Rate Cut Forecasts Show Fed Is Behind the Curve Yet Again

Don’t underestimate the chances that the Fed has underestimated inflation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As recently as the beginning of this year, the consensus was that the U.S. Federal Reserve’s Federal Open Market Committee would enact a series of interest rate reductions in 2025, extending the cycle it began in September 2024.

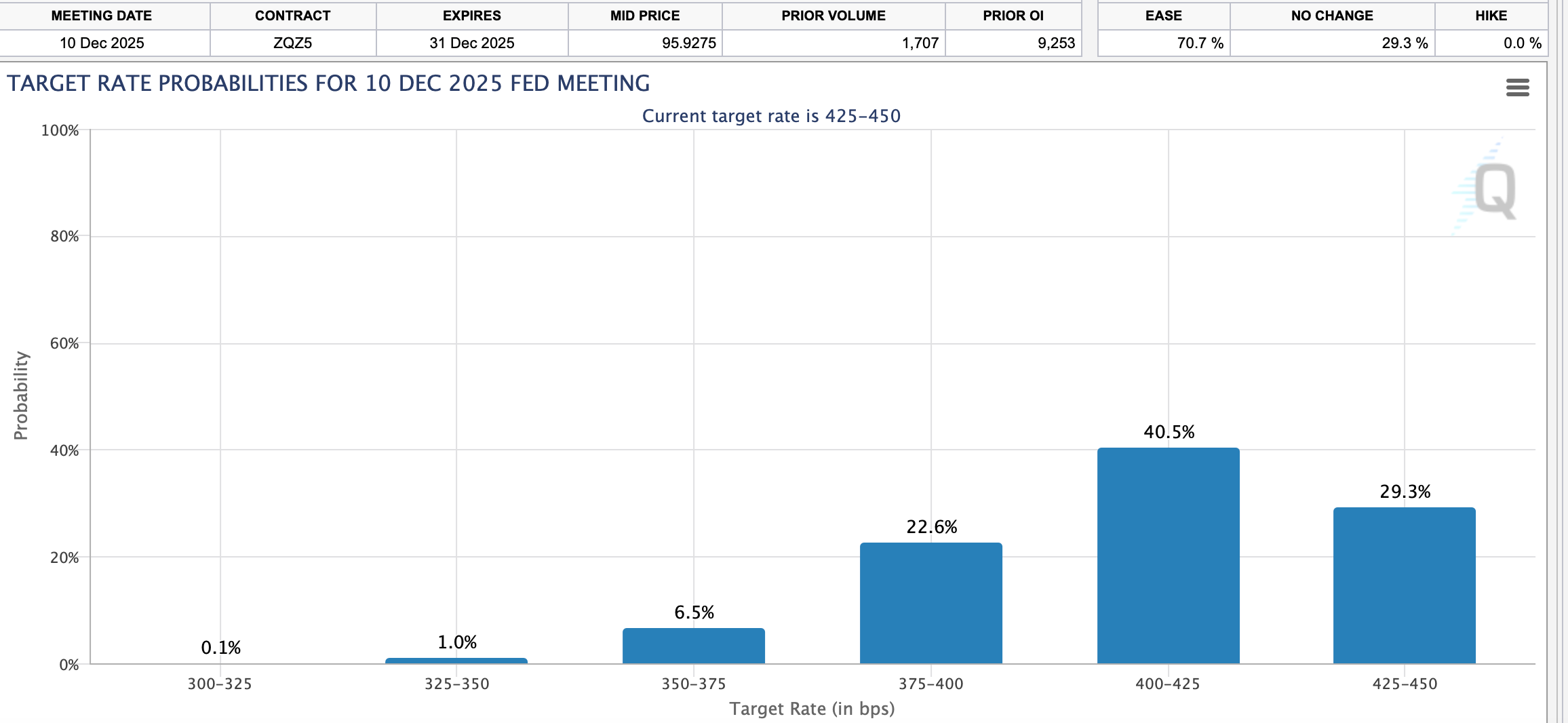

After Wednesday's hot consumer price index (CPI) report, the hope for any rate cuts at all are on life support. According to the CME’s FedWatch Tool, there is now a 29% chance that there will be no FOMC rate cuts this year, and just a 40% chance of one reduction in the Fed funds rate before the end of this year.

What is not priced in, in any form, is a rate hike. Based on the above information, the odds of a Fed rate increase in 2025 are zero. Is it possible that the Fed is once again underestimating the stickiness of consumer inflation?

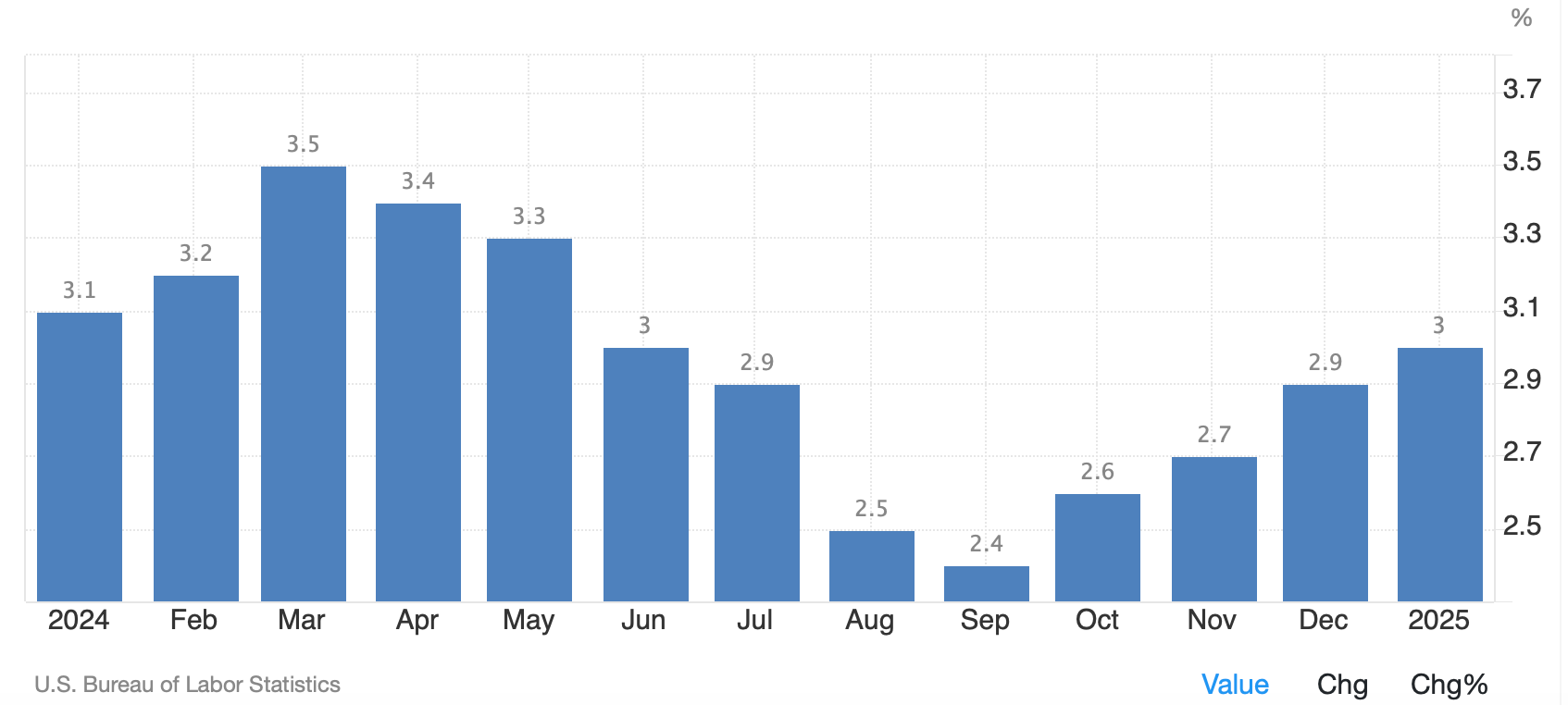

The January CPI report showed inflation surging by 3% annually at the consumer level, up from 2.9%. When measured on a monthly basis, consumer inflation jumped by 0.5% in January, well above the estimate of 0.3%.

The chart below shows the annual CPI inflation rate steadily increasing since September. Ironically, the FOMC started cutting the Fed funds rate just as inflation was about to reignite.

While the Fed missed the mark, the market nailed it. The yield on the ten-year U.S. treasury note, which jumped by 2.2% on Wednesday, began to climb just as the Fed started to cut.

The T-note’s yield bottomed on September 17 (green arrow). Ironically, the FOMC reduced the Fed funds rate by 50 basis points the very next day.

Based on the overall trend of the 10-year, it’s not difficult to imagine its yield rising to its 52-week high of 4.80%, set just last month.

Now, consider that we are just three weeks into the second Trump administration. Over the next four years, we are likely to see lower taxes and extensive deregulation. Trump’s policies are likely to spur economic growth — and with it, inflation.

Tariffs also have the potential to stoke inflation, but I’m going to withhold judgement on that topic until more information is available. Considering last week’s short-lived tariffs against Canada and Mexico, it’s impossible to know exactly how this aspect of the Trump administration’s policies will play out.

It’s possible that these potentially inflationary policies will be somewhat offset by lower government spending, which tends to be disinflationary. That depends on how much spending is to be cut, and the timing of those cuts.

In summary, additional rate cuts are being priced out of the markets, but as of yet, no rate hikes have been priced in. It’ll be interesting to see how this resilient stock market reacts when it realizes that the Fed is behind the curve once again.

At the time of publication, Ponsi had no positions in any securities mentioned.