Tariff Deadline Reset?

Trump appears to set new August date as BRICS nations plot own agenda; also those jobs numbers get harder to swallow ... and let's chart the tricky path for the S&P.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Last week, investors worked around one self-imposed deadline. This week, we thought we'd work around another. That's not exactly so. Coming off of several huge wins over the past few weeks, most notably the passage of the "big, beautiful" bill into law, the Trump administration now has to try to get several international trade deals across the finish line. This Wednesday would have been when the 90-day pause that the president had implemented, after first announcing a series of reciprocal tariffs in April against just about every nation on earth, would run out of time. The idea was to permit trading partners time to negotiate new trade deals, and a few trade partners did.

The U.K., China and Vietnam had all signed either completed trade deals or at least agreements that allowed the process to continue. In recent days, news of India and South Korea being close, but needing a little more time, had made their rounds, while headlines also landed showing that it could be a little tougher for Japan or the E.U. to "get there." On Sunday evening, Pres. Trump and Commerce Secretary Howard Lutnick confirmed to reporters that the administration would likely start sending 12 to 15 letters out as soon as today (Monday) to different trade partners informing them that if a deal is struck by Aug. 1, then tariffs on goods imported from those nations will revert back to the "reciprocal" levels announced back on "Liberation Day."

Earlier on Sunday, Treasury Sec. Scott Bessent made the morning news shows and told viewers that several deals were in the "home stretch." Bessent mentioned on CNN that... "We're going to be very busy over the next 72 hours." Bessent did not push out the president's deadline at that time. With that deadline being pushed out last night, we have to wonder if this means a number of trading partners are that close to a deal, or if this means that too many trading partners are really not that close to deal. US equity index futures are showing some overnight weakness.

Another Brick in the Wall, Part 2

If you don't eat yer meat, you can't have any pudding

How can you have any meat if you don't eat yer meat?

- George Roger Waters (Pink Floyd), 1979

More Tariffs for You?

The annual BRICS summit will conclude this morning from Rio de Janeiro. The acronym contains the first letters of Brazil, Russia, India, China and South Africa and has come to represent emerging market nations with more than 20 countries either openly affiliated or loosely connected. This year's summit, which began on Sunday, was not attended by either Russian Pres. Vladimir Putin for obvious reasons, or Chinese Pres. Xi Jinping. This was the first BRICS summit that Xi has missed since he became mainland China's head of state in 2012. Iran was present and represented by Foreign Minister Abbas Araghchi.

BRICS leaders criticized NATO's decision to increase defense spending to 5% of Gross Domestic Product and the situation on the ground in the Gaza Strip. The BRICS nations also released a 31-page document that condemned "in the strongest terms" recent Ukrainian (Yes, Ukrainian) attacks on Russia. The BRICS nations have also flirted with the idea of creating an alternative to the U.S. dollar as a reserve currency and for international trade, one that might potentially be backed by a hard asset such as gold and not just currency by fiat. Egyptian Pres. Abdel Fattah al-Sisi withdrew, while uncertainty also grows about how involved with the BRICS either Saudi Arabia or the United Arab Emirates want to be.

The U.S. Dollar Index strengthened very early on Monday morning as U.S. equity Index futures remained in the red in response to remarks on social media, made by the U.S. president that threatened an additional tariff on nations aligning themselves with the BRICS nations. Pres. Trump posted, "Any Country aligning themselves with the Anti-American policies of BRICS, will be charged an ADDITIONL 10% Tariff. There will be no exceptions to this policy."

In Other News: Poland Ready to Deploy...

Poland is apparently ready to deploy 5,000 troops to its border with Germany on Monday in an attempt to prevent the return of failed asylum seekers. Obviously, this has the potential to heighten tensions between Warsaw and Berlin, two key NATO players.

Last Week

Interestingly, U.S. stock markets had a strong holiday-shortened week going into Independence Day, while Treasury markets did not. Yields worked their way higher from the start of the week past up to its conclusion, while the S&P 500 and Nasdaq Composite both went out at all-time record high closes.

The above-mentioned trade deal with Vietnam and the passage of the president's all-encompassing tax and spend bill mostly cheered investors, but the murky looking June Jobs report on Thursday put something of a confused spin on how the week would be perceived.

On Employment

They bought stocks. They sold Treasury debt securities. More job creation than had been projected. A high percentage of those jobs came from government hires. That is not part of the organic U.S. economy and does not reflect economic strength. The number of individuals leaving the labor force contrasts with the numbers of part-time workers finding full-time jobs. Those two sudden trends don't seem to fit. Demand for hours worked by employers and wage growth are both slowing. This also cannot be considered positives for growth.

Demographically, there are problems, too. A dramatic improvement in the unemployment rate for adult women with no movement for men? A soaring unemployment rate for ethnic Blacks and African Americans, but not for other racial groups, even other minority groups?

No, June was not a weak month for labor, but no honest or a politically unbiased economist would call June strong. Certain groups have held their ground as others have fallen further behind, which is troubling. Layoffs are not rampant. It does appear though that private sector hiring is getting close to hitting stall speed.

The GDP Game

Last week, the Atlanta Fed revised their Gross Domestic Product Now model for the second quarter down to growth of 2.6% from growth of 2.9% (q/q, SAAR). Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q2 growth now stands at 1.56%, down from 1.72%, while the Cleveland Fed still sees Q2 growth of 1.97%. As I have noted, this estimate has not budged in a number of weeks. The St. Louis Fed also took their estimate for Q2 GDP higher from growth of 1.02% to growth of 1.32%. As readers can see, there is now something remotely close to a consensus view across the regional Federal Reserve Q2 GDP models taking shape. They are all moving in the same (wrong) general direction.

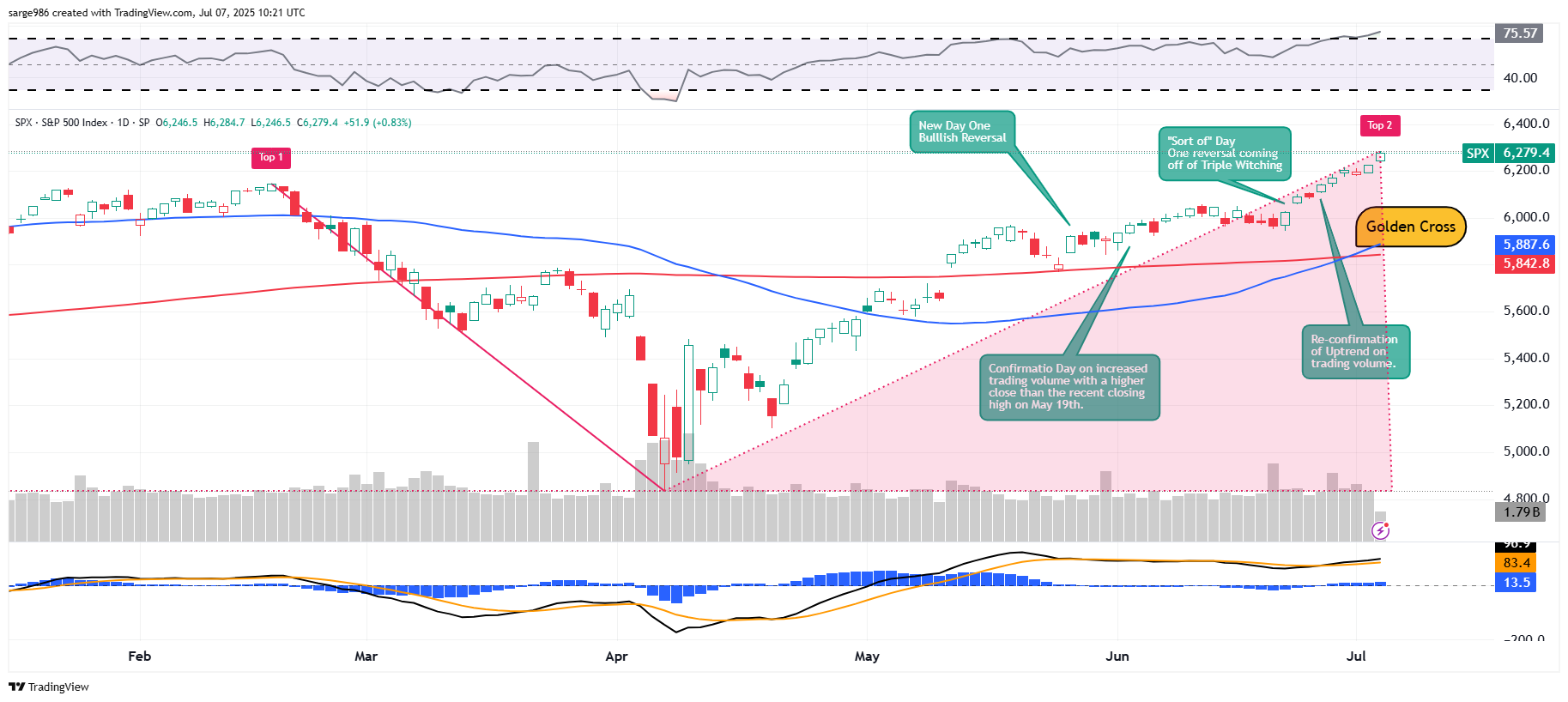

The Chart...

As readers can easily see, the S&P 500 has continued to benefit from last week's "golden cross." That said, the market is not yet out of the woods concerning the threat posed by a potential Double Top pattern of bearish reversal. But one also has to consider that without a sizable "down" day sometime soon that this threat may pass or may have already passed.

Above the chart, readers will see that the reading for Relative Strength now is firmly entrenched in technically overbought territory. Below the chart, readers will see that within the daily Moving Average Convergence Divergence of the S&P 500, the histogram of the 9-day Exponential Moving Average is now well above the zero-bound as are the 12-day and 26-day Exponential Moving Average with the 12-Day line above the 26-day line. This is still an undeniably bullish posture.

What's Ahead?

The week ahead, unless there are trade deal announcements, could be an incredibly quiet week. Second-quarter earnings season kicks off with the big banks toward the end of next week. Until then, scheduled news events will likely be few and far in between.

- The domestic macroeconomic calendar is lighter than a feather this week. The headline event will likely be the auction of $39 billion worth of new U.S. Ten-Year Notes on Wednesday. The U.S. Treasury Department will also auction off $22 billion worth of new Thirty-Year Bonds on Thursday.

- The Federal Reserve will not be extremely visible this week. The FOMC Minutes of the last policy meeting will be published on Wednesday afternoon. There are few Fed speakers on my radar for the week ahead at this time though Fed Gov Christopher Waller, a potential rival to Fed Chair Jerome Powell will speak on Thursday afternoon.

- The earnings calendar is almost non-existent this week. Delta Air Lines DAL and Levi Strauss LEVI will both report on Thursday. There are, however, other corporate events on the docket. Amazon AMZN will launch its now four-day Prime Day event on Tuesday. Look for Walmart WMT, Target TGT, Best Buy BBY, Kohl's KSS, and Macy's M to all try to compete this week with somewhat similar sales events.

Economics

(All Times Eastern)

No significant domestic macroeconomic data scheduled for release.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights

(Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle had no position in any security mentioned.