That Was Then, This Is Now

Here's why 2026 is unlikely to repeat the Q1 2025 market playbook. We also check in on sentiment's 'giddy gauge,' the QQQs and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I have a confession to make. I just typed "2025" on the top of this document when I started it. Like that old joke about how "I’m still writing (last year) on all my checks." Oh some of you youngsters don’t even know what a check is, but you get the point.

I bring this up because several folks have asked me if I see a repeat of what happened in the first quarter of 2025 occurring in 2026. Let me state right now that not only do the indicators look vastly different, I also believe markets rarely repeat the same action in consecutive years.

Sure it happens, but it’s rare.

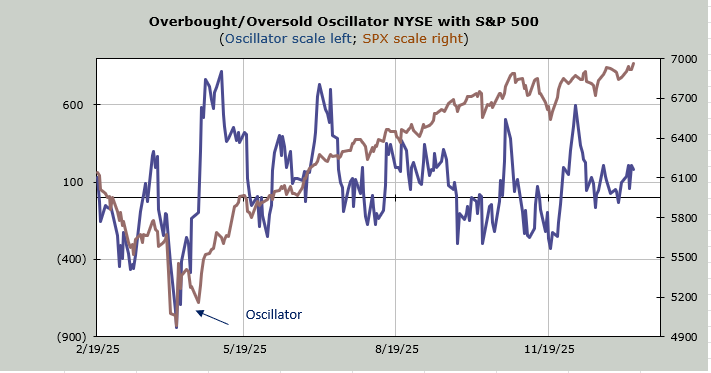

Let me remind you that in December 2024 the majority of stocks peaked after the November rally. That meant that the ensuing three months were a series of lower highs for most stocks. The small-caps are loved now but look at the action in January heading into February last year: a giant chopfest at a lower high.

It is possible, since we only have one week of January under our belts, that the small-caps go into a chopfest now and start the same setup we had heading into late February, but they wouldn’t be doing it from a lower high.

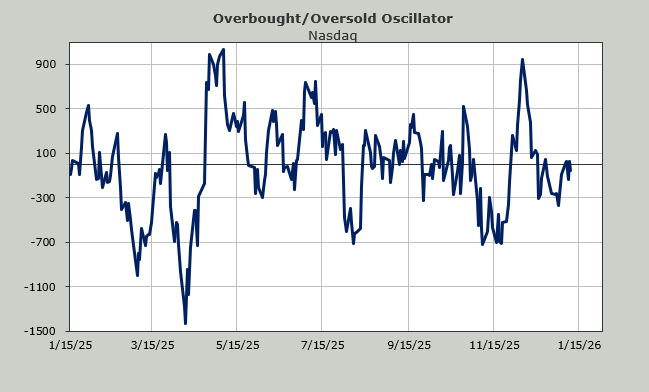

Now let’s look at the (QQQ) s. We are now in month three of no new high for this tech-heavy ETF. In January last year we were a few weeks into it not three months. So the charts look different.

Now what might be possible is the way the QQQs had that last-gasp false breakout in February (arrow) before heading south. Think of what a rally over this present line would do. It would take us from complacent to giddy. It would get everyone to stop pointing out the lagging mega-cap tech stocks.

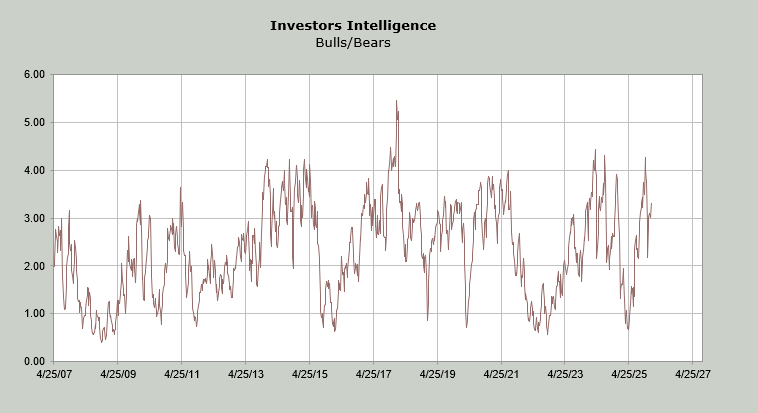

It would take the sentiment indicators that are sitting just below giddy right into giddy. For example, the Investors Intelligence bull-to-bear ratio is currently 3.3, but it wouldn’t take much to tip to over 4.0 (which is giddy).

Last week the bulls were 56.6% and the bears were 17%. What if the bulls moved to 60% and the bears down to 15%, which isn’t very far, is it? That would scoot the ratio right over 4.0.

What if the equity put/call ratio, which has been below 0.50 for two consecutive days (heading into giddy territory) saw another few days with readings in the 40s, or even low 50s? That would scoot the 10-day moving average back down to the low 50s. That would make it giddy.

I think it is too much to ask to get the Daily Sentiment Indicators (DSI) to giddy quickly though. They are currently 71 and 73 for the S&P 500 and Nasdaq, respectively. Over 85, as they were in late October, would take quite a move up, not a small one. It’s possible but not likely.

Once again, as I have said for months now, sentiment is complacent but not giddy. It was giddy in late October but we came off the boil. We did not get fear, we just came back to complacent, which is where I think we still are.