Realization Week

It's a week where everyone realizes that stocks have been dropping and begin to update their targets accordingly.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It’s exhausting, isn’t it?

We can’t seem to get anything that looks like capitulation. We are using up the oversold condition by churning around the 5600 area on the S&P. Breadth isn’t terrible but it’s not good either. The CPI comes in better than expected, and bonds go down. Stocks barely go up.

But this week feels like a bit of a Realization Week. I know I typically say it’s a Realization Day because there is often a day where everyone sort of realizes some asset has been going up or down when that asset has been going up or down for weeks or months already.

This week feels like the week folks finally understood that there is a slowing in the economy. This is the week some Wall Street firms took their targets for the S&P down. This is the week some Wall Street firms took their earnings estimates and GDP numbers down. It is also the week we started to see some companies pre-announce earnings.

It started with Delta earlier this week (and the stock still hasn’t stabilized). Wednesday saw some comments from a few CEOs. For example, Mr. Dimon at JP Morgan said they are seeing the consumer pull back. Colgate said they, too, are seeing a hesitant consumer. And the layoff announcements have picked up as well. There are others, but my point is we didn’t see much of this last week; it began in earnest this week.

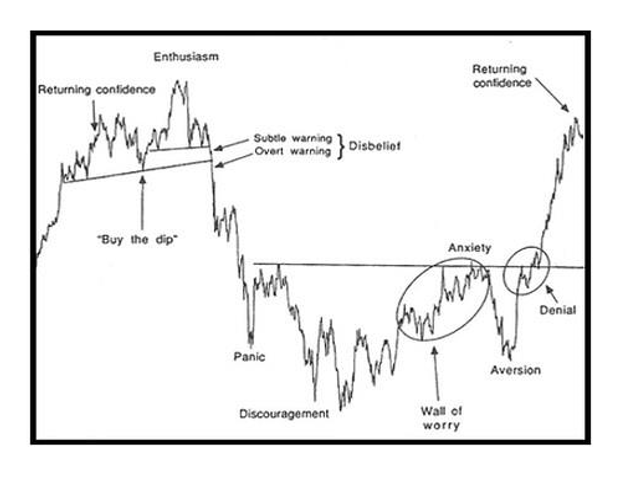

Where would that put us on the Sentiment Cycle my mentor Justin Mamis developed decades ago? My guess is we’re probably just to the right of Buy the Dip, although some stocks are further along (have you seen the Transports at a new low?).

But you see, this is actually good news in some fashion. When we were in the chop zone, we were still up there, just over subtle warning/disbelief, so we’ve come down from there. It’s a journey.

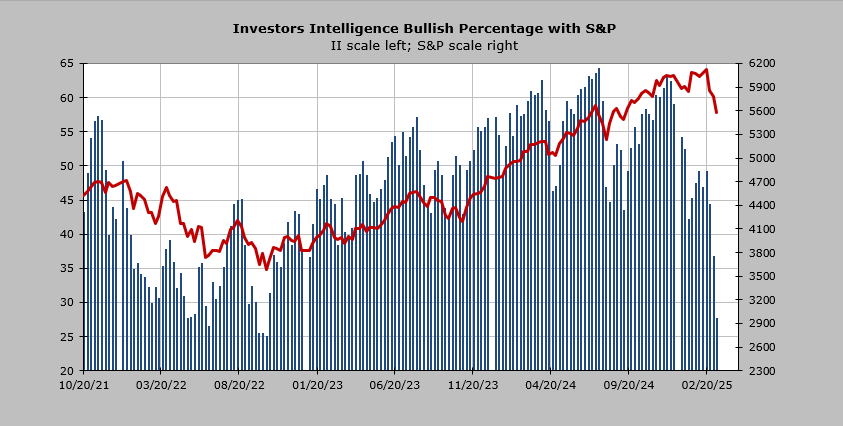

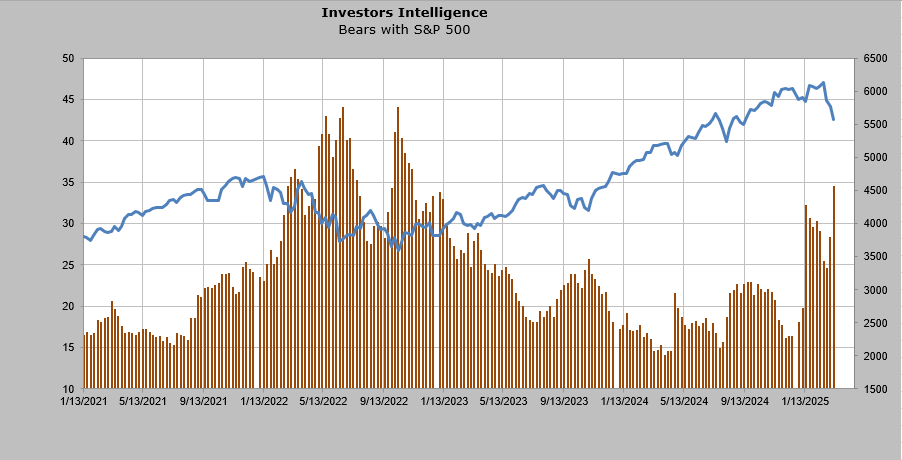

This week’s Investors’ Intelligence bulls plunged to 27.6%, and the bears lifted to 34.5%. This is the first time since the fall of 2022 we’ve seen more bears than bulls in this survey. I consider this survey the gold standard. While I often complain about AAII, this one is one to fuss over.

Notice that we had more bulls than bears in the spring of 2022, a period of time I highlighted just yesterday when we looked at volume. In fact, I recall I used this Sentiment Cycle chart that spring and thought we were in a similar spot on the chart.

In the spring of 2022, the intermediate-term indicators weren’t oversold the way they were in the fall of 2022. That is similar to now. In the spring of 2022, we did get a rally off that initial plunge as we should now. I doubt this will play out the same exact way because the market is never that convenient to give us an analogy we are so familiar with. But at least we now have a shift in sentiment that shows the same as the AAII reading that got everyone so excited three weeks ago.