The Big Shift: Charting Changes, Bessent Speaks, Trump Moving Back In and More

Let's see if this is a 'Day of Confirmation,' examine Treasury Secretary pick's positions, and review Nasdaq and S&P charts.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Veteran hedge fund manager Scott Bessent had his confirmation hearing before the Senate Finance Committee for Secretary of the Treasury on Thursday and made a few of his thoughts on pertinent matters clear. He spoke to some things that I think we all can agree on. For example, he called the potential failure by Congress to extend the 2017 tax cuts by year's end as an "economic crisis" and "a crushing $4 trillion tax hike." He even referred to a failure to renew and extend those cuts as an "economic calamity" that would fall most heavily upon the middle class.

Bessent also declared that the U.S. government is "not going to default" on his watch and that he would respect the independence of the Federal Reserve on matters of monetary vs. fiscal policy. He responded to questions on the budget as one might have expected, saying that the U.S. "must work to get our fiscal house in order" but backed incoming President Trump's openly expressed view that "Social Security and Medicare will not be touched." In doing so, he pointed out that discretionary spending excluding those two programs is up 40% over just the past four years.

Two items of importance that Bessent was not heavily pressed on by the senators present nor did he offer much clarity on, was the need or not to still have a debt ceiling and the glaringly gross mismanagement of federal debt-load duration by current Treasury Secretary Janet Yellen, though Sen. Elizabeth Warren of Massachusetts did try to take him there on the debt limit.

A Bridge to Sell

Interestingly, during the hearing, Bessent referred to the Chinese economy as "the most imbalanced, unbalanced economy in the history of the world" and stated that the Chinese government is "using their surpluses to fund their military machine." He also stated that China is "in a severe recession / depression" and is "trying to export their way out of their current malaise."

Almost on cue, though many professional economists share views similar to Bessent on this matter, on Thursday evening (U.S. East Coast time), China's National Bureau of Statistics reported that the Chinese economy had hit its target for gross domestic product growth of 5% in 2024, despite slowing industrial production, and slowing retail sales. This was achieved by posting 5.4% fourth-quarter growth, which was exactly what the Chinese economy needed to hit 5% growth, it target for the year.

The stimulus applied to the economy by the Chinese government during the fourth quarter is credited with getting the numbers needed to hit targets but was still a deceleration from 5.4% growth in 2023. It should be noted that consensus view for the quarter was for growth of an even 5.0% and that calculations done by Bloomberg News showed nominal growth for the Chinese economy for the full year of 2024 at 4.2%.

Speaking of GDP

On Thursday, here in the U.S., after December retail sales fell short of headline expectations, but met core expectations, the Atlanta Fed revised its GDPNow model for the fourth quarter up to growth of 3.0% (q/q, SAAR) from growth of 2.7%. Yes, the Philly Fed Manufacturing Index printed at its strongest pace of growth since the cows came home, but that survey is a January (Q1) number. The Atlanta Fed tweaked higher its inputs for real personal consumption expenditures, and real government expenditures, while tweaking lower its input for real gross private domestic investment. Atlanta will revise the model again later this morning after December Housing Starts and December Industrial Production hit the tape.

The Necessary Pause...

Remember what I wrote to you on Thursday morning: That for Wednesday's rally to be confirmed as the "Day One" of an upward change in trend, that there had to be a pause in between that day and the "Day of Confirmation." No promises, but to this point, U.S. equity markets are playing along to our script.

After Wednesday's rally that swept up both debt and equity securities in a mini state of pre-inaugural relief, debt securities held their ground for the most part, but equity performance was lumpy. The yield for the U.S. Ten-Year Note fell to 4.61% on Thursday and that is where I have seen it this morning. The Two-Year Note has been hanging around 4.25% as well.

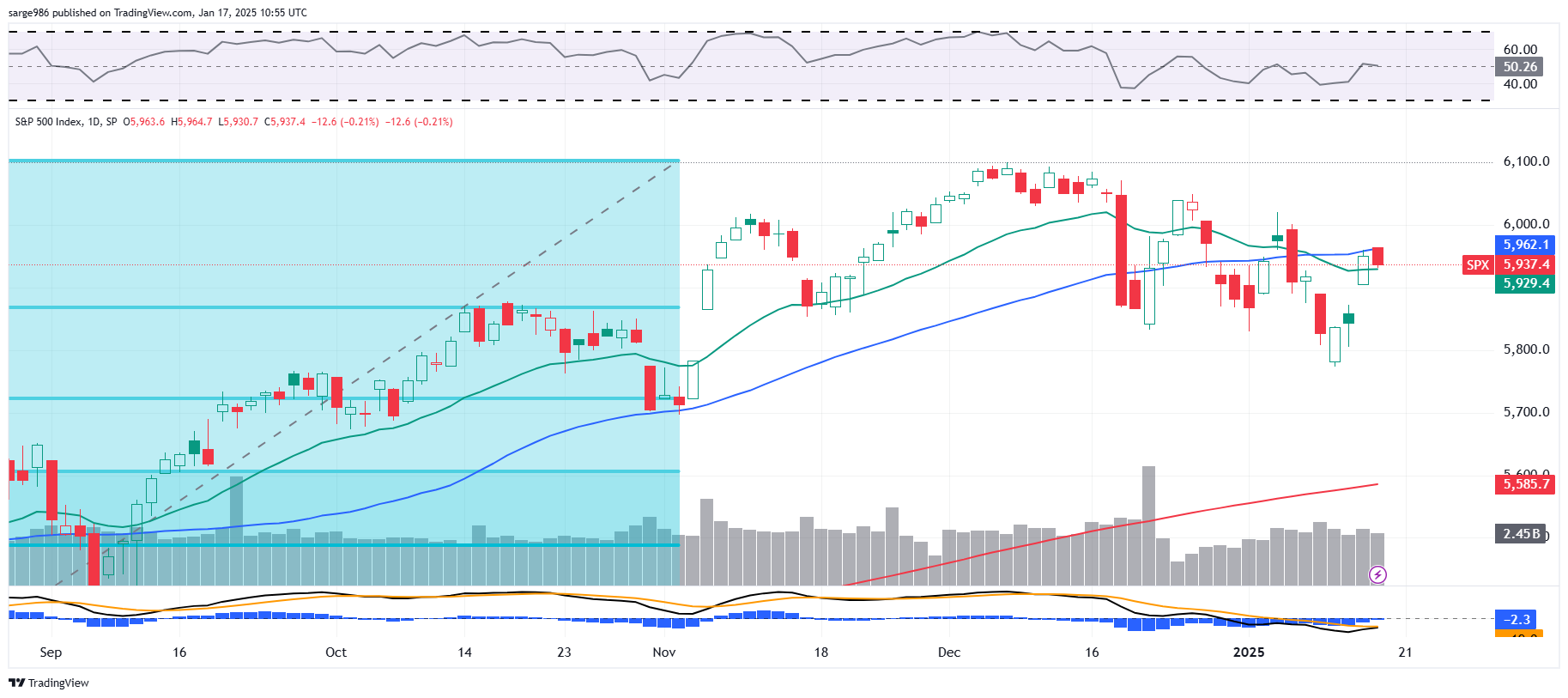

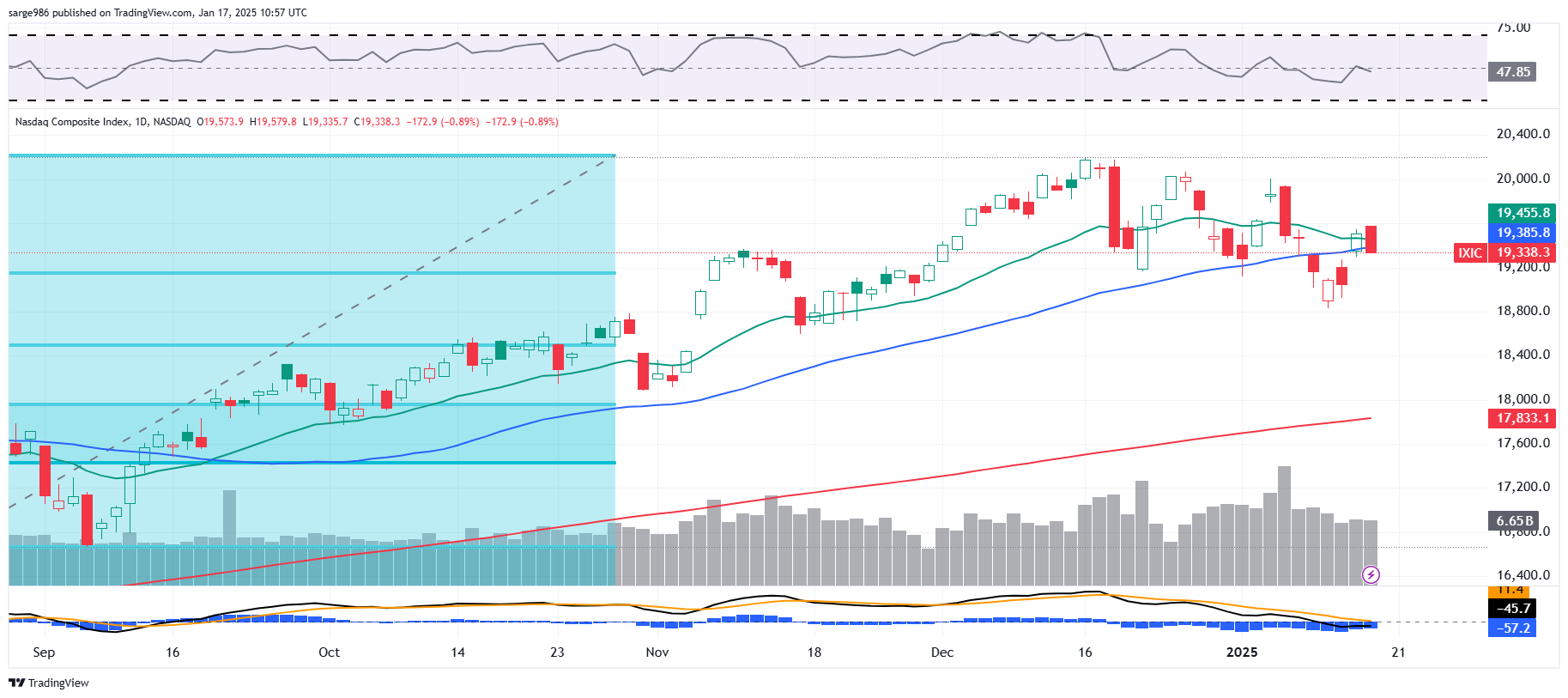

But the Nasdaq Composite was slapped around for a loss of 0.89% for the regular session as the S&P 500 gave up 0.21%. This gave the overall market a negative feel despite the fact that all of the small to midcap indexes closed in the green and the Dow Transports gained 0.98% on the day.

A Down Day with Positive Internals?

Exactly. Eight of the 11 S&P sector SPDR exchange-traded funds gained ground on Thursday, with the most interest rate sensitive funds in the lead. The Utilities XLU and the REITs XLRE gained 2.53% and 2.24% respectively, while growth underperformed. Tech XLK gave up 0.77% as Communication Services XLC gave back 0.57%. This was despite the fact that a solid earnings release by Taiwan Semiconductor TSM driven by demand for AI-capable chips led to winning sessions among the semiconductor equipment providers. Applied Materials AMAT, KLA Corp KLAC and Lam Research LRCX posted gains of 4.54%, 4.33% and 4.03% respectively.

Breadth was beautiful... for a "down" day. Winners beat losers by a rough 5-to-3 margin at the NYSE and by just a smidgen at the Nasdaq. Advancing volume claimed a 63.3% share of composite NYSE-listed trade and a 57.4% share of composite Nasdaq-listed activity, again ... on a "down" day. Even better, aggregate trade ebbed just a bit on a day over day basis, -5.7% across NYSE-listings and -2.4% across Nasdaq-listings, which plays into our "Day One and wait" short to medium-term analysis perfectly.

Note That...

While the 50-day simple moving average remains an unconquered hill for the S&P 500, support was provided on Thursday by the 21-day exponential moving average. Within the daily Moving Average Convergence Divergence indicators, the 12-day exponential moving average has made contact with the 26-day EMA, though both are still below the zero-bound.

The Nasdaq Composite did give up its 50-day simple moving average on Thursday.

In order to keep our semi-positive narrative alive, this index probably cannot lose contact with that line.

It's Friday

U.S. financial markets are closed this coming Monday in honor of the late Dr. Martin Luther King Jr. Monday also happens to be Inauguration Day as the presidency changes hands. The long weekend along with the transition of power coupled with what is expected to be fairly huge monthly options expiration could make for a somewhat volatile session. In other words, we could see the increase in trading volume that the bulls are looking for. The direction just has to be higher. Should this thesis fail, it's still Friday.

Go Notre Dame!

Why? Because I'm Irish Catholic? I am, but no. Because I served in the Fighting 69th Infantry (The Irish Brigade) of Civil War fame that Notre Dame's athletic teams are named for (Bet you didn't know that)? I did and they are, but no. Simply because if Notre Dame wins the national title, it makes both Army and Navy, 12-2 and 10-3 respectively, look better and perhaps gets both of them into the final Top 25. That hasn't happened since 1960.

Economics (All Times Eastern)

08:30 - Housing Starts (Dec): Expecting 1.32M, Last 1289M SAAR.

08:30 - Building Permits (Dec): Expecting 1.46M, Last 1.493M SAAR.

09:15 - Industrial Production (Dec): Expecting 0.2% m/m, Last -0.1% m/m.

09:15 - Capacity Utilization (Dec): Expecting 77.2%, Last 76.8%.

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 584.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 480.

4:00 - Net Long-Term TIC Flows (Nov): Last $152.3B.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CFG (.83), FAST (.48), HBAN (.32), RF (.55), SLB (.90), STT (2.44), TFC (.88)

At the time of publication, Guilfoyle had no position in any security mentioned.