Speculation and Giddiness Left Us With a Go-Nowhere S&P

If you look at what's underpinning the S&P 500, many stocks are performing poorly. Let's go back to see how we ended up here.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

NYSE Trader

NYSE Trader

Let’s go back six months to when this began. By this, I mean the S&P churning into a go-nowhere index.

Back in September, we had what I compared at the time to SPAC-mania. We had the quantum stocks soaring, rocket stocks, AI, crypto, and probably some other garbage flying. It was quite similar to SPAC-mania in early 2021.

But in 2021, all that speculative stuff peaked while the Mag 7 stocks kept cranking along. Then, in late 2021, we saw breadth peak—yes, breadth came back for a few weeks in late 2021 along with the mega cap tech stocks. That was early November. But the market meandered around with a minor upside bias and didn’t head south in earnest until January.

Today’s action looks quite different in the post-speculative phase, but there are some basics that are similar. Speculative moves and Giddiness in sentiment as well. This time, we had the speculation in September/October and the peak giddiness in late October. Back then, two months after the S&P peaked, it was heading south. This time, we are still in the same place we were (on the S&P) six months ago.

All of this sideways action with violent moves under the hood didn’t happen out of nowhere; it is the result of too much speculation and giddiness in the market from months ago.

I see many folks praising the market (meaning the S&P) for holding up so well in the face of all this bad news. I see folks citing the great earnings as a reason for why we are holding up so well. Yet somehow, some way, a majority of stocks are down in the last six to eight weeks. That doesn’t sound like ‘the market’ is holding up so well.

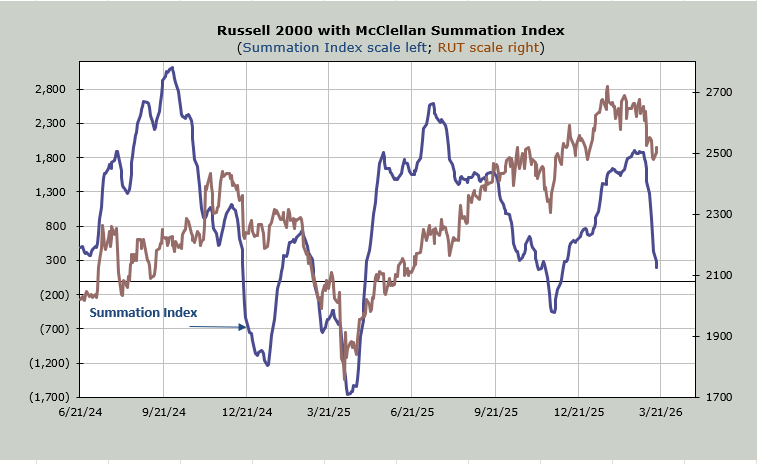

Just look at the McClellan Summation Index, which tells us what the majority of stocks are doing, which in this case is heading down. At this point, it needs a net differential of +1600 advancers minus decliners on the NYSE to halt the decline. We may see it uptick first, but typically when the Summation Index has gotten this close to the zero line, it will eventually cross under it.

I know I have harped away about the banks, but do you realize that while they have rallied for a few days now, the last four trading days have seen them close at the low of the day?

That’s why it makes sense that folks have been buying puts for the last several weeks. The ten-day moving average of the put/call ratio is now at 0.97. The last two trading days, despite the major indexes being in the green, have seen the put/call ratio chime in over 1, something it hasn’t done in this entire move down.

But this feels more like gloom than it does panic. No one is selling furiously, no one is in ‘get me out’ mode. And the biggest change is that the oversold condition thus far has produced such a lethargic rally. The buyers seem to have little or no conviction. The sellers, too.

Maybe the Fed Day will bring us some conviction.

Related: A Two-Day Winning Streak, But This Is the Real Story to Watch