The Crypto Capital

Bitcoin and other coins surges amid Trump plan, military contractors turn green following Zelenskyy talks, and ... what does the Fed know about jobs....

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The surging prices for several cryptocurrencies on Sunday were dramatic. Pres. Trump posted his thoughts on the matter on his social media network:

"A U.S. Crypto Reserve will elevate the critical industry after years of corrupt attacks by the Biden Administration, which is why my Executive Order on Digital Assets directed the Presidential Working Group to move forward on a Crypto Strategic Reserve that includes XRP, SOL, and ADA." The president then added, "I will make sure the U.S. is the Crypto Capital of the World."

President Trump finally followed up ensuring that his followers understood that both Bitcoin and Ethereum would be "at the heart of the Reserve."

The president first introduced the very thought of a federal bitcoin or cryptocurrency reserve during the 2024 presidential election run. Sen. Cynthia Lummis, a Republican out of Wyoming, introduced the idea this past summer alongside Pres. Trump and has pushed the concept regularly ever since.

Building such a reserve would put a bid under not just Bitcoin but several of the cryptocurrencies in focus as the reserve builds out. However, some "crypto supporters" have expressed concern that such an action would be in opposition to the idea of monetary decentralization that attracted them to crypto in the first place. Others worry that including various cryptos seen as lower in quality relative to Bitcoin or even Ethereum could hurt not just the credibility of this reserve, but also permit artificial government influence to impact both overall demand and valuation.

Fix Bayonets...

Asian markets have been mixed on Monday (Sunday night into the zero dark hours on the U.S. east coast). Japanese markets outperformed. We are now through the market openings across Europe. These openings have been mixed to moderately higher across the continent. Very interestingly, after the continent's regional leaders gathered on Sunday for a summit in London, there appeared to be agreement to continue to support the government in Kyiv after the dust-up late last week between Presidents Donald Trump and Volodymyr Zelenskyy in Washington.

Leaders from Germany, Denmark, Italy, the Netherlands, Norway, Poland, Spain, Canada (Yes, I know Canada is not a European nation), Finland, Sweden, the Czech Republic, Turkey, and Romania were joined by the NATO Secretary General for the event. French President Emmanuel Macron, U.K. Prime Minister Keir Starmer and Zelenskyy have agreed to work together on forming a plan intended to bring about a peace between Russia and Ukraine and then bring that plan to Pre. Trump.

The key, at least for investors, is that several European leaders pledged to increase defense spending from current levels. As I type this note, European defense contractors such as Dassault Aviation, Rheinmetall AG, BAE Systems, Leonardo, and Thales are all among the top ten Stoxx Europe 600 Index leaders this morning. Here in the US, RTX RTX, General Dynamics GD, Lockheed Martin LMT and Northrop Grumman NOC are all in the green as we traverse the overnight session.

What a Day! What a Month?

Equity markets rallied nicely on Friday. That was a nice day. End of month mark-up? Last week certainly was tough. So was the month of February. It was just February 19th that the S&P 500 created both an all-time intraday record high and an all-time closing record high. Since then, as Treasury debt securities rallied fiercely, stocks met up with the ugly stick and suffered a serious beating.

Interestingly Ryan Detrick of Carson Group who appears on CNBC often and whose thoughts I caught up with at Seeking Alpha over the weekend, passed on some history on what happens to the S&P 500 during years where a negative February follows a positive January. According to Detrick, since 1950, this has happened 16 times.

Of those 16 times, March has been positive 10 times and negative six times for an average return of just 0.2%. For all years since 1950, the S&P 500 has returned an average of 1.1%. For the full calendar year following such a set-up, there is good news though. For those 16 years, the average return for the year has been 12.3%, while the average return for all years 1950 through 2024 has been 9.5%. Additionally, the S&P 500 has been positive 13 of those 16 years (81%), but positive just 72% of all years over that time frame.

Recession Calling?

This past week, the incoming macroeconomic data continued to weaken as had been the recent trend. The Conference Board's February survey for Consumer Confidence fell off of a cliff confirming what we had seen in the University of Michigan's Consumer Sentiment survey for February a few days earlier. Outside of that one data-point, January New Home Sales missed the mark, contracting sharply from December's levels as headline level January Durable Goods Orders printed flat from the month prior.

The Atlanta Fed incredibly went negative and revised their GDPNow model for the first quarter sharply lower to -1.5% from 2.3%. Among other regional central bank district branches running close to real-time GDP models for the current quarter, the New York Fed revised that estimate for Q1 growth down just a smidgen from 2.95% to 2.94%, while the Cleveland Fed took their view for Q1 growth up to 1.86% from 1.85%. The St. Louis Fed revised their model for Q1 GDP lower again, from 1.77% to 1.49% and down from 2.11% two weeks ago.

There is clearly no consensus here as Atlanta has swung from one of the more optimistic models to easily the most negative outlier in the bunch. New York and Cleveland barely touched their models. Keep an eye on St. Louis. Their track record for accuracy is rather strong and they have been continually drawing down their estimate.

Down Week

Among the major to mid-major U.S. equity indexes, the week may have been negative, but was only truly ugly for the big tech crowd...

- The S&P 500 rallied 1.59% on Friday but lost 0.97% for the week.

- The Nasdaq Composite gained 1.63% on Friday but lost 3.47% for the week.

- The Nasdaq 100 gained 1.62% on Friday but lost 3.38% for the week.

- The Russell 2000 gained 1.09% on Friday but gave back 1.47% for the week.

- The S&P Small Cap 600 gained 0.88% on Friday but surrendered 1.08% for the week.

- The S&P Mid Cap 400 rallied 0.99% on Friday, giving up just 0.22% for the week.

- The Dow Transports gained 1.42% on Friday but lost 0.3% for the week.

- The Philly Semiconductors rallied 1.71% on Friday but bludgeoned for a 7.2% weekly loss.

- The KBW Bank Index gained 2.05% on Friday and managed a 0.93% weekly gain.

On Friday, all 11 S&P sector SPDR ETFs closed in the green, led higher by the Financials XLF, the Discretionaries XLY and Energy XLE, all cyclical in nature. Even for the week, just seven of the eleven S&P sector SPDR ETFs still closed in the green, still led by the Financials. But defensive sectors took three of the next four slots on the weekly performance tables.

Technology XLK easily led the losers at -3.98% for the week as the semiconductors took the brunt of the beating. For the week, On Semiconductor ON, and Marvell Technology gave up 12.95% and 11.55% respectively. Nvidia gave back 7.07% for the week after reporting last Wednesday. Just an FYI... I did have my long position in that name as the stock failed to regain contact with its 50-day simple moving average late Friday.

Silver Lining...

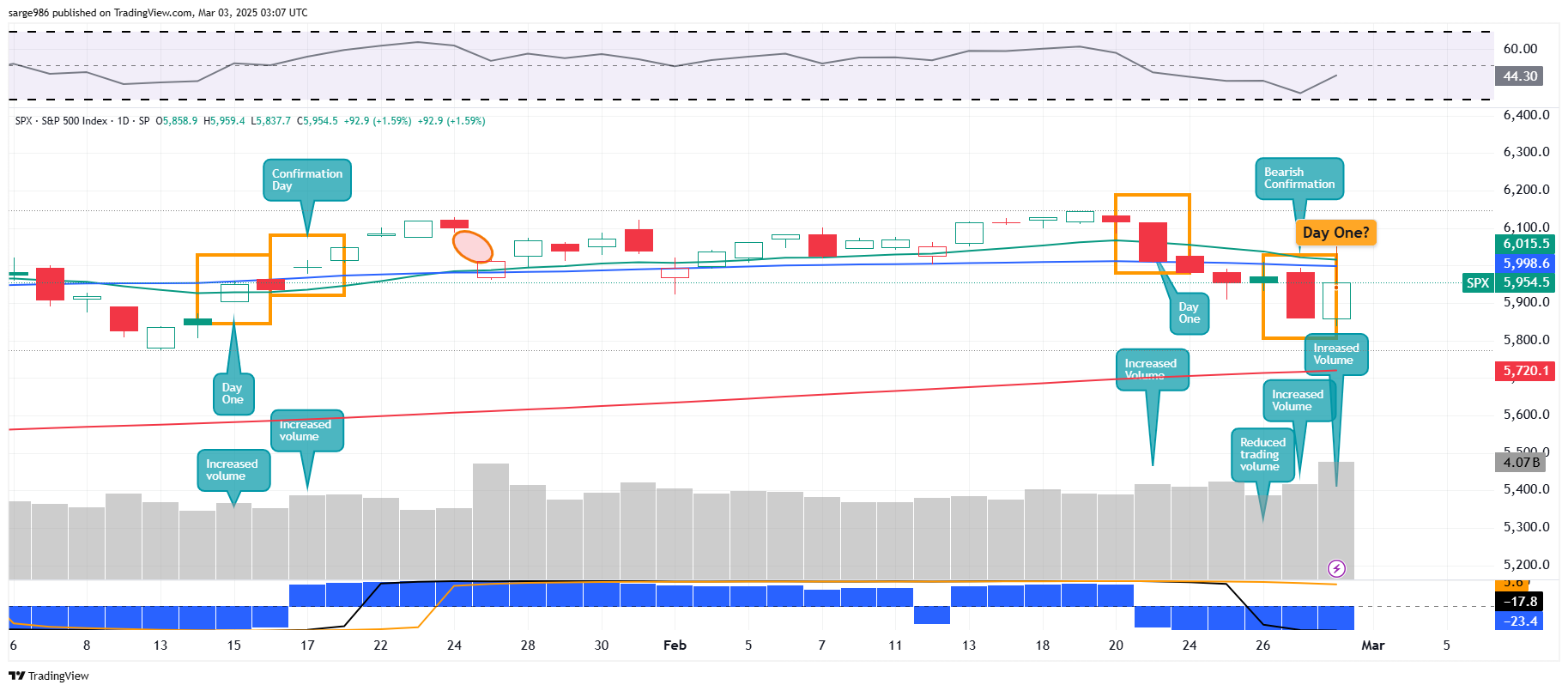

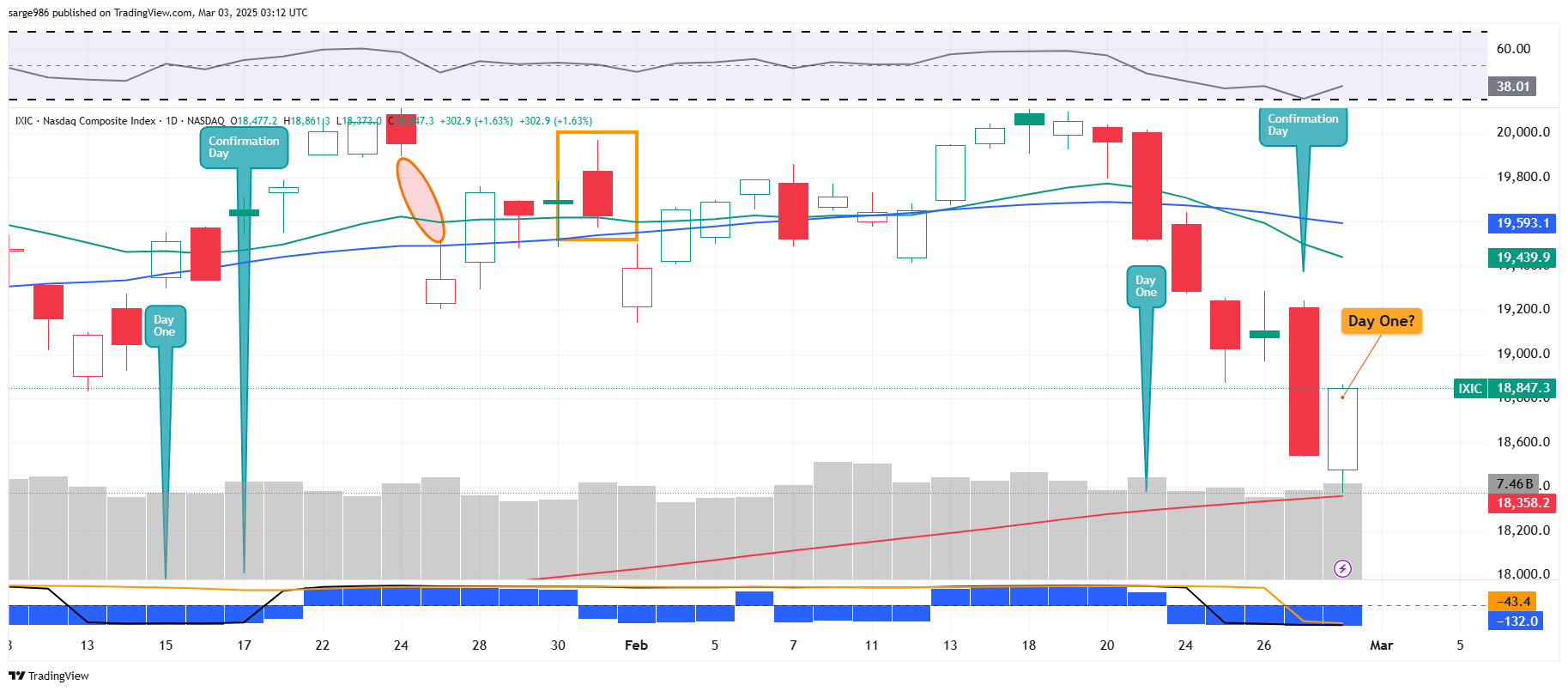

We literally had just called a "confirmation day" on Thursday after the S&P 500 and Nasdaq Composite had sold off on increased trading volume after the early week selling had paused on Wednesday. Yes, common sense tells us that Friday had as much to do with end of month market-ups or pension fund rebalancing as anything else. Still, technically, our equity markets put together a "day one" on Friday, but a "day one" of a potential bullish change of trend. It may be nothing. That's why we wait for confirmation before getting a little nuts. Check this out:

We see very nearly the same situation for the Nasdaq Composite below. Sure, the index is still in a weaker position, but you still have a positive trading session on increased trading volume.

The daily Moving Average Convergence Divergence is still postured quite bearishly, and Relative Strength is not strong, but you do technically have what we call a "day one."

Earnings Squeeze

According to FactSet, with 97% of the S&P 500 having reported their fourth-quarter earnings, 75% of those firms reporting have beaten earnings expectations, while 63% of those reporting have beaten revenue expectations. At this point, for the quarter, earnings growth is running at a blended (results & expectations) rate of 18.2% (up from 16.9% two weeks ago) on revenue growth of 5.2%.

For the quarter, the financials have posted by far the greatest earnings growth of any sector at +55.9%, with communication services in second place at +29.6%. Just one sector has now shown a year-over-year earnings contraction for the quarter, with energy at -26.3%. The industrials, materials and staples have all moved from contraction to expansion over the past few weeks.

As for the current quarter (Q1), consensus is currently for earnings growth of just 7.6% (down from 11.3% a few weeks ago) on revenue of 4.3%, down from 5% over several weeks. For the full year 2025, Wall Street sees earnings growth of 12.1% (down from 14.8% over a few weeks) on revenue growth of 5.5%. Yes, as Q4 results have come in much better than expected... projections for Q1 2025, and full year 2025 have been contracting rapidly. Something to keep an eye on.

As for valuation, the S&P 500 went into the weekend trading at 21.2 (down from 22.2 over two weeks) times 12-month forward looking earnings and 26.1 (down from 27.6 two weeks ago) times 12-month trailing earnings. These ratios both remain well above their respective five-year and ten-year averages.

What Does the Fed Know?

Interesting week ahead for trader types. The Fed will be out in force, and tariff-related headlines will be in focus, but Friday is "February Jobs Day " and that will be the headline level event of the week from an economics / markets perspective.

....The Fed will be rather quiet this week, that is with the exceptions of the release of the Beige Book on Wednesday afternoon and an absolute plethora of Fed officials that will be making public appearances on Friday. This, readers must understand, is highly unusual. It is rare for our central bankers to speak publicly the same day that the Bureau of Labor Statistics releases our nation's monthly employment survey results.

Our central bankers usually take a pass on "Jobs Friday" and come out swinging early the next week in an effort to create or control a narrative around the data. The fact that right now, I have at least five appearances by at least four officials on my radar for Friday definitely has me wondering what they know about the jobs numbers and why they are being overt in their effort to be public almost immediately.

Maybe I'm just being paranoid, but for those who are not economics nerds, this is not normal. Fed Chair Jerome Powell speaks at 12:30 p.m. ET from a monetary policy forum at the Chicago Booth School of Business. Fed Gov. Michelle Bowman and New York Fed Pres. John Williams are also set to speak at that event.

.... The Macroeconomic calendar will obviously be active this week. It will all be about Friday. For the month of February, the unemployment rate is expected to have held steady at 4%, but there is expected to be a rise in underemployment as employers may have moved some staff from full time status to part time. Average hourly earnings is expected to have held at a pace of 4.1% annual growth, but average hourly workweeks for full-timers is expected to have remained alarmingly low, at 34.1.

For those unaware, this is well below the normal range of 34.3 / 34.4 hours for this series. The average full time hourly wage US worker has not seen 34.3 weekly hours since November and has not seen 34.4 weekly hours since March 2024.

.... The earnings calendar is rather light this week, as the Q4 2024 reporting season winds down. Investors will hear from the likes of Best Buy BBY and Target TGT on Tuesday morning followed by key tech names Marvell Technology MRVL, MongoDB MDB and Zscaler ZS on Wednesday afternoon. On Thursday, Campbell's Soup CPB, Macy's M, Broadcom AVGO and Costco COST will all report.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Feb-F): Flashed 51.6.

10:00 - ISM Manufacturing Index (Feb): Expecting 50.7, Last 50.9.

10:00 - Construction Spending (Jan): Expecting 0.1% m/m, Last 0.5% m/m.

The Fed (All Times Eastern)

11:35 - Speaker: St. Louis Fed Pres. Alberto Musalem.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: GTLB (.23), OKTA (.74)

At the time of publication, Guilfoyle was long NVDA, RTX, LMT, GD, NOC equity.