Surveying a Wild Week, China Trade Latest, Who Loses Jobs First to AI

Let's look at who won and lost in the banking industry, mixed messages on the chart, news for Micron, the tariff battle and who's competing with AI for work.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Born to Be Wild

I like smoke and lightnin'

Heavy metal thunder

Racing with the wind

And the feeling that I'm under

Yeah, darlin' gonna make it happen

Take the world in a love embrace

Fire all of your guns at once

And explode into space

- Mars Bonfire (Steppenwolf), 1968

Tracking Mayhem

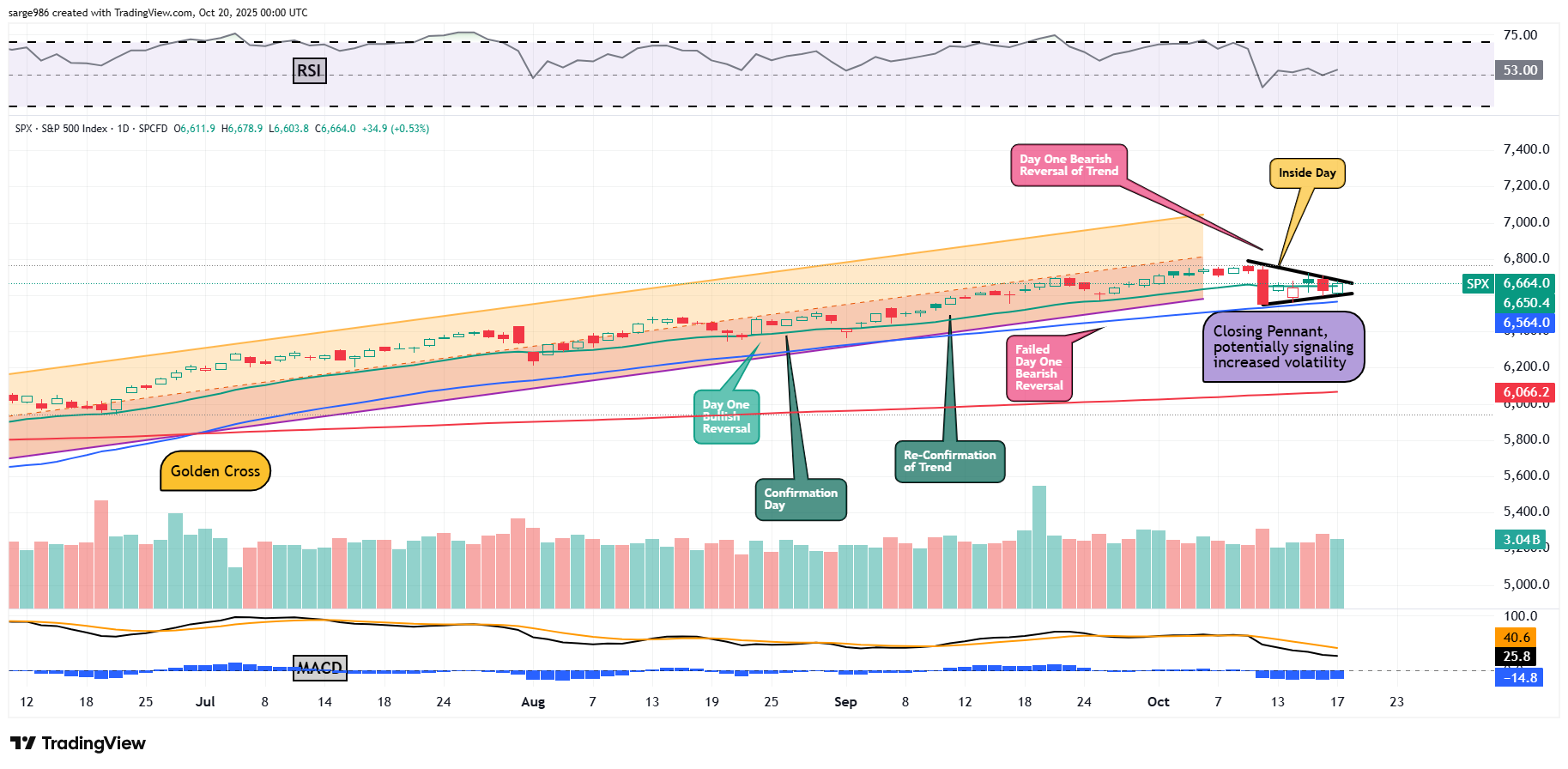

Equity markets sold off rather severely on Friday, Oct. 10. Last Monday, Oct, 13, equities rallied, taking back some of that lost ground. Some readers may recall that I pointed out in this column on Oct. 14, that the day before had been what we refer to as an "Inside Day," which is a one-day pattern that often signals a short-term reduction in volatility. Well, we certainly did have some give and take over the balance of the week. The S&P 500 has not moved in the same direction two days in a row since Oct. 9 and 10.

That said, volatility did subside. Financial markets were hit with a significant level of risky headline level events for the week, yet most of your mid-major to major U.S. equity indexes still managed to post decisive gains over the five days session. Just as interestingly, after the Inside Day on Monday, the S&P 500 made multiple lower highs and multiple higher lows going into the weekend. Out of the woods, Sarge? Don't be silly. More like back to "square one."

Looking Back

It was a wild week on Wall Street. Traders and investors had to deal with ever-changing headlines regarding the condition of trade between the U.S. and China. Earnings season kicked off with a bevy of reports issued by the nation's largest money-center and regional banks. The winner for the third quarter so far appears to be a Sarge-folio name, Wells Fargo (WFC) . However, the big banks were not the problem.

On Thursday, regional banks put a scare into investors. Both Zions Bancorporation (ZION) and Western Alliance (WAL) revealed issues with troubled loans and that created jitters that ran through the entire marketplace well beyond the financials. JP Morgan Chase (JPM) CEO Jamie Dimon rattled a few cages in hindsight as market pundits, including yours truly, cited his "cockroaches" comment.

Other News

Other stocks making headlines included Micron Technologies (MU) , another name of mine, after Reuters had reported that the memory chip designer was planning to abandon the Chinese market after failing to have ever recovered from Beijing's 2023 ban on its server chips. Mainland China had accounted for 12% of Micron's revenue generation.

Additionally, Nebius Group (NBIS) introduced its latest AI cloud product, Nebius Cloud 3.0 or "Aether." This offering apparently delivers features that allow for businesses and organizations to run their most critical AI workloads in a trusted environment and at scale. Regardless, the stock gave up 7.8% on Friday and 12.5% for the week but is still up 1% for October and 520% from its April 2025 low.

On China

Late Friday, U.S. Treasury Sec. Scott Bessent said that he will meet this week with Chinese Vice premier He Lifeng and see what he can do about de-escalating measures on both sides as Beijing and Washington have each acted in pursuit of leverage over the past more than a week, ahead of the planned meeting between President Trump in late October in South Korea with his Chinese counterpart, Xi Jinping. Remember, on Friday, in an interview with Maria Bartiromo at Fox Business, President Trump admitted that he did not see his latest tariffs on China as "sustainable," and that he does expect a "fair deal."

Some may have missed this one. On Thursday, Jefferies strategist Christopher Wood, in his report "Greed & Fear" wrote that Pres. Trump's recent tariffs are more a negotiatory tactic than a point of conviction. Wood says that Beijing could agree to making some key concessions if Washington were to take a less staunch or even publicly disavow support for Taiwanese independence. Wood thinks this would cost the U.S. little politically. On that, I am not so sure. Something like that may just cost the U.S. some valuable allies in the region who don't have the best relationship with Beijing themselves.

In any case, Wood's base case for the meeting in South Korea is some kind of partial trade deal that at least extends the current condition if not an improved condition of trade between the two powers. and perhaps removes the stigma among U.S.-based fund managers associated with investing in China. I honestly can't tell you what year I last held a Chinese-based stock in any of my main portfolios.

The Week That Was...

What the mid-major to major U.S. equity indexes did last week, as stocks did the hokey pokey and they turned themselves around...

- The S&P 500 gained 0.53% on Friday and 1.7% for the week.

- The Nasdaq Composite gained 0.52% on Friday and 2.14% for the week.

- The Nasdaq 100 added 0.65% on Friday and 2.46% for the week.

- The Russell 2000 surrendered 0.6% on Friday but still gained 2.4% for the week.

- The S&P Smallcap 600 gave up 0.12% on Friday but added 2.98% for the week.

- The S&P Midcap 400 gained 0.23% on Friday and 1.96% for the week.

- The Dow Transports added just 0.13% on Friday and an impressive 4.04% for the week.

- The Philly Semis lost 0.32 on Friday, but "soared 5.78% for the week.

- The KBW Bank Index gained 0.55% on Friday and 0.98% for the week.

On Friday, nine of the 11 S&P sector SPDR ETFs closed out the session in the green, led higher by the Staples (XLP) and the Discretionaries (XLY) . The Utilities (XLU) led the losers in the wrong direction.

For the week, all 11 S&P sector SPDR ETFs traded higher with the REITs (XLRE) out in front, Followed by the Discretionaries and Technology (XLK) . There was no real discernable pattern of leadership across cyclicals, defensives or growth-type sectors.

The Chart...

We have already discussed the "Inside Day" this past Monday that signaled a short-term decrease in volatility. We have now enjoyed that short period of lower highs coupled with higher lows. This, as short as it is, looks like a Closing Pennant pattern to me. What does a closing pennant signal? You in the back.. That's right, increased volatility. Good job. What does a closing pennant not signal? You again... That's right. Direction. Closing pennants can often signal explosive volatility but do not signal direction. What does that mean? Be ready. I know you always are but be ready.

Readers will note that Relative Strength for the S&P 500 is fluttering around neutral territory not signaling strength not weakness. However, below the chart, the daily Moving Average Convergence Divergence looks considerably less friendly. The histogram for the nine-day exponential moving average has crossed below the zero-bound and remained there. That's probably short-term bearish. The 12-day exponential moving average has crossed below the 26-day EMA and also remained there. These are both short to medium-term bearish signals. However, both the 12-day and 26-day EMAs remain above the zero-bound. That's a medium-term bullish signal. Mixed messages? Precisely.

Earnings

According to FactSet, for the third quarter, with 12% of the S&P 500 having reported, 86% of those companies have surprised to the upside on earnings while 84% of those companies have surprised to the upside on revenue generation. The fast start to earnings season and increased guidance in general, has boosted third-quarter earnings growth expectations for the S&P 500 to 8.5% from just 8% a week ago. Revenue growth expectations now stand at 6.6%. up from 6.3%. For the full calendar year of 2025, Wall Street now sees S&P 500 earnings growth at 11%, up from 10.9% on revenue growth of 6.2%, up from 6.1%.

Back to the quarter, Technology, the Financials and Utilities are expected to be the outperformers with projected earning growth of 17% or more. Financials are new here as last week, realized and expected growth for the sector improved from 13.2% all the way to 18.2%. Wow! Four sectors are still projected to suffer a year-over-year earnings contraction led to the downside by Energy. Over the past two weeks, the Health Care sector saw consensus for its y/y earnings growth for the quarter fall from +0.1% to -1.7% to the present -4.6%. Talk about sinking like a rock.

Valuation

Still using data provided by FactSet, and aided by improved forward looking guidance, the S&P 500 ended last week trading at 22.4- times 12 months' forward-looking earnings, down from 22.8-times a week ago. This is still well above the five-year average of 19.9-times for the index as well as its ten-year average of 18.6 times. The S&P 500 also ended last week trading at 28.4-times trailing 12 months' earnings, down sharply from 28.9-times a week ago. That also stands well above the five-year (25 times) and ten-year (22.8 times) averages for the index.

Ten of the 11 sectors are now trading above their five-year average valuations, led by Tech (30.1-times) and Consumer Discretionaries (28.3-times). Only the REITs (17.1-times) are not historically overvalued relative to their five-year averages.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the third quarter growth up to 3.9% (q/q, SAAR), up from 3.8% despite a lack of reported macroeconomic data. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth stands unrevised from a week ago at 2.34%. The Cleveland Fed's model for the third quarter also remained unrevised at growth of 1.99%. Lastly, the St. Louis Fed model too was left unrevised at growth of 0.42%.

There remains nothing close to a Fed consensus on just how robust economic activity was during the third quarter. It appears that as we expected in this column, that the regional Fed districts that run these models are close to halting the regular updating of said models.

Fed Funds Futures

Fed Funds futures trading in Chicago are now pricing in a 99% probability for a quarter-percentage point rate cut on Oct. 29 and a 94% likelihood for another 25-percentage point cut on December 10. Those probabilities are up from 97% and 88% a week ago. At present, there are now three-quarter points worth of additional rate cuts fully priced in (65% chance, up from 52% a week ago) for all of calendar 2026.

For Whom AI's Bell Tolls

Show of hands... How many of you read the 54-page paper authored by Sayed M. Hosseini and Guy Lichtinger who are Department of Economics doctoral students at Harvard? Not too many, huh? The paper, titled "Generative AI as Seniority-Based Technological Change: Evidence from US Resume and Job Posting Data" is available for free at the SSRN (Social Science Research Network) website. Now, I am not going to reprint their entire piece for you, but I want to excerpt their conclusion for you. Might just scare the heck out of you, especially if your children are in college and not in trade school.

This is from the revised publication dated Oct. 13. The first edition was published in late August:

"This paper provides early, large-scale evidence that the diffusion of GenAI since 2023 is associated with seniority-biased employment effects within firms."

Skipping a few lines, we get to: "We document that GenAI adoption coincides with a pronounced decline in junior employment, while senior employment remains unchanged. Difference-in-differences, triple-difference, and staggered event-study estimates consistently point to this pattern. The decline in junior employment is concentrated in occupations highly exposed to GenAI, with low-exposure occupations showing no comparable change."

Finally, we get to: "The evidence suggests that GenAI adoption may be shifting work away from entry-level tasks, potentially narrowing the bottom rungs of internal career ladders. Because early-career jobs play a central role in skill development and life time wage growth, such shifts could have lasting implications for inequality and mobility. These patterns raise several important questions for future research. Understanding whether the observed adjustments persist, and how firms and workers adapt through training, task design, or career development, remains an open and important area for further study."

Is the advent of generative or especially agentic AI the beginning of the end for entry-level, learn the ropes, white-collar corporate culture? The end of professional mentoring? Ultimately, the end for senior-level white collar work as well? At least for some lines of work, I think it is a certainty. The only reason in my opinion, that junior positions are being impacted first, is that senior managers are being asked to reduce overhead. They will protect themselves for as long as they can.

The bell will toll for all though. Senior level white collar labor may outlast junior level white collar labor, but not by much in geological time. The C-Suite will figure out soon enough that they can pay a middle manager a lot less to take on a senior manager's responsibilities if you just don't fire them. They'll do more and say, "thank you." I saw it on the trading floor when algorithms replaced humans and gutted the junior ranks first. Improvise. Adapt. Overcome. There will be no choice.

On The Docket...

Without a lot of macroeconomic data to go on with the government shutdown now in its 20th day, investors and traders have had to focus on corporate earnings and Fed speakers almost entirely as catalysts and for guidance on where to go with the flow of capital. The Fed is now in their pre policy meeting media blackout period, so we'll lose that as well.

... The Federal Open Market Committee will release its next policy statement a week from this Wednesday. The group has gone into their media blackout period, meaning that we will not hear from anyone on the committee until Fed Chair Jerome Powell's press conference following that statement. I usually look forward to these periods as I do feel that our central bankers have way too much to say. However, with any macroeconomic data-points to lean on, this week, I think we could have used some spoken words here or there.

.... As far as the macroeconomic calendar is concerned, again, due to the shutdown, we won't have a lot to look at. that said the Bureau of Labor Statistics is going to get its September consumer price index report published this Friday so that our central bankers will at least have that data when they make their policy decision on Oct. 29.

..... The earnings calendar will be fairly hot and heavy this week. Starting on Tuesday morning, 3M (MMM) , Coca Cola (KO) , GE Aerospace (GE) , General Motors (GM) ), Lockheed Martin (LMT) Northrop Grumman (NOC) and RTX (RTX) will all go to the tape with their third quarter numbers. They will be followed on Tuesday evening by Netflix (NFLX) and Texas Instruments (TXN) . AT&T (T) will bat lead-off on Wednesday morning alongside GE Vernova (GEV) . On Wednesday afternoon, investors will hear from IBM (IBM), Lam Research (LRCX) , and Tesla (TSLA) . Looking out to Thursday, numbers are due from Freeport McMoRan (FCX) , Honeywell (HON) , Union Pacific (UNP) , Ford Motor (F) and Intel (INTC) . Finally, on Friday morning, General Dynamics (GD) , HCA Healthcare (HCA) and Procter & Gamble (PG) will go to the tape.

Economics

(All Times Eastern)

10:00 - CB Leading Indicators (Sep): Expecting 0.1% m/m, Last -0.5% m/m.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (CLF) (-.45)

After the Close: (STLD) (2.63), ZION (1.39)

At the time of publication, Guilfoyle was long WFC, JPM, MU, GE, NOC, RTX, GEV, LRCX, TSLA, FCX, F, INTC equity.