Tariff Tightrope, 'Confirmation Day' Calling, Elon Lets Loose, CrowdStrike ... Ouch!

Let's chart the markets, welcome Wells Fargo's latest good news, hear Musk's true view of the 'big, beautiful bill' and take some pain killer after that CrowdStrike report hit last night.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I Wanna Rock

Turn it down you say

But all I got to say to you is time again I say no (no)

No, no, no, no, no

Tell me not to play

Well, all I got to say to when you tell me not to play I say no (no)

No, no, no, no, no

So, if you ask me why I like the way I play it

There's only one thing I can say to you

I wanna rock (rock)....

- Dee Snider (Twisted Sister), 1984

'Extremely Hard to Make a Deal'

Last Thursday, Treasury Secretary Scott Bessent referred to U.S. / China trade talks as "a bit stalled" and implied that Presidents Trump and Xi would likely need to get in touch with one another to advance those talks further. The two leaders, representing the planet's two largest economies, have not spoken directly to one another since January, and that was prior to Inauguration Day, so they have not spoken since Pres. Trump officially reclaimed the office.

On Monday of this week, White House Press Sec. Karoline Leavitt said that the two presidents would speak this week. This, of course, came after both nations accused each other of having violated the 90-day trade truce that both had agreed to last month. Most of you, if you were following the markets last night, saw U.S. equity index futures markets wiggle.

Those futures have recovered overnight but definitely swooned last night. That was in response to a post on Truth Social by Pres. Trump that reads... "I like President Xi of China, always have, and always will, but he is VERY TOUGH, AND EXTREMELY HARD TO MAKE A DEAL WITH!!!" Does that mean that the call between the two is imminent? Markets are acting like it as we traverse the zero-dark hours.

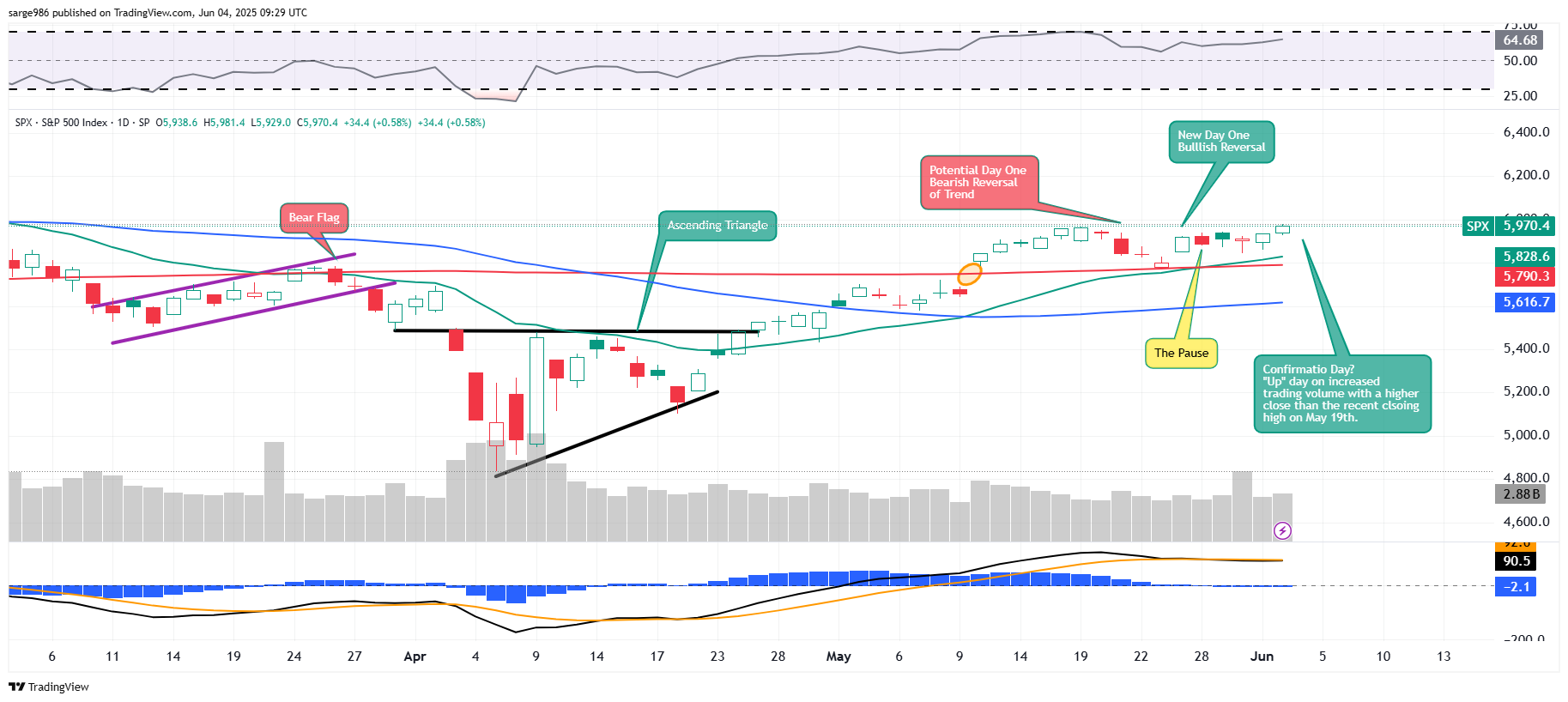

Confirmation Day?

I'd be really slow about making that call, especially ahead of this Friday's employment report. That said, that's sort of what the S&P 500 experienced on Tuesday. "Sort of." On Tuesday after starting off weakly, US equities rallied. That was almost a carbon copy of Monday's trading pattern, with the exception that there was a little more trading volume on Tuesday.

For the session, the S&P 500 added 0.58%, while the Nasdaq Composite tacked on 0.81%. The rally on Tuesday, was broad in nature as all of the small to midcap indexes participated as did the Dow Transports, the KBW Banks and the Philly Semiconductors. Eight of the eleven S&P sector SPDR exchange-traded funds closed out the day in the green with three of these funds gaining more than 1%. Technology XLK, Energy XLC, and Materials XLB led the way.

The fact that all three of these groups are either labeled as growth or cyclical in nature is a market positive. The fact that all four defensive sectors closed in the bottom six slots on the daily performance tables is also a market positive.

As far as trading volume is concerned, there is obviously some caution evident with such a huge economic event coming at the end of the week, but Tuesday was clearly positive. Winners beat losers by a 9-to-4 margin at the NYSE and by slightly better than 2 to 1 at the Nasdaq. Advancing volume took a 69.4% share of composite NYSE-listed trade on Tuesday and an even stronger 71.4% share of composite Nasdaq-listed activity.

Now, here's what matters as long as Presidents Trump and Xi don't screw this up, or the Bureau of Labor Statistics labor market report on Friday prints either too hot or too cold. Aggregate trading volume increased by 4% across NYSE-listed securities on Tuesday and by 2.7% across Nasdaq-listed securities. Trading volume, while not huge by any means, also grew across the membership of the S&P 500.

What It Looks Like...

Readers will see that on Tuesday, the S&P 500 traded higher on increased trading volume, breaking the pause, and closed above the recent closing high of May 19.

The S&P 500 is now less than 3% away from retaking the intraday record high of February 19. Yes, though with the call between the two presidents imminent and with May jobs data due Friday, it is difficult to be bold, we do have a technical confirmation of a bullish change in trend that occurred with last Thursday's "Day One."

Wells Fargo Comes Around

This is why we have been long Wells Fargo WFC all this time. After the close of business on Tuesday afternoon, the Federal Reserve announced that Wells Fargo is no longer subject to the asset growth cap that had been imposed upon the bank in 2018. The Fed has announced that Wells Fargo has net all conditions required by the consent order.

Under the enforcement action taken in 2018, Wells Fargo was required to improve its governance and risk management program and then complete a third-party review for the restriction on growth to be removed. The consent order was placed upon the bank in 2018 in response to a series of scandals that came to light in 2016.

Current CEO Charlie Scharf, whom your author is a fan of, took the job in 2019 with the stated mission of resolving the bank's regulatory issues and cleaning up its reputation. Mission accomplished, Charlie. Nice job.

Tell Us What You Really Think, Elon

Speaking of reputations. Former DOGE king and White House cost cutting czar Elon Musk, who really put his reputation on the line, not to mention, his businesses, is not too fond of the "big, beautiful bill." Musk posted to his "X" social media network, calling the bill a "disgusting abomination" and described it as a "massive, outrageous, pork-filled Congressional spending bill."

The CEO of Tesla TSLA added, "Shame on those who voted for it: you know you did wrong. You know it." While the passage of this bill is likely a market positive, for the time being anyway, it's very hard not to agree with Musk on this issue, unless we can definitely say that this spending will surely be offset by tariff driven revenue. Musk's point is valid.

The Ugly Stick Visits CrowdStrike

CrowdStrike Holdings CRWD reported last night. The stock took out our $470 target price last week. Hopefully, those of you long the name with me, maintained some target price discipline. The stock went out last night at $488.76. I have seen the stock trade with a $455 handle early this morning. Guess, I'll have to come back to you with something in depth on this one in a few hours.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.98%.

07:00 - MBA Mortgage Applications (Weekly): Last -1.2% w/w.

08:15 - ADP Employment Report (May): Expecting 115K, Last 62K.

09:45 - S&P Global Services PMI (May-F): Flashed 52.3.

10:00 - ISM Non-Manufacturing Index (May): Expecting 52.0, Last 51.6.

10:30 - Oil Inventories (Weekly): Last -2.795M.

10:30 - Gasoline Stocks (Weekly): Last -2.441M.

The Fed (All Times Eastern)

08:30 - Speaker: Atlanta Fed Pres. Raphael Bostic.

2:00 p.m. - Beige Book.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DLTR (1.20), THO (1.79)

After the Close: FIVE (.83), MDB (.66), PVH (2.24)

At the time of publication, Guilfoyle was long WFC, CRWD equity.