Steer Clear of Momentum Names as Market Pain Set to Continue

There are several reasons to remain concerned about the market and rotation is sure to persist.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I had a lot of time on Bloomberg TV on Veterans Day:

- The first segment, macro-focused, starts at the 4:20 mark. There's pain ahead in AI, electricity and production for security or "ProSec," as we label it. It runs until about the 11:30 mark.

- The second segment starts at the 15:15 mark and is primarily focused on the government shutdown ending

- The most interesting part starts at the 22-minute mark where I’m given the privilege and time to discuss Academy Securities in greater detail.

I don’t normally share all of the media I do (I'll be on Bloomberg radio on Monday and TV on Tuesday) but we covered so much ground and got such an opportunity to discuss Academy, that I wanted to share.

Concerns for the Market

Last week, we questioned the stock market surge on Monday and proved to be correct as, on the week, the Nasdaq 100 index fell slightly. It was a sizeable reversal and I think many of the concerns I have, will continue to weigh on the market.

Bitcoin

Whether it is leading the market or just going along with the “momentum” stocks, crypto had a tough week, with Bitcoin dropping from $104,000 last Friday to $94,000 this Friday.

It was rebounding a bit this past weekend, and is worth watching as virtually every regulatory and administration headline remains positive, but it cannot seem to rally significantly. I think it is safe to say that everyone keeps an eye on Bitcoin as a barometer for risk assets, especially on weekends, when markets are closed, but the news flow doesn’t stop.

Retail Dip Buying

I remain suspicious that the longs are held by “pros” at this stage as I’ve seen evidence of profit taking by retail.

Having said that, the “retail” favorite names and ETFs had a very volatile week (even more so than the market as a whole) and we did see some inflows into some of the most “beat up” names. Maybe it was retail that led the surge, but it could have also been pro traders getting “cute” and trying to anticipate positive weekend news (the administration has been quick to provide positive headlines, especially over the weekend and on Monday morning, when stocks stumble).

We will see what happens, but I think the almost 1% late-day fade off of the highs is telling. Of late, dip buying isn’t always providing instant gratification.

Volatility

VIX inched higher on the week, while realized stock market volatility rose rather aggressively. The MOVE Index (a measure of bond market volatility) rose more rapidly than the VIX. Higher overall volatility can force some “risk parity” strategies to de-risk. Any shift in correlations between major asset classes can cause them to reduce as well. This could be happening already, but I doubt it has been meaningful.

Another week like the past week (especially if the net result is more to the downside) could cause real de-risking.

Bonds and the Fed

The probability of a Fed cut has moved from over 60% to “only” 43% according to Bloomberg’s WIRP function. Now that the probability has dropped below 50%, the Fed may lean toward not cutting, since the market isn’t “forcing” their hand.

The 10-year rose from 4.10% to close out the week at 4.14%, though it briefly got to 4.05% on Friday morning (around the timing of OPEX). I continue to expect more downside for treasuries with the 10-year yield to approach 4.3%. That will weigh on stocks if it turns out to be correct.

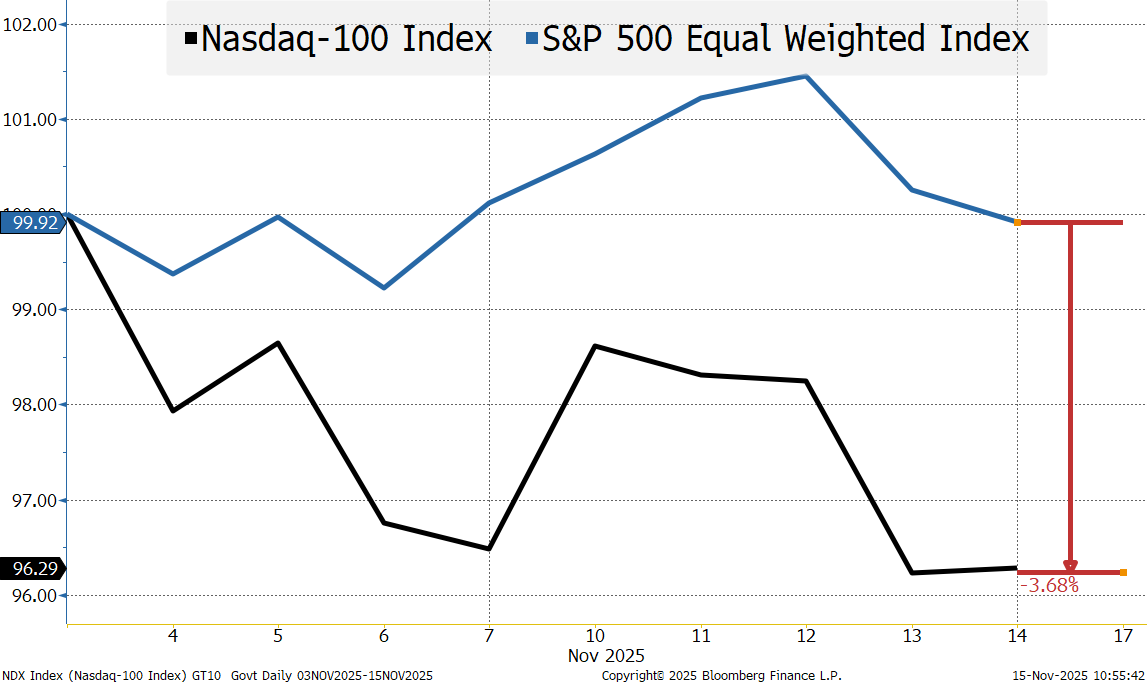

Rotation

There is certainly a rotation trade and I think it will continue to work.

For this trade, I like the S&P 500 equal weight versus the Nasdaq 100. In the past year, (QQQ) (a Nasdaq 100 ETF), is up about 20% while (RSP) (an S&P 500 equal-weight ETF) is up only 4.5%. There is room for significant outperformance on this relative value trade.

Bottom Line

We're sticking to our ProSec themes. See any of our recent reports at Academy Macro.

Look for the “rotation” to continue.

Also, I think the pain continues. The Nasdaq 100 is down on the month and the issues facing it (discussed above and detailed last weekend), have not been resolved. If anything, the big move on Monday and then the fierce dip buying on Friday may well have left a lot of short-term “trading” longs exposed to a further pullback.

I don’t like treasuries (targeting at least 4.25% on 10s).

We continue to think credit spreads will remain under a bit of pressure. Nothing major, but a combination of “surprise” hiccups in private credit, increasing concerns about the state of the lower income consumer (delinquencies) and the trillions of debt needed to support AI, data centers and the required energy buildout.

This is a “normal” or even “run of the mill” adjustment to valuations, current conditions and various outlooks. Certainly not alarming, but not yet time to fully reload into the momentum names.