Taking Stock of Things We Know About the Bear Market

With earnings season kicking off this week, let's look at some things to watch for.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There are a few things we know.

Let’s start with earnings season, which begins in earnest later this week when the banks kick it off. It is highly unlikely any company will give guidance. Why would they? I fully expect to hear and see a lot of ‘We’re suspending guidance for the rest of the year due to uncertainty.’ There is absolutely no incentive for a company to be heroic in this environment. So, if you are expecting any clarity from earnings, I’m not sure you will get it.

What else do we know? We know that in the last two trading days, longs have been taken to the woodshed. And so have shorts. These 3-4% swings intraday are not what leads to confidence in the market. So that becomes less about panic and more about ‘maybe I should sit this one out.’

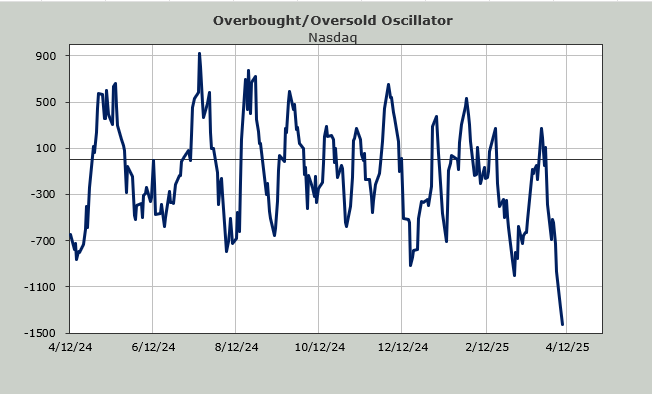

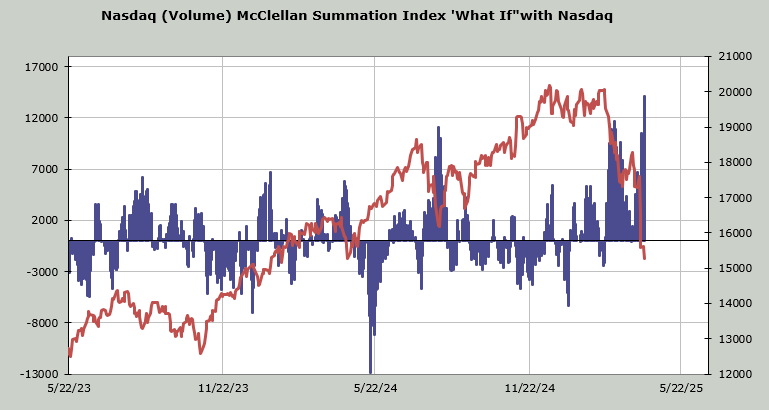

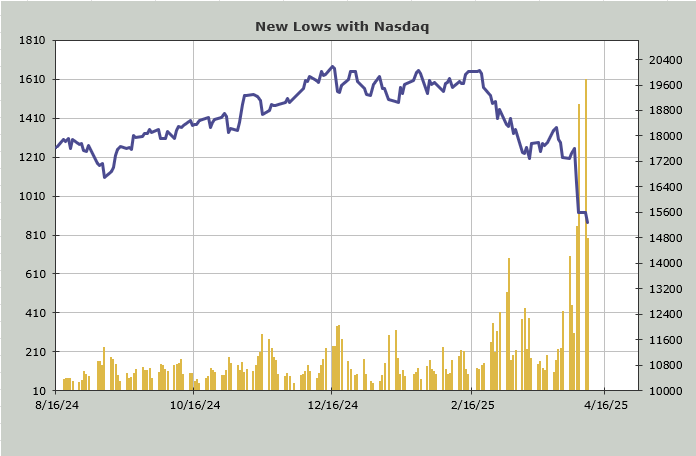

We know that the market is short-term oversold. By almost any measure. Using the McClellan Summation Index and what it will take to turn the direction from the current down to up, we know that since I use volume for this indicator, it now requires a net differential of +14 billion shares. That is massive.

Nasdaq has been averaging about 10 billion shares a day, so it now requires at least two consecutive days where 90% of the volume is on the upside just to get the indicator to stop going down. That’s what makes it oversold.

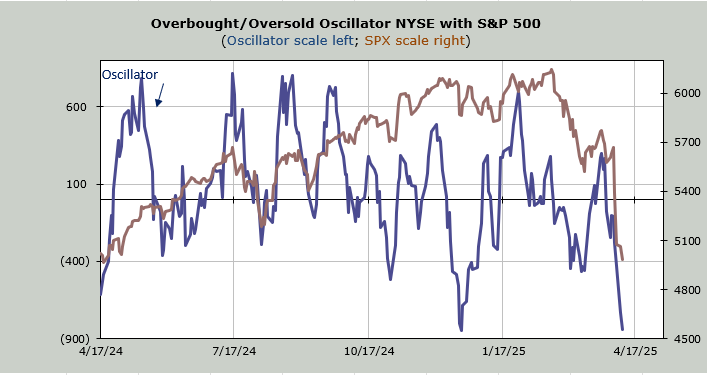

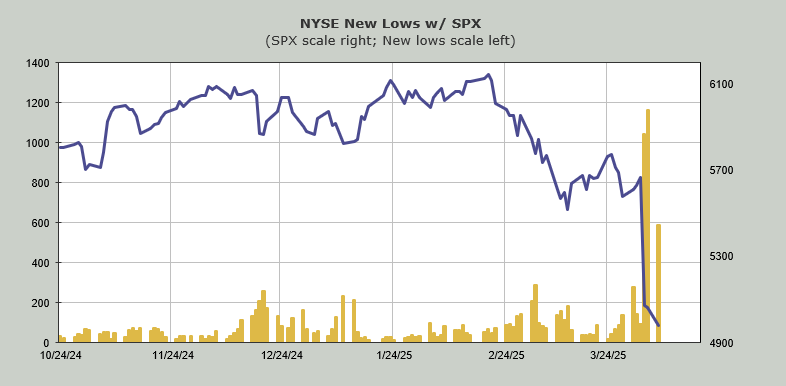

The NYSE’s Summation Index has finally stepped a toe into oversold territory. It now needs a net differential of +4300 (advancers minus decliners on the NYSE). You can see that at +5000, we have rallied over the last two years.

We also know that while the major indexes did not make lower intraday lows on Tuesday, the S&P and the Nasdaq both made lower closing lows. Obviously, much can change with a renewed plunge on Wednesday, but at least on Tuesday, there were far fewer stocks making new lows than we saw on Monday.

The put/call ratio was 1.22 which means we now have four straight days with readings over 1.15. People are finally getting serious about buying puts. That puts the ten-day moving average at 1.05. I suspect it goes higher, but at least it is finally pushing upward.

The ISE call/put ratio, where the mostly small traders play their options, continues to stay over 1.0. There is no fear there whatsoever. Typically, by this point in a decline, the readings would regularly be under 1.0, but now they are buying every dip.

Finally, I am back to watching the chart of the ratio of the SOX to the Nasdaq. It did not make a lower low on Tuesday. It may do so on Wednesday or any other day, but the semis were one of the first groups to start down. So, I watch it for signs of stabilizing on a relative basis because that ought to mean an oversold rally.

I do expect, after an oversold rally, we’ll come back down, but we first need the oversold rally!