The Big Trade: China Agrees to Rare-Earths 'Deal'

Reports of a rare-earths deal with China help boost trading, but we'll see how priced in the news is Friday. Also, let's check developments in stable coins and chart something ... scary?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It finally happened. The very rumor probably had a little something to do with Thursday's rally across U.S. equity markets. The actual news resulted in the rally in Europe and supported U.S. equity index futures overnight. How priced in that news is, we'll find out on Friday. That news itself, though, is decisively positive.

Bloomberg News, among others, reported on Thursday evening that the U.S. and mainland China had finalized something of a trade deal or framework, or "agreement" (in Bloomberg's words) that the two nations had reached last month in Geneva and then reinforced in London. Put bluntly, U.S. Secretary of Commerce Howard Lutnick told the media, "They're going to deliver rare earths to us" and in response, "We'll take down our (tech-related) countermeasures."

On Friday morning, the Chinese Ministry of Commerce released a statement confirming that such a deal had been signed. China will review and approve export applications to items subject to export control rules, while the U.S. will cancel a range of existing restrictive measures imposed against Chinese purchasers. Specifics were not given.

Lutnick appeared on Bloomberg TV and informed viewers that the president was likely to finalize a slate of trade deals within the next two weeks ahead of the July 9 deadline that had been set. Lutnick said, "We're going to do top 10 deals, put them in the right category, and then these other countries will fit behind."

It just so happens that a team of trade officials from India are scheduled to hold meetings with their U.S. counterparts over the next two days. The U.S. and Japan are also currently in trade discussions that neither side has yet made comment on. There is a chance that with so many nations now rushing ahead of that deadline, that the deadline could be extended.

Other Rally News ...

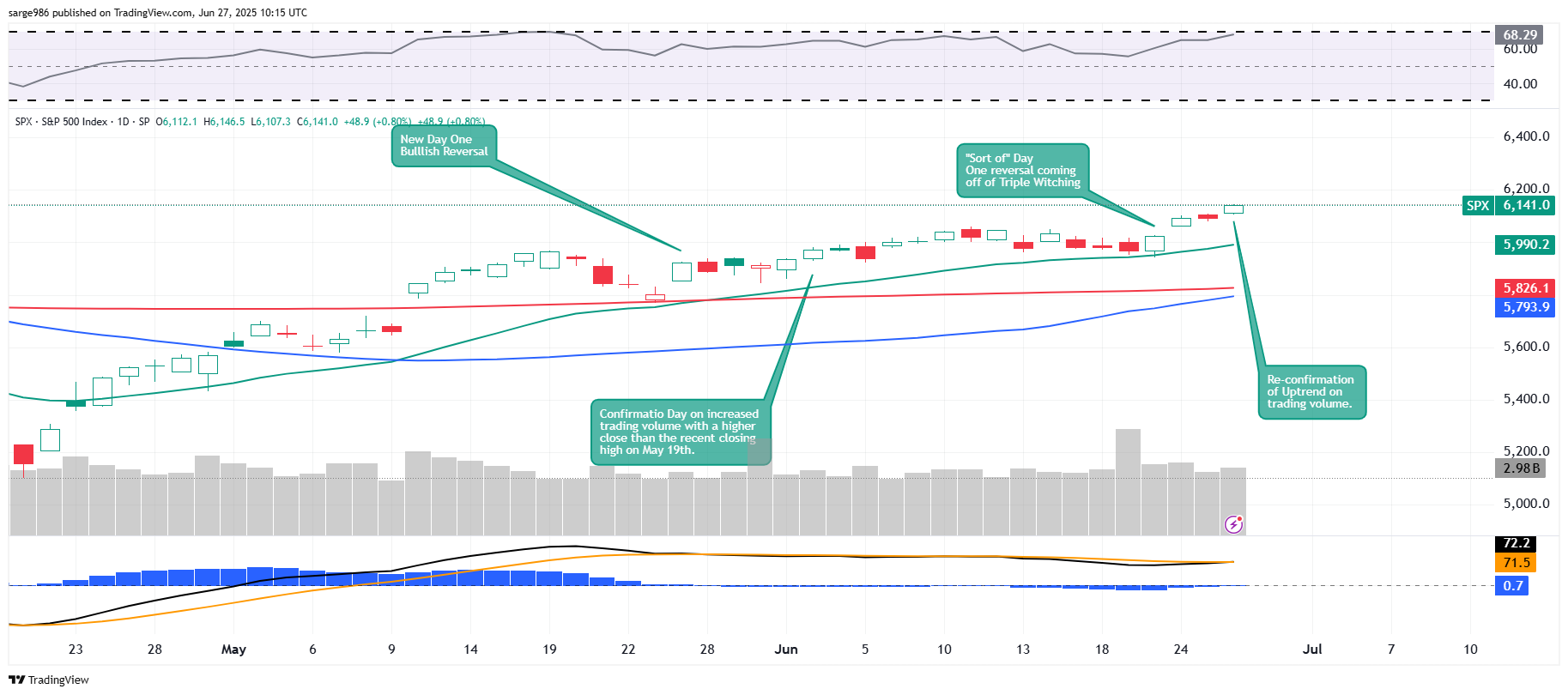

There was more to the rally, of course, on Thursday that pushed the S&P 500 to the doorstep of a new all-time record high. On Thursday, the S&P 500 closed at 6,141 after apexing for the session at 6,146. Back on Feb. 19, the index closed at "just" 6,144, but after peaking at 6,147. The "deal" with China only started making the rounds up and down Wall Street later in the day.

Ahead of that, markets reacted to the fact that the U.S. Treasury Department has announced a deal with the rest of the G-7 to exclude U.S. businesses from taxes imposed by other nations in exchange for the removal of Pres. Trump's Section 899 (or simply the "revenge tax") from the "big, beautiful bill." Congressional tax committee chairs are already on board with the change to the bill made at Secretary Bessent's request.

In addition to that, House Republicans are planning a single vote to pass the Senate's Genius Act (and its own Clarity Act) and get at last the Genius Act to President Trump's desk for an autograph (with an actual pen controlled by an actual human hand attached to an actual US president) by next week.

The idea behind the Genius Act would be to normalize stable coins, while bringing them into a more standardized and increased regulatory environment. Why is this good for stocks? Understand that stablecoins can put downward pressure on short-term interest rates, as these tokens are often backed by U.S. Treasury Bills. The increased demand for these short-term investments, in turn, can drive higher prices for those T-Bills, which puts downward force on yields.

This could be helpful in a monetary environment where the Federal Open Market Committee appears to have abandoned any and all connection to data dependency. At a time when both consumer-level inflation has weakened significantly and the U.S. economy has started to sputter, a little data-dependency at the central bank would be nice. It could be called "nice." It could also be called actually doing one's job. After cutting rates ahead of the election last year when there was nowhere near the case for a rate cut that exists now, this Fed Chair's position is quite shaky (not to mention, absurd) and many members of the FOMC have started speaking out.

Bank Rules ...

News broke on Wednesday that helped push values for risk assets higher on Thursday that this same Federal Reserve Bank had proposed easing some post-financial crisis requirements for large banks, which would free up some capital. The board voted 5 to 2 to issue the proposal to reduce the enhanced supplementary reserve ratio.

The proposal asks those large banks to comment on the possibility of excluding the purchase of U.S. Treasury debt securities from the leverage ratio denominator. Doing so would allow those banks to purchase more federal debt in times of financial stress, creating a broader avenue for safe-have seekers. This could also place downward pressure on yields.

Marketplace

On Thursday, the Nasdaq Composite gained 0.97% as the S&P 500 popped for an upside move of 0.8%. The rally was broad in nature as small- to mid-cap stocks stole the show. The S&P 400, S&P 600 and Russell 2000 gained 1.32%, 1.56% and 1.68% respectively. Nine of the 11 sector SPDR ETFs ended the Thursday session in the green with Energy XLE and Communication Services XLC out in front. In a positive sign for stocks, the bottom three rungs on the daily performance tables were all populated by sectors that are defensive in nature.

Breadth was outstanding. Winners beat losers at the NYSE by more than a rough margin of 9 to 2, and at the Nasdaq by about 9 to 4. Advancing volume took a commanding 0.9% share of composite NYSE-listed trade and a 72.3% share of composite Nasdaq-listed activity. Most importantly, on a day-over-day basis aggregate trading volume increased across the realms of NYSE-listing and Nasdaq-listings and across the membership of the S&P 500. You know what that means, right, gang? Check this out...

Take a look at that. Remember earlier this week when I wrote that Monday may serve as a "sort of" Day One bullish reversal after three consecutive "down days?" My point at the time was that although trading volume on Monday was lower than it had been last Friday, last Friday was a triple-witching expirations event. Therefore, the true comparison on trading volume for Monday, had to be last Thursday.

On Wednesday, the S&P 500 paused. Remember, we always like to see a pause ahead of a technical confirmation. That indicates that it was not all one move and at least some managers were adding long-side exposure after thinking about what they were doing and not just as a reflexive response to visible momentum.

Then came Thursday. An impressive upside move on increased day over day trading volume. We call that a "Confirmation Day." In short, the S&P 500 experienced a Day One bullish reversal on May 27th. The upward trend was confirmed by volume on June 3rd. This past Monday, after the rally had stumbled around a little, we had a Day One wake up call. The uptrend was reconfirmed by volume yesterday. Huzzah!

Fear the Reaper?

Just beware ... the bears, if there are any left, are going to see great potential for a Double-Top bearish reversal at this level.

Now, we expect positive trade news over the next few days. Should that news not hit the tape in the way we now expect, there is a technical reason for a negative response. We also have the Personal Consumption Expenditure inflation numbers for May due this morning and the Fed's stress test results this afternoon.

Does That Scare Me?

No. I am still proceeding as if we are in a risk-on environment. That does not mean that I am blind to potential avenues of attack or spots where investors or trades could walk into an ambush. Heads on a swivel. I'm taking advantage of the rally while it's a rally.

Economics (All Times Eastern)

08:30 - Personal Income (May): Expecting 0.3% m/m, Last 0.8% m/m.

08:30 - Consumer Spending (May): Expecting 0.1% m/m, Last 0.2% m/m.

08:30 - PCE Price Index (May): Expecting 0.1% m/m, Last 0.1% m/m.

08:30 - Core PCE Price Index (May): Expecting 0.1% m/m, Last 0.1% m/m.

08:30 - PCE Price Index (May): Expecting 2.1% y/y, Last 2.3% y/y.

08:30 - Core PCE Price Index (May): Expecting 2.5% y/y, Last 2.6% y/y.

10:00 - U of M Consumer Sentiment (March-F): Flashed 60.5.

10:00 - U of M One-Year Inflation Expectations (March-F): Flashed 5.1%.

10:00 - U of M Five-Year Inflation Expectations (March-F): Flashed 4.1%.

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 554.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 438.

The Fed (All Times Eastern)

09:15 - Speaker: Reserve Board Gov. Lisa Cook.

09:15 - Speaker: Cleveland Fed Pres. Beth Hammack.

4:30 p.m. - Bank Stress Test Results.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle had no position in any security mentioned.