'Tactically Bullish'

Monday appears an exhibition game as earnings blitz looms, Scott Bessent makes the rounds, and JP Morgan states ... the obvious.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The regular trading session on Monday was more or less an exhibition game. The day came after a raucous four-day rally and ahead of a four-day release blitz. The release schedule for Tuesday through Friday of this week is simply chock full of key quarterly earnings and high priority macroeconomic data. How much did Monday count? While certainly better than a sharp stick in the eye, not so much in my opinion.

Heck, last Monday, the day of our marketplace's most recent panicked sell-off turned into one of the same market's best weeks in months, so Mondays can be misdirection, or in the case of this particular Monday, non-directional. That doesn't mean that Monday was good for nothing. It just means that in isolation, Monday had more in common with the band that performed ahead of the band that you paid to see than with the creation of headlines that could push markets very far.

One Man Speaks

On a trading day void of overt market-moving catalysts, one man appeared in the media more than once. That man more or less created an early selloff and then created a rally. Kind of funny the way that works out. Treasury Secretary Scott Bessent appeared at CNBC and referred to the trade condition between the U.S. and China as "unsustainable" due to the fact that China exports five times more (in terms of value) worth of goods to the U.S. than goes the other way. Bessent said that it is "up to China" to de-escalate the current tension between the two nations. This pressured asset prices on a morning where there had already been some profit taking.

However, Scott Bessent wasn't quite done. He also appeared at Fox News, where he quipped, "I would guess that India would be one of the first trade deals we would sign."

Bessent added that the U.S. has also held substantial talks with Japan and other Asian nations, while also saying that the president would be "intimately involved" in negotiations with fifteen or more important trade partners. This turned the algorithms that control price discovery around on a day without much more to go on.

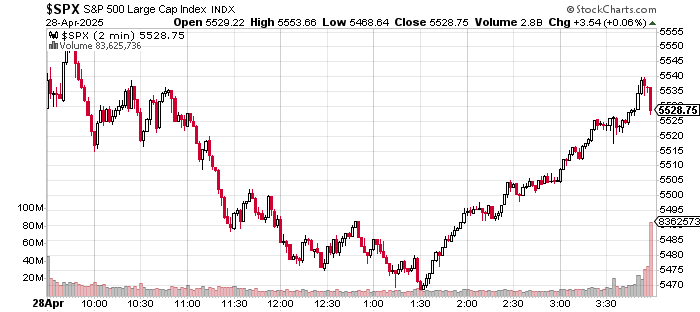

While the major domestic equity indexes closed very close to where they opened, they got there in a roundabout way. This is a two-minute chart of the S&P 500 for Monday's regular hours.

On Chinese Sustainability

Goldman Sachs GS released a report on Monday concerning the trade war between the U.S. and China from the Chinese side, economically. This excerpt, if true regarding Chinese employment, could be telling: "Our estimate suggests that 16 million jobs are involved in the production of goods exported to the U.S., almost one quarter of them in the wholesale and retail sector. Communication equipment, apparel, and chemical product sectors are more vulnerable than other manufacturing sectors due to their high share in U.S.-bound exports from China."

Better Than One Might Think

Overall, U.S. market internals were better than one might think on Monday. Treasury debt securities were strong again, as the yield for the U.S. Ten Year Note dropped to 4.21%. While the S&P 500 gained just 0.06% for the day and the Nasdaq Composite lost 0.1%, the small to mid-cap indexes all gained between 0.35% and 0.41%. The Dow Transports actually outperformed broader markets at +0.47%, as the KBW Banking Index gained 0.44%.

Tech was a little weak, as the shares of Nvidia NVDA reacted poorly to a report that China's Huawei was set to test that company's new AI-capable processors in the absence of imported U.S. chips. But market-wide breadth was very solid.

Winners beat losers at the NYSE by a 5-to-3 margin and by a rough 5 to 4 at the Nasdaq. Advancing volume took a 77.2% share of composite Nasdaq-listed trade and a 71.7% share of composite NYSE-listed activity. This all came on increased aggregate trading volume on a day over day basis, across both NYSE and Nasdaq listings as well as across the membership of the S&P 500.

Additionally, while no S&P sector SPDR ETF closed more than 0.7% away from where it closed on Friday, nine of those 11 funds closed out the Monday session in the green. Energy XLE led the way north followed by the REITs XLRE, while Tech XLK and the Samples XLP closed in the red. There was no pattern of out or under-performance visible across growth, cyclical or defensive sectors.

We Did See...

That support for the S&P 500 showed up exactly where we had said it needed to be in our note twenty-four hours ago.

We'll continue to watch what had been resistance from early April into Friday's attempted breakout from this ascending triangle pattern for continued support. This morning's key earnings as well as the Conference Board's release of their April Consumer Confidence survey at 10 a.m. ET will be key to holding that line.

Party Hats?

Bloomberg News is reporting that JP Morgan's JPM trading desk is turning "tactically bullish" on U.S. equities and is projecting that tailwinds that would include this week's "big tech" earnings and potential trade deal announcements could continue to push equity prices higher. In a research note to clients on Monday, the bank made these points but also covered their tracks, emphasizing that the rally could fade within weeks should the negative impacts of current trade policy start to bite the U.S. economy.

JPM head of global market intelligence Andrew Tyler wrote "Overall, the de-escalation trade has room to run, (but) this is not an all-clear for markets." The note goes on to say, "The combination of light positioning, low liquidity, subdued investor participation means that this market is likely to drift higher in the absence of negative news such as tariff headlines or a spike in bond yields."

Seems like common sense to me. Imagine: If only good things happen and nothing bad happens, markets will go higher. But, and this is a "big but", if bad things happen and good things fade, then the rally will end. Got it. Thanks, Sparky. People actually get paid to say out loud what rookie retail investors easily figured out for themselves a week or two ago. Welcome to Wall Street 2025.

Economics (All Times Eastern)

08:30 - Goods Trade Balance (Mar): Last $147.91B.

08:30 - Wholesale Inventories (Mar-adv): Expecting 0.6% m/m, Last 0.3%, m/m.

08:55 - Redbook (Weekly): Last 7.4% y/y.

09:00 - Case-Shiller HPI (Feb): Expecting 4.7% y/y, Last 4.7% y/y.

09:00 - FHFA HPI (Feb): Expecting 0.3% m/m, Last 0.2% m/m.

10:00 - CB Consumer Confidence (Apr): Expecting 87.9, Last 92.9.

10:00 - JOLTs Job Openings (Mar): Last 7.568M.

10:00 - JOLTs Job Quits (Mar): Last 3.195M.

4:30 p.m. - API Oil Inventories (Weekly): Last -4.565M.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: MO (1.19), AMT (2.39), KO (.72), GM (2.66), HON (2.21), PYPL (1.16), PFE (.69), SPOT (2.21)

After the Close: QRVO (1.00), SNAP (.04), SBUX (.49), V (2.68)

At the time of publication, Guilfoyle was long JPM equity.