Risk And Return Are Related

They say there's no such thing as a free lunch. But that's not quite true for investors. Here's how you can earn a free lunch.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This is the fourth of ten articles in the Filthy Rich Animal Investing Basics Series.

If you like what you see and are not yet subscribed or would like to share with a friend, please visit this link to join us. It's free!

Money for Nothing

Money for nothing. Is that too much to ask for? Dire Straits even wrote a song about it back in the 1980s.

Unfortunately, there's universal agreement that you can't get something for nothing; there is no such thing as a free lunch.

Luckily, the universe is a little bit wrong here. It might be more correct to say there is one free lunch in finance.

A guy even won the 1990 Nobel Prize for proving it with math. His name was Harry Markowitz, and his Modern Portfolio Theory was just a fancy way of saying that if you own a portfolio of different kinds of assets, like stocks and bonds, you can get something for nothing. More accurately, if you diversify your portfolio by owning stocks and bonds, you will increase your returns while decreasing your risk.

To this day, professional portfolio managers reduce risk and increase their returns by building diversified portfolios. And you can, too.

Diversification

At my financial planning and money management firm, I worked closely with a mutual fund company called Dimensional Fund Advisors. There was a saying that Dimensional’s reps often repeated: “Risk and return are related.”

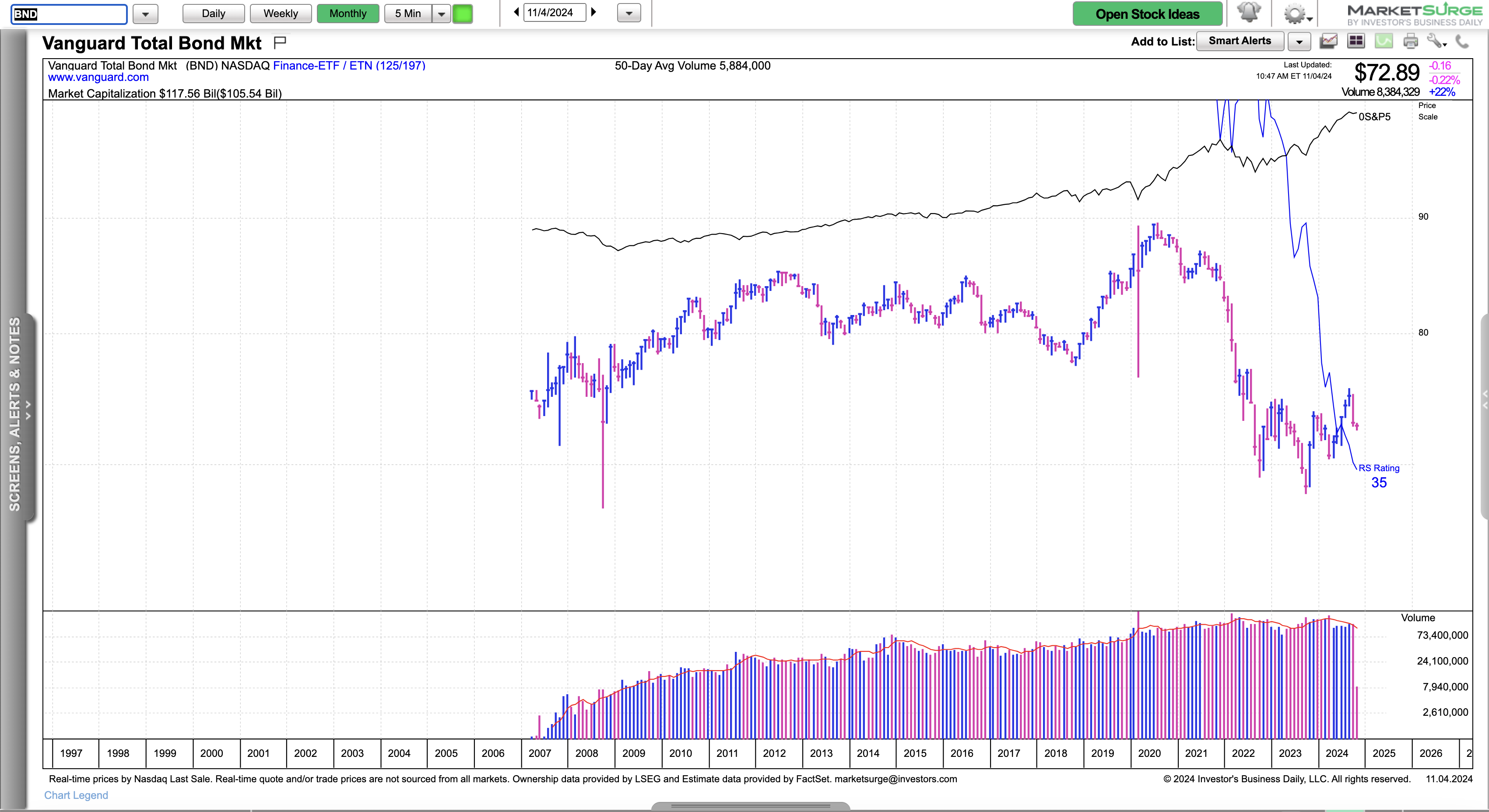

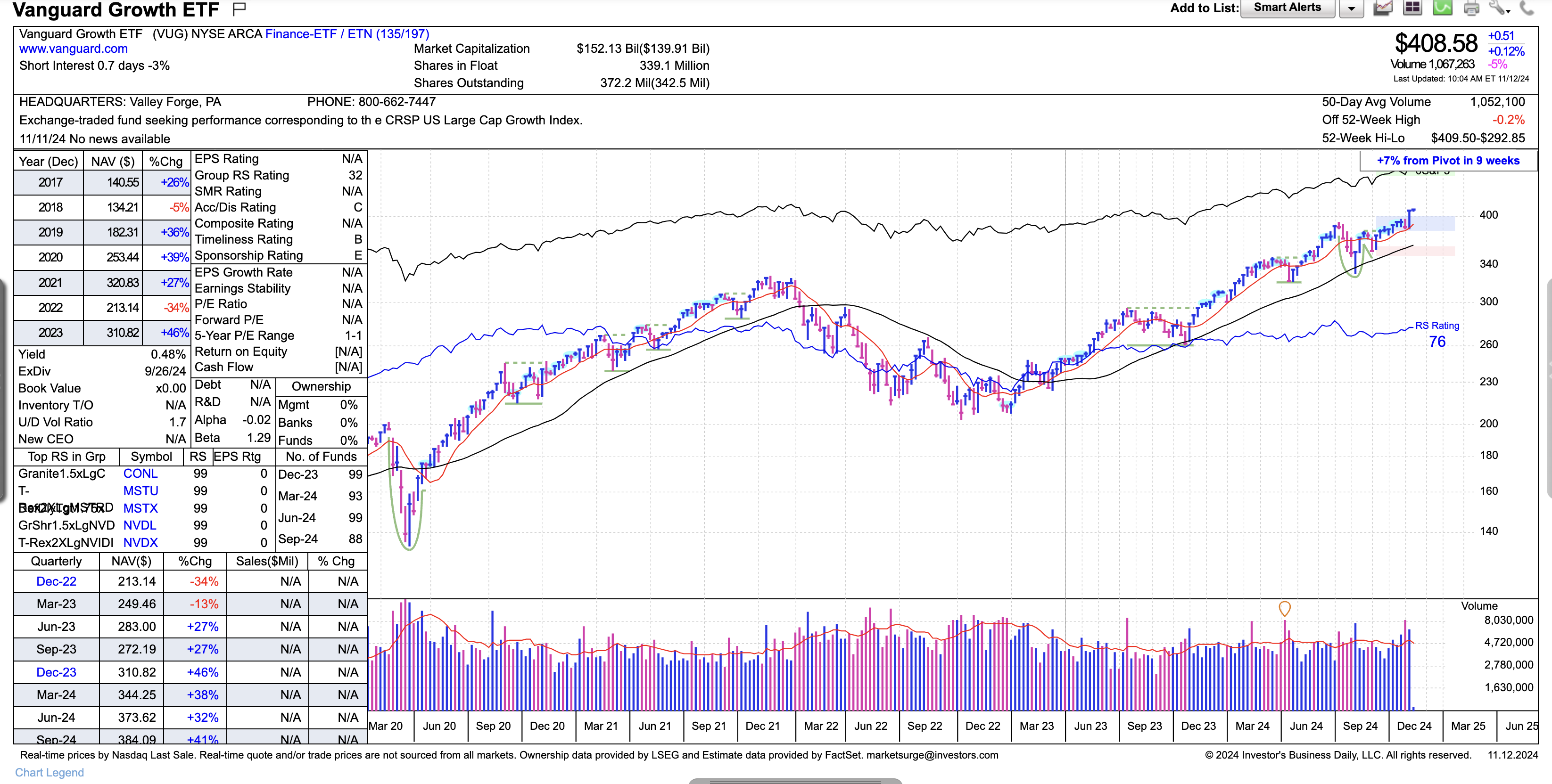

For example, as a general rule, investors get higher returns by taking on higher portfolio risk. That makes intuitive sense. Here are 10-year total returns of two ETFs that can serve as proxies for a high-risk versus a low-risk investment:

- Vanguard Total Bond Market ETF BND: 1.45%

- Vanguard Growth ETF (VUG): 15.27%

Those charts illustrate that a higher return is expected with a higher risk instrument, which in this case means growth stocks.

However, introducing diversification can smooth returns during times of volatility.

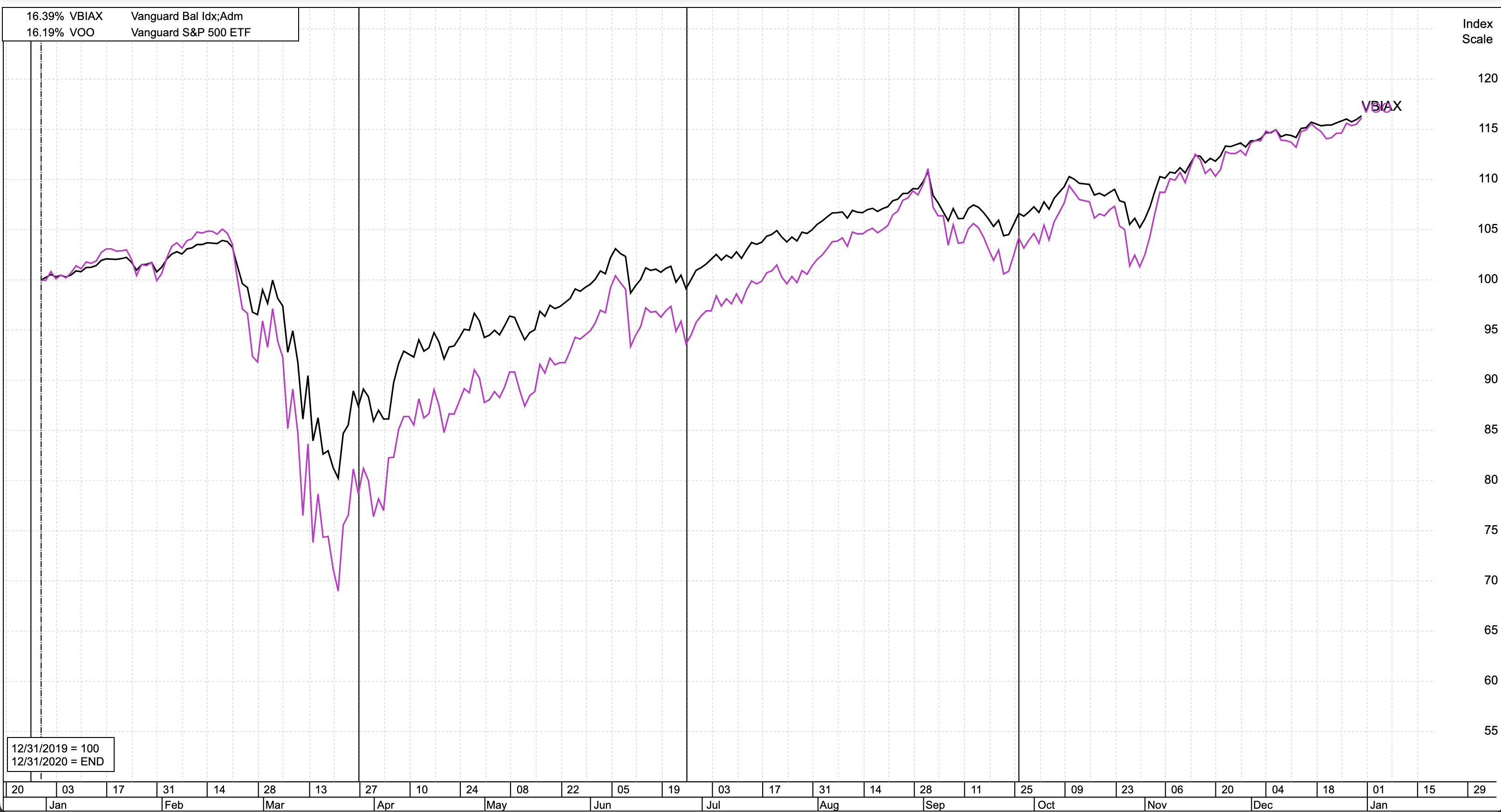

Here’s an example using two more Vanguard funds, showing how they fared in comparison to one another in 2020, when equity markets tanked at the start of the pandemic, but rebounded to finish the year with gains.

This chart compares the Vanguard Balanced Index Admiral Shares (VBIAX) with the Vanguard S&P 500 ETF (VOO). VBIAX is a mutual fund that invests 60% of its assets in stocks and 40% in bonds. That puts it in the category of a diversified portfolio.

I’m cherry-picking the data here, but that’s deliberate: I want to illustrate how a balanced portfolio can and probably will, at specific times, outperform the S&P 500.

In the past 15 years, the S&P has outperformed a balanced portfolio, but this is where the risk calculation comes into play.

While the S&P 500 has delivered strong returns over the past 15 years, its volatility creates challenges for retirement savers.

I’ve had clients ask me if they should just invest in the S&P 500, or even a portfolio of small-cap stocks, since they can have markedly higher returns during certain timeframes.

That answer is no. Investing solely in the S&P 500, or any equity asset class, means exposure to significant market swings, with potential losses that could be devastating just before or during retirement.

Retirement savers generally need stability and predictable income.

A balanced portfolio, combining stocks and bonds, helps cushion against sharp market downturns and offers steadier returns over time.

By diversifying, retirement savers can achieve growth while reducing the risk of major losses that could put their retirement at risk.

What do Risk and Return Really Mean?

People often refer to risk as the “sleep at night factor.” That’s partially true; if you find yourself checking the market throughout the day, that may be a sign your investments are too risky.

However, there’s more to it: Portfolio risk and return represent key measures in investment management.

Return is the profit or loss an investor earns. It combines gains from price appreciation and income like dividends. Investors typically look to higher returns to grow wealth over time.

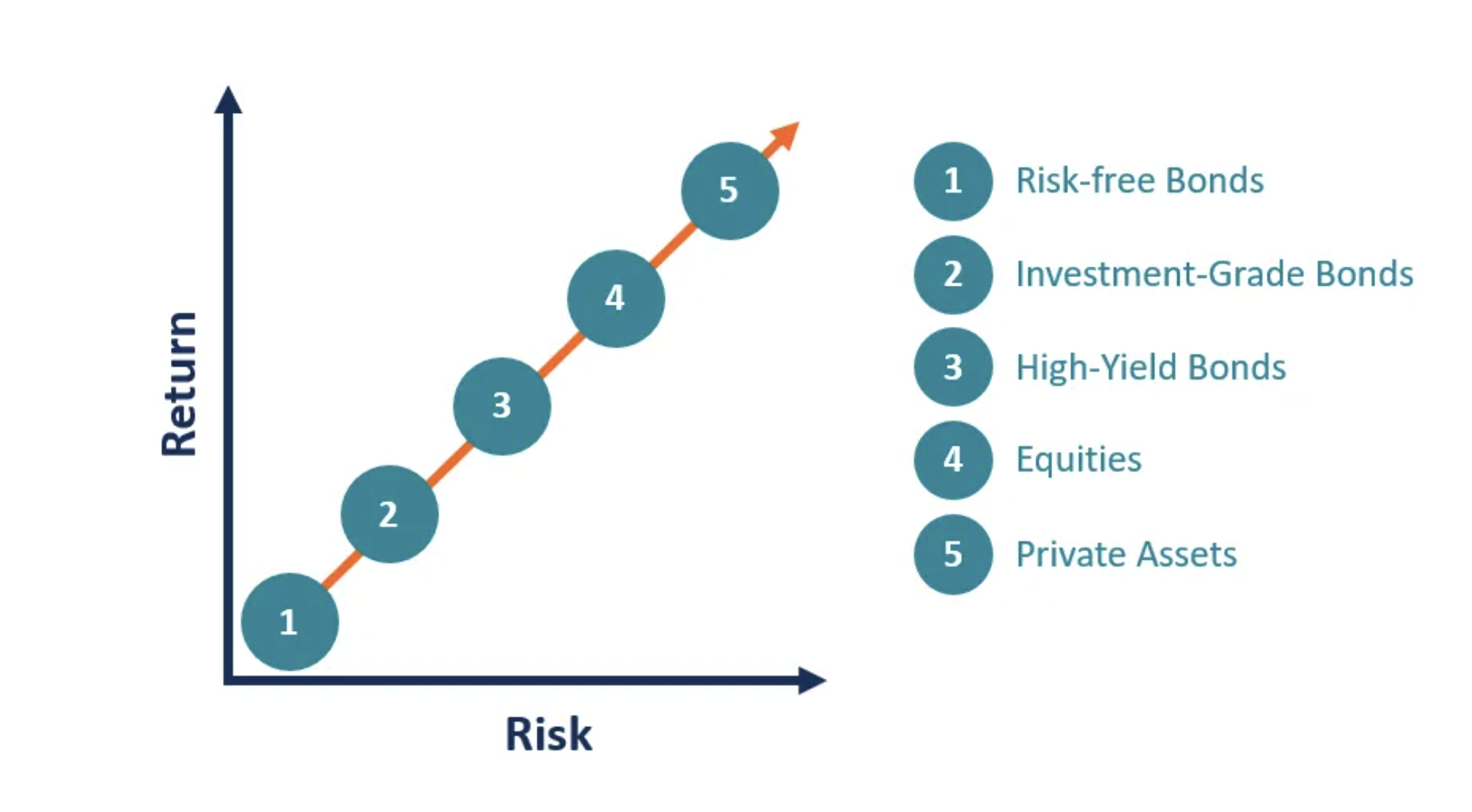

Risk measures the uncertainty or potential for loss in a portfolio, usually calculated by volatility or standard deviation. How much the investment zigs and zags.

Different investments each have their own risk levels; stocks are riskier than bonds. But within those broad categories there are differences. For example, emerging market stocks are riskier than developed market stocks, and long-term bonds are riskier than short-term.

Don’t worry, we won’t get into mathematical formulas here, but a riskier portfolio has greater potential for high returns but also for losses.

It's all about balance.

The goal is to achieve an optimal balance, where expected returns align with an investor's risk tolerance.

That’s the sweet spot where a portfolio generates the income an investor needs, while managing risk, so as not to blow up the portfolio at an inopportune time, such as right before retirement.

But the days of the “widows and orphans” portfolio are long gone. Today’s retirees can’t rely on just bonds for their retirement income. Retirement can last three decades or longer; that means portfolio growth is necessary. And that means taking some risk.

Diversification is a pretty good deal.

Which brings us back to the idea of diversification and the “free lunch” and how that relates to portfolio risk.

Harry Markowitz’s "free lunch" concept highlights how diversification lowers portfolio risk while also generating a retiree’s expected return.

This approach balances growth potential with stability, offering safeguards against market downturns while creating retirement income. For those wanting the “sleep at night” factor, this is a pretty good deal.