Red Meat Prices Must Fall After Hysterical Livestock Rally

The livestock market, particularly feeder and live cattle, has been overwhelmingly bullish. Being a bear is a lonely existence.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The livestock market, particularly feeder and live cattle, has been overwhelmingly bullish.

Being a bear is a lonely existence. It is not lost on me that I’ve completely underestimated the cattle bull (no pun intended), but I’ve yet to see a commodity market survive the reality of high prices curing high prices. Without fail, renewable commodities and even those of the fossil fuel variety have always experienced and eventually succumbed to high prices. Sometimes, it just takes a little longer. I’ll die on this hill; $2.00 live cattle and $3.00 feeder cattle are the livestock version of $10.00 natural gas and $8.00 corn. I discussed this topic on "Cow Guy Close" on RFD-TV last week (click here for the clip).

After Friday’s close, we received the latest “Cattle on Feed” report, a monthly publication issued by the USDA’s National Agricultural Statistics Service (NASS) that provides estimates of the number of cattle being fed for slaughter. It only includes feedlots with a capacity of 1,000 or more, which is sufficient to capture about 85% of all cattle in the U.S. In short, this is an inventory report that tracks cattle in the pipeline, which will ultimately supply grocery stores with beef.

As with any industry or economic report, its mere release stirs up emotions that have the potential to influence trade both before and after the report's release. However, what sets these cattle reports apart is that they are released on a Friday afternoon after the livestock markets are closed, forcing market participants to fret over how the market might react to the news over the weekend. As you can imagine, speculators and hedgers are vulnerable to rash decision-making in exchange for a weekend of peace.

Last week’s hysterical rally was likely driven by those who felt obligated to buy, rather than those who were voluntarily establishing bullish positions. We suspect that many cattle hedgers (ranches who sold futures contracts to lock in what seemed like high prices at the time of the transaction) either opted not to refund their accounts to meet margin calls or were unable to obtain the necessary cash or financing to do so. This created a large, short squeeze going into the Cattle on Feed report as those short futures hedges were bought back.

The latest "Cattle on Feed" report was bullish, but was it bullish from current market prices? Probably not.

The March report showed a decline in cattle inventory relative to both expectations and the previous report, which was released after the close on February 21. Going into the February report, April live cattle futures settled near $194.00 versus Friday’s pre-March report high of $211.00, and April Feeders were at 267.50 versus Friday’s high of $290. Simply, the futures markets rallied 8% between the February and March reports. Thus, buyers at these levels must firmly believe the following report or two will also be bangers. Yet, history suggests otherwise. Supplies are generally the tightest coming out of the winter season; inventory concerns often thaw out with the ground going into spring.

It's hard to be a bear when prices are increasing parabolically, but there are some red flags that I cannot ignore:

- The "Cattle on Feed" report sparking aggressive buying is based on the head of cattle, not weight. Cattle weigh a lot more today than they have in the past, so inventory by weight isn’t all that tight.

- Perhaps speculative buying is driven by exuberant speculation and momentum chasers looking for a place to park hot money. It's not unlike some of the meme stock rallies we’ve witnessed. Cattle, particularly feeder cattle, can be dominated by a small amount of capital due to their lower liquidity relative to markets such as corn and crude oil. For instance, the open interest in feeder cattle futures (across all contract expirations) exceeds 80,000. Previously, the largest position ever held was about 60,000. Feeders have been leading the charge, but that lead might be artificial, driven by speculation rather than fundamental reality. There are now more traders long feeder cattle than ever before, and sentiment readings are extremely bullish. The sad truth is most speculators lose money, and most market analysts are wrong; if everyone is thinking the same thing, there is a good chance that expectation is incorrect.

- High prices always cure high prices. I’ve yet to see an exception. Even a high-protein or keto diet trend will eventually run into consumer price sensitivity. It is hard to buy a pack of red meat at Costco for less than $80.00; this will be difficult to sustain.

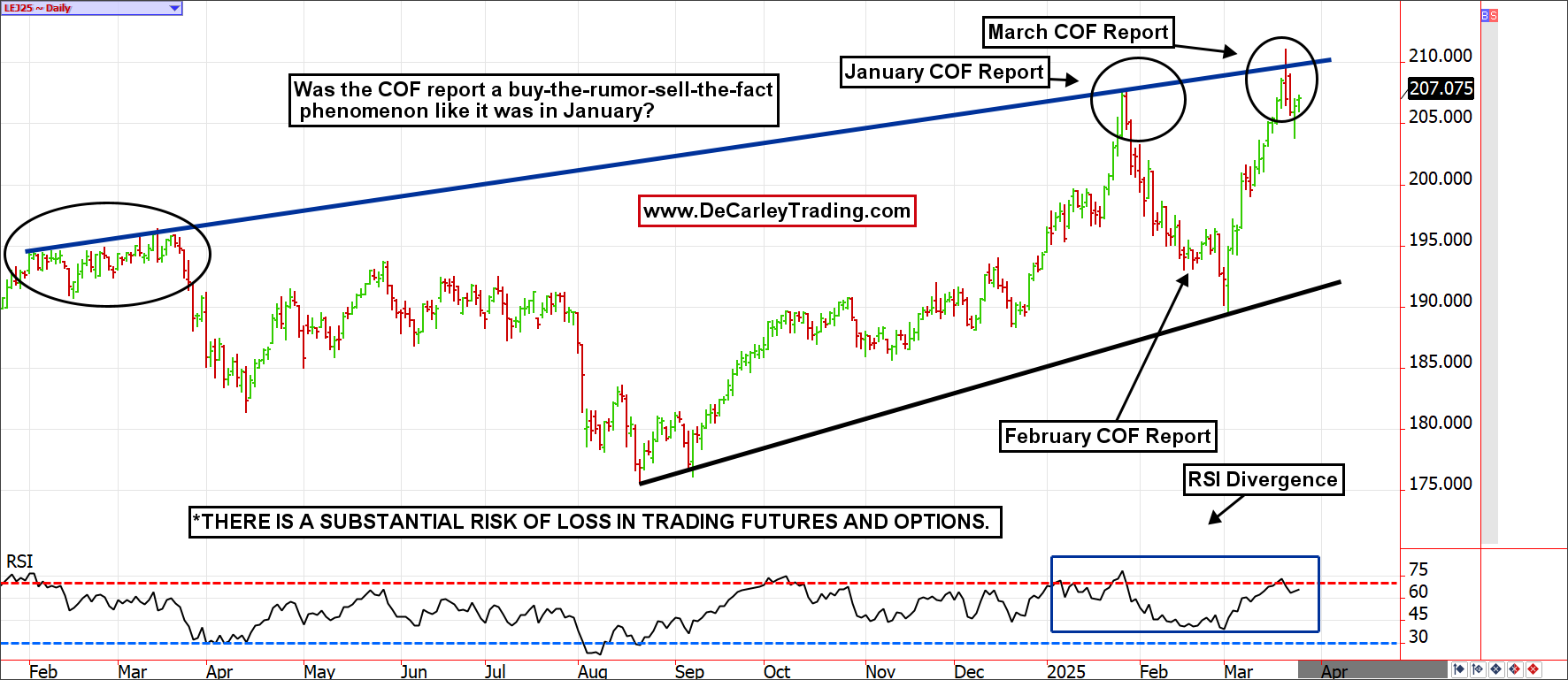

Daily Live Cattle Chart

We appear to be repeating the aftermath of the late January "Cattle on Feed" report. Prices strengthened ahead of the report, effectively pricing in the bullish news before it was even announced. This resulted in buy-the-rumor, sell-the-fact price action. April is typically a seasonally-weak month for cattle, and the livestock markets tend to experience trend reversals at the turn of the month. The stars seem to be aligning for a large correction or maybe even something much more stunning.

Monthly Feeder Cattle

Cattle is the only commodity market that hasn’t given back its 2023 inflation-era rally. Is this the one magical commodity bull market that avoids the inevitable cycle? We doubt it. The monthly chart's RSI suggests that momentum is waning; there is a divergence between the futures price and the RSI, as new highs in the market are accompanied by lower highs in the indicator.

In Summary

It doesn’t feel like it now, but livestock prices and even red meat on our grocery store shelves will meet price inelasticity.

Consumers haven’t changed their habits yet, but historically, they always do. Furthermore, producers are being incentivized to increase production. Cattle reproduction and fattening are not instantaneous or simple processes, but U.S. ranchers know how to get the job done, and they will eventually succeed. An undersupplied market always becomes an oversupplied market. For reference, refer to a five-year chart of orange juice, corn, wheat or natural gas. There is a clear pattern of feast and famine; it is in nobody’s best interest to try to pretend it doesn’t exist.