Tech Trade Gets Thorny; Hynix Hit; U.S. to Ramp Up Fight With Iran?

Here’s how I’m handle the tech trade as it gets tough; also, let’s check the latest with Iran, the semis and … some good news on inflationary data.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

U.S. military forces attacked targets inside of Iran for a fifth straight day on Thursday. Iran fired upon U.S. military bases inside Kuwait and Jordan. The U.S. and Iran have accused each other of violating the all-but-forgotten “memorandum of understanding” that never prevented Iranian forces from attacking civilian merchant vessels traversing the Strait of Hormuz anyway. The beat goes on.

Late Wednesday, International Energy Agency Executive Director Fatih Birol spoke from the Aspen Security Forum in Colorado. Birol said bluntly, “If the Strait of Hormuz remains closed, we may again have some difficulty for global economies, including those in the region and developing nations and Asia. It is not months, it is weeks” until the Strait needs to be “fully open, unconditionally open.”

According to Bloomberg News, as the war has intensified of late, Visible traffic through the Strait has notably thinned out over the past week or so, as vessels have been hit and the U.S. Navy has reimposed its blockade of Iranian ports. We know that Saudi Arabian loadings from inside the Persian Gulf have waned significantly.

On that, U.S. military aircraft, early on Thursday morning, fired missiles and hit the U.S.-sanctioned Belma after that vessel repeatedly ignored warnings that it was in violation of the naval blockade and continued to approach Kharg Island, which is the Iranian island where as much as 90% of that nation’s crude exports are shipped out of. The U.S. Navy did permit a bulk carrier loaded with soybean meal to enter into the area. The Navy has stated that shipments of food and medical supplies will be permitted to reach Iran’s civilian population.

Going to Get Worse…

… before it gets better? On Wednesday evening, the Wall Street Journal reported that U.S. Pres. Donald Trump was leaning toward expanding military operations inside Iranian territory. The president apparently hosted a meeting in his Situation Room the day prior to discuss the potential seizure of the above-mentioned Kharg Island as well as other coastal territories. The potential bombing of Pickaxe Mountain, where it is believed that Iran has continued to develop a nuclear weapons program was also discussed as was expanding strikes against internal infrastructure used by Iran’s military.

While taking possession of Kharg Island would more than cripple the Iranian economy and its potential to recover, it would also require extensive use of U.S. “boots on the ground.” The operation would be too large to get away with the surgical use of Marine Raiders or Navy Seals. The operation would likely also require the use of shock-type troops that would include U.S. Army Rangers and U.S. Marine Corps infantry.

There is a growing fear across financial markets that such actions will continue to pressure crude oil supplies and subsequently supplies of refined gasoline as well as liquefied natural gas. There is also a fear that, while seizing Iran’s ability to export and refine crude oil would expose certain elite U.S. military units to hostile enemy fire, occupying and securing those locations would require a larger number of troops. Depending on how well the U.S. air war is in suppressing Iranian capabilities, these troops would likely face the same drone and missile attacks that Iran is launching against civilian cargo ships as well all of that nation’s neighbors. There would be more U.S. casualties than the American public is used to hearing about.

Chip Rout Goes On

While you were sleeping, shares of SK Hynix (SKHY) traded 11.5% lower in South Korean market action. Samsung Electronics gave up 8% as well. In Japan, the heavily invested Softbank Group surrendered 6.3%. This followed a bifurcated U.S. trading session on Wednesday where the headline equity indices moved higher but the Philadelphia Semiconductor Index gave up 2.1%. SanDisk (SNDK), Micron (MU), Marvell (MRVL) and Intel (INTC) led the U.S. losers.

That leads us to Taiwan. Taiwan Semiconductor (TSM) reported a great quarter. The world’s leading chip foundry posted 77% annual and 23% sequential earnings growth while both sales and profitability beat expectations. The company lifted its current quarter sales forecast. Still, TSM is down more than 3% overnight. Does that have to do with capital spending? Maybe. TSM announced that the company will invest an additional $100 billion in its Arizona-based facilities to meet strong U.S. demand, bringing its total investment in that state to $265 billion.

Traversing This Environment as a Tech Trader

Am I running for the hills in the tech or semiconductor space? No. Not really. Regular readers well know that I had to reduce my exposure to the memory / storage basket. That was a matter of self-defense. Not all of that cash has been redeployed, so my cash levels (in percentage terms) are at their highest since the divorce was finalized.

That said, TSM remains my largest holding. Advanced Micro Devices (AMD) has moved back into my top five holdings with Intel knocking on that door. Away from the semis, CrowdStrike Holdings (CRWD) remains a top five name for me and has been one of our strongest performers over the past few months (Up 128% from the April low). I have also moved Microsoft (MSFT) back into my Top 10. Nvidia (NVDA) you ask? Still exposed. Has not been a Top 10 name in months.

There Was Good News

On the macroeconomic front, on Wednesday, the Bureau of Labor Statistics released its data for June producer level prices. Those results for the month of June were just as encouraging as were the ice-cold consumer level prices released on Tuesday. Headline PPI for June printed at -0.3% month over month and growth of 5.5% year over year. This was well below the 6.2% growth that had been expected and down sharply from 6.5% growth in May.

Core PPI prices grew 0.2% in June on a monthly basis and 4.7% year over year. This was also well below the expected 5.2% growth and down from May’s 4.9% print. The data on inflation both at the consumer and producer levels for June was very positive for the US economy. That put some pressure on yields (bond prices higher) as it became clear that there is no logical economic case to be made for a hike in short-term interest rates.

That said, the intensification of the war in the Middle East will impact July prices. I have already seen higher prices at the pump this week in my neighborhood as I am sure you have. While shortages of crude, fuel oil, crude oil and natural gas would not be relieved by changes in monetary policy, they still impact businesses and consumers. This makes it awfully difficult to trust the progress made in June on taming the inflation beast.

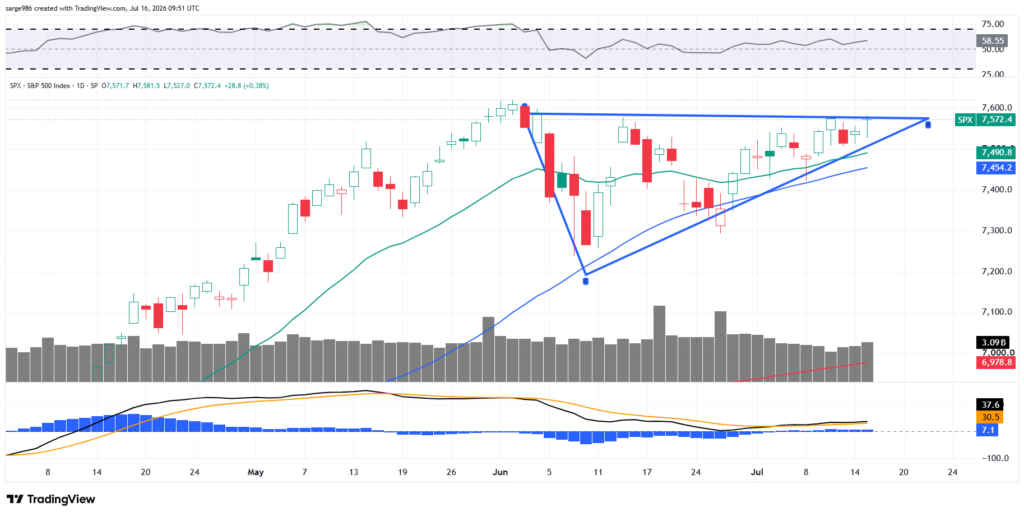

Hmmm…Look at the Chart…

My program accidentally removed all of my notations from my daily chart of the S&P 500. That allowed me to see this:

That’s an Ascending Triangle pattern, kids. Ascending Triangles are patterns uo bullish continuation. This is not only supported by robust but not technically overbought reading for Relative Strength, but by the current posture of the daily moving average convergence divergence. That indicator is now sending multiple short to medium-term bullish signals. Food for thought.

Economics (All Times Eastern)

08:30 – Initial Jobless Claims (Weekly): Expecting 216K, Last 215K.

08:30 – Continuing Claims (Weekly): Last 1.814M.

08:30 – Philadelphia Fed Manufacturing Index (July): Expecting 12.0, Last 10.3.

08:30 – Retail Sales (June): Expecting 0.3% m/m, Last 0.9% m/m.

08:30 – Core Retail Sales (June): Expecting -0.1% m/m, Last 0.8% m/m.

10:00 – Business Inventories (May):

Expecting 0.3% m/m, Last 0.5% m/m.

10:00 – Pending Home Sales (June):

Expecting -0.3% m/m, Last 3.8% m/m.

10:00 – NAHB Housing Market Index (July):

Expecting 35, Last 35.

10:30 – Natural Gas Inventories (Weekly): Last +61B cf.

The Fed (All Times Eastern)

12:30 – Speaker: Dallas Fed Pres. Lorie Logan.

19:00 – Speaker: Federal

Reserve Vice Chair Philip Jefferson.

Today’s Earnings Highlights (Consensus EPS Expectations)

Before the Open: ABT (1.28), GE (1.86), USB (1.29), UNH (4.85)

After the Close: NFLX (0.79)

At the time of publication, Guilfoyle was long SNDK, MU, INTC, TSM, AMD, CRWD, MSFT, NVDA equity.