Ruling With an 'Iron' Fist

Trump puts the pedal to the metal with steel and aluminum tariffs, boosting Cleveland-Cliffs, U.S. Steel, Alcoa and others; Also, my favorite stock, Palantir, gets a lift.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I received multiple e-mails as morning melted into afternoon on Super Bowl Sunday. Folks were concerned. Not about the Philadelphia Eagles. Not about the Kansas City Chiefs. No. Financial folks wanted to know if the fact that President Trump was expected to sign new executive orders regarding increased tariffs on Monday would hit our marketplace hard. My response was that I thought this was already priced in, but I could not be sure. Things like this are tricky, but if there were to be profound weakness, I thought that would be the result of algorithmic overshoot rather than careful, thoughtful consideration.

Futures markets were positive overnight coming into Monday morning and there was a risk-on atmosphere around our marketplace that lasted throughout the day's regular session. Equities were strong, but there was some strength seen in the U.S. Dollar Index due to the anticipation that the president would move on implementing reciprocal tariffs on processed, industrial-use metals. This forced some weakness upon treasury debt markets, which allowed yields (interest rates) to rise slightly. The U.S. Ten Year Note paid 4.5% by quitting time on Monday and I see that benchmark instrument yielding as much as 4.52% as we work our way through the zero-dark hours on Tuesday morning.

The president waited until after the closing bells at 11 Wall Street and up at Times Square had made their final audible peal on Monday afternoon. Then, executive hand and pen moved to paper. Orders were issued placing 25% tariffs on all steel and aluminium imports into the United States. All exemptions were cancelled. This impacts trade with suppliers from Canada, Mexico, Brazil and more. The new levies also include finished metals and are meant to crack down on exporters from countries like China and Russia that circumvent duties already in existence by moving their products through third countries before hitting U.S. shores.

President Trump said, "This is the beginning of making America rich again. No exceptions, no nothing." U.S. equity index futures have cooled overnight in response after what was a strong day on Monday. Not the domestic steel / metals stocks though. U.S. Steel X, Cleveland-Cliffs CLF, Steel Dynamics STLD and Alcoa AA all outperformed broader U.S. markets on Monday and have continued to rise in off-hours overnight trade.

Here Comes the Cheese

The day that many traders and investors had looked forward to has arrived. At 10 a.m. this morning, in our nation's capital, a kindly looking, grandfatherly sort of a well-spoken lawyer will take a seat before the Senate Banking Committee. The lawyer, who ultimately became the most powerful economist in both the country and the world, despite a resume that lacks a formal economic background, will offer up his semi-annual Monetary Policy Report and then proceed to answer questions both intelligent in nature and quite inane from those serving on that committee.

The lawyer turned economist is Fed Chair Jerome Powell, a Republican with unusual support that stretches across the aisle in that often-divided town. Powell was nominated to the Federal Reserve's Board of Governors by President Barack Obama, elevated to the Fed Chair by President Donald Trump during that president's first term and then re-nominated to the post by President Joe Biden.

What to expect today? Perhaps less than he will tomorrow morning when he appears before the House Financial Services Committee. Why is that? The Bureau of Labor Statistics will release January data for consumer prices at 8:30 on Wednesday morning. With inflation having potentially trended higher in January, the questions will be different.

I believe that this morning, Powell is likely to stress the central bank's independence from the executive branch of the U.S. government and will likely try to focus more on banking regulation than on the use of short-term interest rates as a tool in the fight against inflation.

Where is Inflation?

Wall Street consensus view for January consumer price index is currently for year-over-year growth of 2.9%, which would be in-line with December's 2.9% print. The Cleveland Fed's model is currently for growth of 2.85%, which would be a slight cooling, while the Hedgeye model, which is something I pay for, shows January inflation rising above 3%.

Interestingly, and perhaps as a warning to all, after inflation bottomed in September and then took off again, January may be another short-term top. Both of these models show a contraction in the pace of rising prices in February that may or may not be temporary.

Fed Funds Futures

As for Fed Funds futures that trade in Chicago, this market shows a 94% probability that Powell's Federal Open Market Committee will leave the target range for the Fed Funds rate at 4.25% to 4.5% when they meet next on March 19. There is a quarter-point rate cut currently priced (62% likelihood) for July 30, and then nothing at all until June of 2026. Will that change? Of course it will, but right now, traders are not placing decisive bets on the short- to medium-term path of interest rates closer to the shorter end of the yield curve.

Manic Monday

The S&P 500 gained 0.67% on Monday as the Nasdaq Composite ran 0.98%. The Dow Transports popped for a gain of 1.03% led north by Uber Technologies UBER, but the small to mid-cap indexes struggled to keep up. The Russell 2000 got by with a gain of 0.36%, but the S&P 600 squeaked by, moving just 0.02% higher. The Philly Semiconductors were hot for the day led by Broadcom AVGO, while the KBW Banks were slapped around on Monday.

Nine of the 11 S&P SPDR ETFs shaded into the green for the session, as Energy XLE gained 2.2%, followed by Tech XLK, which was up 1.5%. The Financials XLF and Health Care XLV were the only two sector SPDRs to close in the red.

Winners beat losers by a 3-to-2 margin at my old stomping grounds (the NYSE), and by roughly 5 to 4 at the Nasdaq. Advancing volume took a commanding 74.2% share of composite Nasdaq-listed trade, and a still impressive 63.7% share of composite NYSE-listed activity.

So, all good in the hood? Yes, and no. While Monday's equity market performance was optimistic in nature, and aggregate trade across those names domiciled at the Nasdaq Market Site was up 23.1% day over day from Friday, that was not the case down on Wall Street. Aggregate trade across both the listings of the New York Stock Exchange and the S&P 500 contracted on a day-over-day basis.

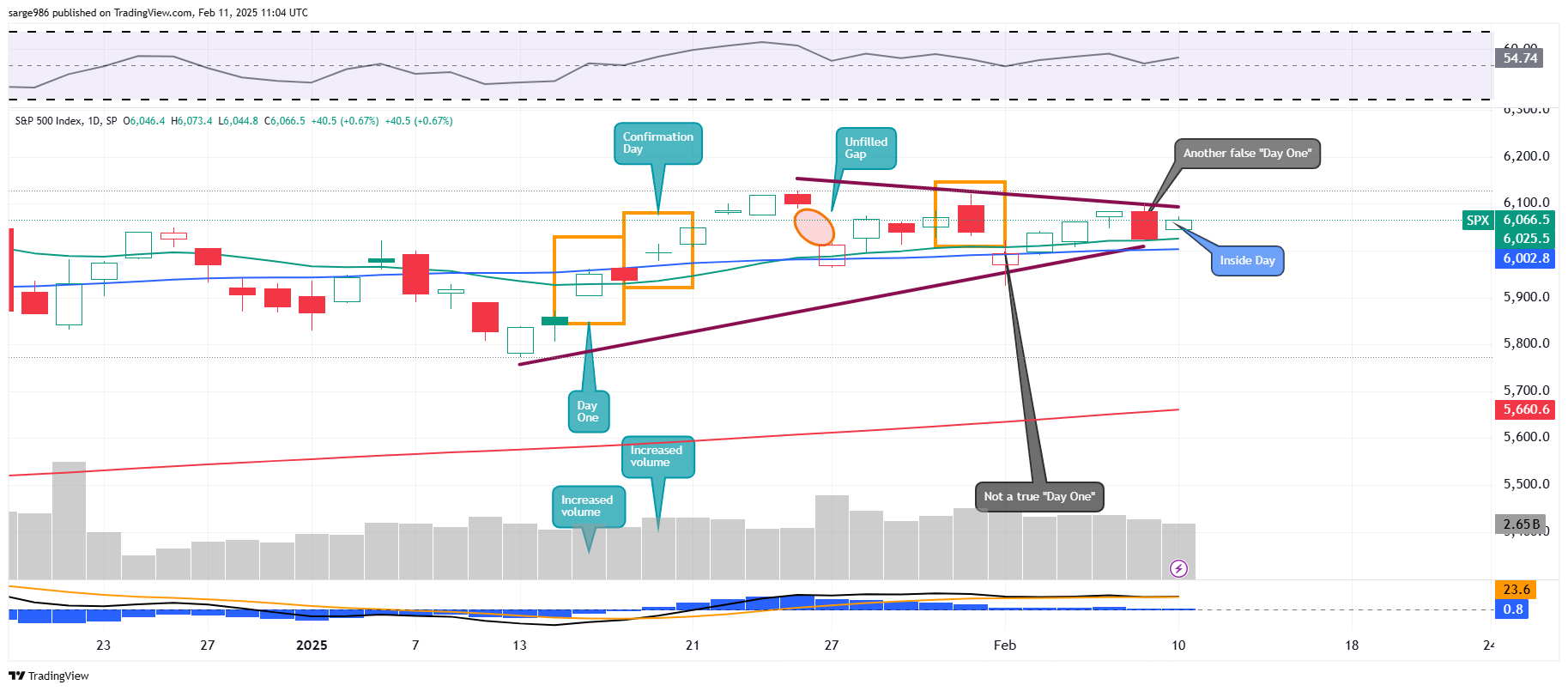

Readers will see that while Monday felt good and your profit / loss ratio may have looked terrific, the S&P 500 put in what's known as an "inside day" on reduced trading volume. This is when the entire range of the daily trading session fits neatly inside of the range of the day prior, while the open and close of the day also fit inside of the open and close of the day prior. What this signals is an expectation for reduced volatility going forward. The decreased trading volume backs that up for now.

Contrary to that indication, however, the pennant formation, in place since mid-January, continues to close. Once closed, it is not uncommon for a violent move to follow. On the bright side, the index has not surrendered either its 21-day exponential moving average, nor its 50-day simple moving average, leading this old trader to believe that both swing traders and portfolio managers are still on board for now.

America's Favorite Stock: Palantir

... Or at least my favorite stock, Palantir Technologies PLTR, was up an additional 5.23% on Monday, closing at $116.65. This came after Dan Ives (5-star sell-side analyst) who has a $120 target price on PLTR wrote on Monday: "We believe Palantir is on the front lines of enterprise AI use cases and the multiplier impact for the rest of tech is the start of a generational $2 trillion of Cap-Ex over the next 3 years for the AI world."

Ives then covered the rest of the AI paying field more broadly, "As more enterprises head down the path of building out AI use cases along with governments, we believe the Street is still underestimating the impact of AI spending for the broader tech world. We believe tech earnings season answered a lot of questions and put DeepSeek agita to rest (for now) although there will continue to be other worries that could come out of left field in this AI buildout."

Remember, that we still have a Wall Street-high target price of $133. Mariana Perez Mora of Bank of America is in second place with a target of $125 and Ives is in third with his target of $120. Pretty much everyone else has been against us. I believe nobody else was even close to being as early as we were as we had this name in the "Stocks Under $10" portfolio with a $6 handle. That's more than an 18-bagger at these prices. Rock & Roll.

Economics (All Times Eastern)

06:00 - NFIB Small Biz Optimism Index (Jan): Expecting 104.6, Last 105.1.

08:55 - Redbook (Weekly): Last 5.7% y/y.

4:30 p.m.- API Oil Inventories (Weekly): Last +5.025M.

The Fed (All Times Eastern)

08:50 - Speaker: Cleveland Fed Pres. Beth Hammack.

10:00 - Speaker: Federal Reserve Chair Jerome Powell.

3:30 p.m. - Speaker: Reserve Board Gov. Michelle Bowman.

3:30 - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: KO (.52), DD (.98), HUM (-2.12), LDOS (2.27), SHOP (.43)

After the Close: DASH (.94), LYFT (.22), SMCI (.63)

At the time of publication, Guilfoyle was long PLTR equity.