The China Chat; Philly Up, N.Y. Down; Semis and Small Caps Boom

Let's look at the lead-up to the U.S.-China call today, the after-effects of the Fed Day, Nvidia and the semiconductors.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

You made it. Again. Every week really does feel like its own marathon these days, even if the past few months have created quite fertile ground for turning a profit. It's still a laborious process. Not that we're ungrateful, especially those of us with no base salary, for anything the marketplace bestows upon us. We only eat, if we can hunt and kill. Modern day, high-tech hunters and gatherers are we.

Thursday was a spectacular day for traders and investors. I did tell readers to get long growth stocks on Wednesday's weakness in my Fed piece that day. Huzzah. I did not mention that maybe readers should also buy small caps. Boo, hiss.

There are no significant quarterly earnings releases set to hit the tape today. There are no significant domestic macroeconomic data-points about to make headlines. For today, there is but a phone call on the docket. Oh, and one Fed speaker. San Francisco Fed Pres Mary Dal, who has sounded dovish of late, will make a public appearance at 2:30 p.m. ET. San Francisco is not a voting member of the Federal Open Market Committee this year and will not regain voting rights until 2027.

The Phone Call

Presidents Trump and Xi off the U.S. and China are expected to speak over the phone today (Friday). The two nations held trade talks earlier this week in Madrid, where the U.S. was represented by Treasury Sec. Scott Bessent and mainland China Vice Premier He Lifeng. It would appear that not all that much came out of those meetings other than the fact that trade relations between the two largest economies on the planet are no worse today than they were a week ago, except maybe for Nvidia NVDA.

While Beijing has apparently dropped its antitrust probe into Alphabet's GOOGL Google, Beijing has also ordered that nation's largest tech companies to avoid purchasing AI-capable, U.S. export-rules compliant chips designed for that market. Beijing would apparently prefer that large Chinese tech companies purchase chips from other Chinese companies.

Still, supposedly, those negotiations did, according to U.S. reports, include a framework commercial agreement for Chinese company ByteDance to divest its TikTok social media app, at least in the U.S., to U.S.-based purchasers. Details of any sale were not publicly discussed, though Oracle ORCL is thought to be among a group of buyers. Bessent did say that any deal required the approval of both heads of state. That is what may come out of this phone call. Improved access for U.S. companies to rare earth minerals and magnets would be nice, too.

Pleasant Surprise (Depending on Where You Are)

Yes, the Philadelphia Fed Manufacturing Index is often looked at by economists as the most important regional manufacturing sector survey in the country. Yes, earlier this week, the Empire State Manufacturing Index for September landed in a surprise state of contraction. In the New York region, New Orders plummeted in September as did Shipments, Number of Employees, Average Workweek, and general Business Conditions.

That's why it was such a nice surprise to see the manufacturing sector flourishing in the Philadelphia region for the month of September. Maybe business is just getting ahead of the mayoral election in New York City? Maybe. It is clear though, that at least this month, conditions for manufacturing businesses deteriorated sharply in New York and New York's loss was Pennsylvania's gain.

For the Philadelphia region, which includes most of Pennsylvania, the southern half of New Jersey and all of Delaware, new orders rocketed out of contraction in September as the headline number absolutely soared. Shipments boomed as well as did inventory building. Even better was the noticeable deceleration in growth for both prices paid and prices received. Number of employees and average workweek both avoided the fate suffered in New York for the month and avoided falling into contraction. I really do not know if it's the "Mamdani effect," but it is not all the time that we see one regional district suddenly flourish so obviously at the expense of a neighboring district.

The Environment

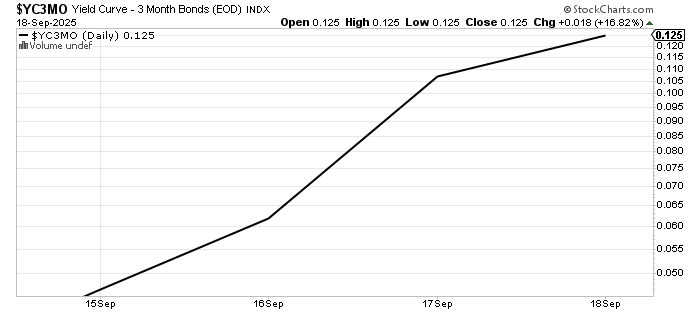

Thursday. How did markets respond to the Fed's policy decision on Wednesday afternoon after getting to sleep on it for a day? Pretty well if one is mostly in equities. Treasuries sold off from the Two-Year Note out to the Thirty-Year long bond, steeping the curve as T-Bills largely found support, the shorter duration the T-Bill the better. This is what the spread between the yields of the Three-Month Bill and the Ten-Year Note looks like this week:

Not only is that interesting. It's early in the easing cycle that Fed Chair Jerome Powell was careful in referring to as a cycle, but this does not help those seeking mortgagees or those burdened with credit card debt. Of course, the U.S. Dollar Index rallied on Thursday and gold sold off, which may be somewhat counterintuitive to what some traders might have thought.

Of course, we need to see a longer timeline before making assumptions or putting together economic models. That said, if equity traders are pricing in a lengthy cycle of easier monetary policy while bond and currency traders are not, something is going to break somewhere. I am waiting before passing judgement as an economist. As a trader, though I have traded just about everything other than cryptocurrencies professionally, I am an equities guy at heart.

Stocks

The S&P 500 popped for a gain of 0.48% on Thursday as the Nasdaq Composite ran 0.94%. Both closed at all-time record highs yet again. The Nasdaq indexes were led by a Philadelphia Semiconductor Index that soared 3.6%. The semis were obviously led by Intel's INTC 22.8% gain after headlines circulated of a deal made between Intel and Nvidia.

This deal not only puts Intel's foundry business on the map but includes a $5B investment in the struggling chipmaker. Micron MU also gained 5.6%. Interestingly, with a U.S. foundry business suddenly getting a boost like that, the semiconductor equipment companies all popped nicely as well. Applied Materials AMAT, KLA Corp KLAC and Lam Research LRCX all had nice days on Thursday.

The small- to mid-cap indexes actually outperformed the broader large-cap indexes. The Russell 2000 added 2.51% for the session, making a new record high just like the majors. The KBW Banks, and Dow Transports also showed gains. The only red on my index screen at day's end came from the VIX and the Dow Utilities.

On The Weekly Chart

Is the Russell 2000 trying to break out of a giant Cup with Handle Pattern with a $2,466 pivot that dates back to late 2021? Keep an eye on this.

Breadth

Seven of the eleven S&P sector SPDR ETFs closed out Thursday's regular session in the green with Tech XLK obviously out in front followed by the Industrials XLI. Three of these funds closed in the red, with the Staples XLP mired in last place on the daily performance tables. The Materials XLB somehow, even with a stronger dollar, managed to close unchanged.

Winners beat losers by a little less than a 2-to-1 margin at the NYSE and a little more than 5-to-2 margin at the Nasdaq. Advancing volume took a 74.3% share of composite Nasdaq-listed trade and a 64.9% share of composite NYSE-listed activity. As for aggregate trading volume, the picture was mixed. Day-over-day volume across Nasdaq-listings increased 12.4%, which implies institutional conviction in the tech / AI / growth trade and maybe even conviction in the small-cap trade. Aggregate trade, however, dropped 8.8% across NYSE-listings. That implies less conviction in the economic growth trade. That. by extension, could negatively impact the small-cap trade to a far greater degree than it would the tech trade.

Economics

(All Times Eastern)

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 539.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 416.

The Fed

(All Times Eastern)

2:30 p.m. - Speaker: San Francisco Fed Pres. Mary Daly.

Today's Earnings Highlights

(Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long NVDA, MU, LRCX equity.