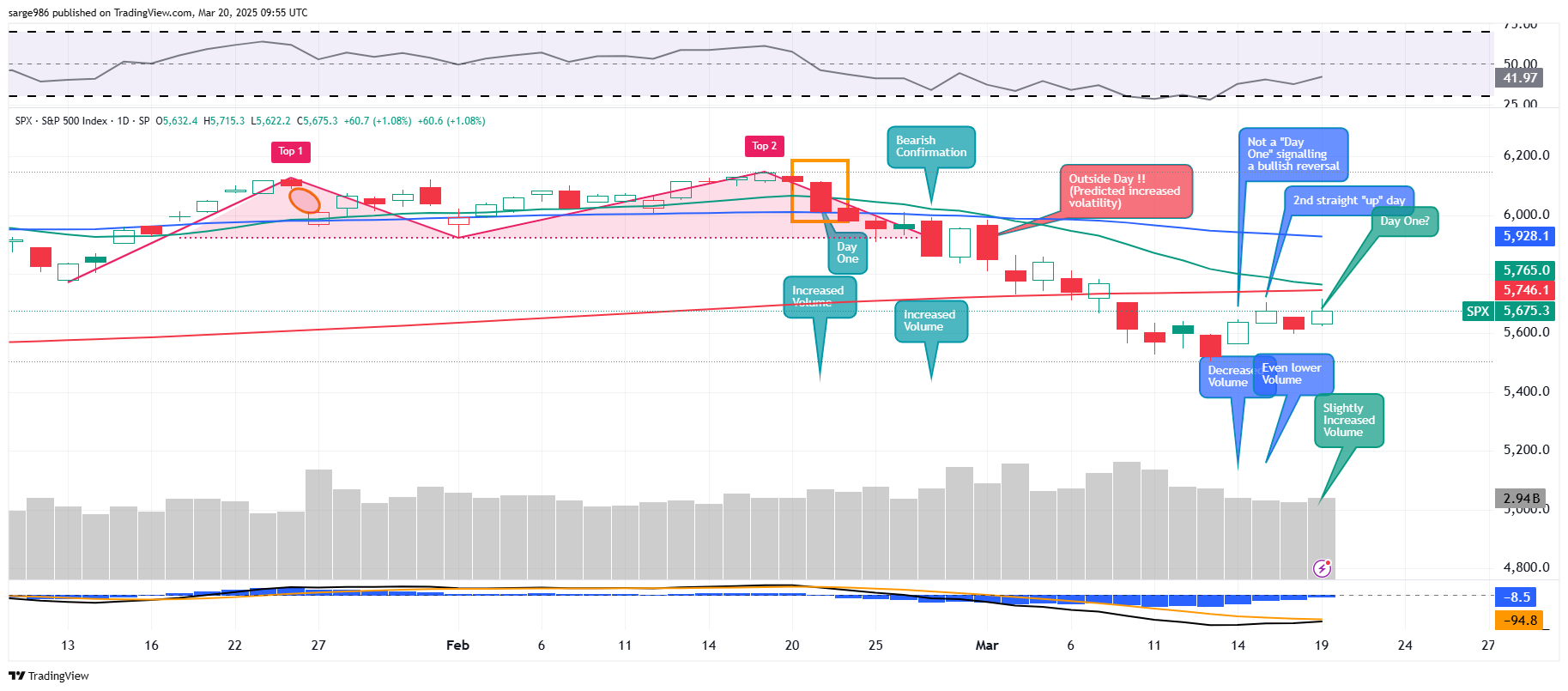

Check This Out...

Readers will see at the lower right-hand side of this chart, slightly increased trading volume across the S&P 500 on Wednesday from Tuesday. Does this make for a "Day One" bullish change of trend? In my opinion, and in all analysis, remember, whether its my work or someone else's, you are dealing with opinion, this increase is not significant enough to be making any declarations. Additionally, trading volume across both the Nasdaq Composite and Nasdaq 100 were lower. Maybe when I was younger, but in 2025, you really don't dance with just the S&P 500 but not the key Nasdaq indices.

This makes Thursday crucial. The indexes have to hold their gains on Thursday and preferably show that conviction in the level of trading activity. As mentioned in previous articles, we won't know a whole lot until these indexes start meeting resistance at their key moving averages and we see how algorithmic traders traverse that environment.

Noteworthy...

New today, Fed Funds Futures trading in Chicago are now pricing in a 55% probability for three-quarters of a percentage point worth of rate cuts in 2025, despite that the FOMC just signaled a half-point worth of rate cuts.

On Inflation...

We all know that the February consumer price index printed at year over-year-growth of 2.8%, down from a seven-month high of 3% in January. Currently, the Cleveland Fed's nowcasting model is showing March CPI at growth of just 2.46% as inflation continues to slow. This is in-line with the Hedgeye Risk Management model that readers know I subscribe to and rely upon, heavily. That's good news, gang. Then again, what did the president say? April 2nd? Perhaps April will be a more focused-upon month than March in this regard. March CPI will be released on April 10.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 222K, Last 220K.

08:30 - Continuing Claims (Weekly): Last 1.87M.

08:30 - Philadelphia Fed Manufacturing Index (Mar): Expecting 10.8, Last 18.1.

10:00 - Existing Home Sales (Feb): Expecting 3.93M, Last 4.08M SAAR.

10:00 - CB Leading Indicators (Feb): Expecting -0.2% m/m, Last -0.3% m/m.

10:30 - Natural Gas Inventories (Weekly): Last -62B cf.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DRI (2.79), DBI (-.49), FDS (4.18), JBL (1.83)

After the Close: FDX (4.64), LEN (1.72), MU (1.43), NKE (.29)

At the time of publication, Guilfoyle had no position in any security mentioned.