Sentiment Shift: From 'No Thanks' to 'Bull Party' in a Week

Investors’ Intelligence bulls are climbing, AAII bulls jumped, and bears fell hard. It’s not an extreme yet—but sentiment is getting close enough to matter.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It’s once again time to talk sentiment. I know this week has been one giant chop-fest in most indexes, but there have been huge gaps—up and down—as is typical during earnings season.

Let’s take a minute, though, to talk software. It has been my contention for some time now that the stocks ought to begin to diverge from each other, with some acting better and some acting worse. Some will continue in their downtrends while others will begin the long process of base-building.

Just look at the difference between Microsoft (MSFT) and Snowflake (SNOW) . Microsoft made its low nearly two weeks before Snowflake. MSFT rallied over the early March high. SNOW could only make it back to resistance.

My take is that they are sorting themselves out. Some, like MSFT, ought to start the base-building process. SNOW would have to cross that downtrend line for me to believe it wants to begin the process. MSFT still has to cross the downtrend line, but it has put itself in a better position for the time being.

As you go through the software stocks, you should begin to see the different patterns shaping up. They should no longer be ‘all one chart’.

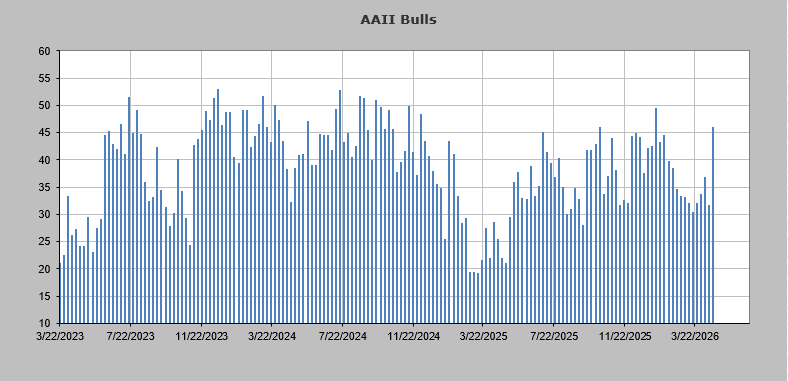

Now, on the sentiment front, we have seen quite a shift this week. Yesterday, I noted the Investors’ Intelligence bulls are now back at 49%, a big climb but not excessive. Last week, I noted the American Association of Individual Investors (AAII) were having none of it; they refused to join the bulls. This week, the bears jumped the fence and joined the bull party in a major way.

The bulls jumped nearly 15 points to 46%, and the bears fell eight points to 34%. That means the bulls are the highest since January, and there are more bulls than bears for the first time since January. They are not extreme, but they are knocking on the door.

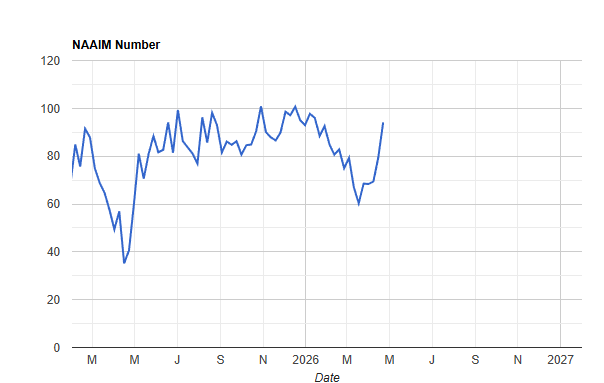

The National Association of Active Investment Managers (NAAIM) who never got that bearish in the decline, only taking their exposure down to 60, has now ratcheted it back up to 94. I consider the 90s to be ‘close’, over 100 (on margin) is excessive.

I always view the options ratios as an early warning sign to what the more intermediate-term sentiment indicators will do. The put/call ratios collapsed this week, with the ten-day moving average of the total put/call ratio sinking to .80 from 1.01. We looked at that chart yesterday.

Now take a look at the equity put/call ratio’s ten-day moving average: it clocked in at .50 yesterday. That is the lowest since the summer of 2023. I take this to mean folks went from incredibly put-heavy to incredibly call-heavy. This has stepped through the door; it is no longer knocking on it.

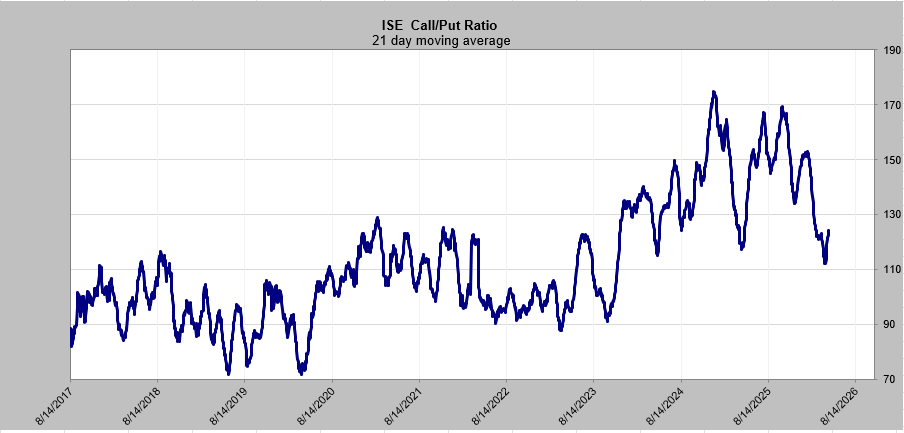

The more intermediate-term 21-day moving average of the ISE call/put ratio has moved up from 1.11 to 1.21, but as you can see, this is not extreme at all. My estimation is that this should be well over 1.30 and possibly over 1.40 in another week or so.

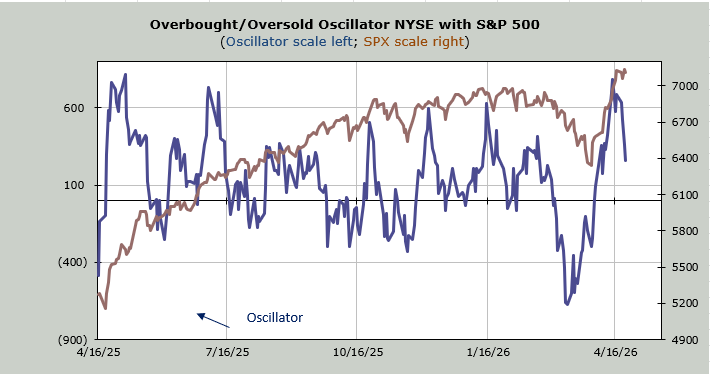

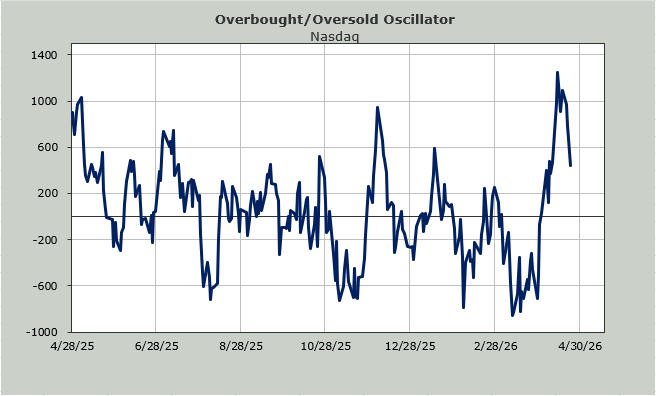

In the meantime, the market has been working off the short-term overbought reading with a giant chop-fest. Well, a giant chop-fest for everything but the semis!

Related: Meta Layoffs, Key Earnings and Conflicting Headlines Spike Volatility