Profits Taken, Nothing Broken

It appears the technicals survived Tuesday's slide. Also, the word of the day is 'skepticism' and guess what Jensen Huang just said about the AI race....

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Some give and some take. Financial markets were on the move again on Wednesday. After a very messy Tuesday that can be blamed on profit-taking across anything speculative in nature or extended in valuation, equities rallied broadly. Treasury debt securities, however, did not. I find that how markets work together in response to various catalysts has become a little more difficult to anticipate in this high-speed, keyword reading, AI-driven algorithmic era than it used to be.

Sentiment was a lot easier to discern when trading boiled down to a bunch of Irish, Italian and Jewish kids from the boroughs of New York City beating the heck out of each other for eighths of a dollar at a time, while wearing colored jackets and waving fingers and making sure they knew everyone else's badge numbers. What's one thing that still works correctly most of the time? Technical analysis. Know your levels. Right or wrong in one's anticipation, knowing how to read the charts, can make up a lot of ground even on days where one gets off on the wrong foot.

In Wednesday's early column, I correctly anticipated a less than certain Supreme Court when it came to the president's use of the International Emergency Powers Act in order to use tariffs as a tool of trade policy. I had expected that such skepticism would result in some turbulence in debt and currency markets. I did not expect a broad rally across U.S. equity markets. I'll take it, but I did not see it coming.

There certainly were some rough seas experienced in the bond market. The U.S. Ten Year Note paid as much as 4.16% by day's end, up seven basis points. The yield for the U.S. Two-Year Note popped five basis points to 3.64%. The U.S. Dollar Index lost ground on Wednesday after a rough six weeks of gains. Interestingly, Treasuries are rallying overnight while the greenback continues to drop. The truth is that there were a number of reasons why stocks rallied on Wednesday. The reasons, though many, were sort of. kind of, optimistic in nature, but not too optimistic. Just peachy.

Jobs!

According to the ADP Employment Report for October, labor markets are improving. A little. The report stated that the U.S. economy added 42,000 private-sector jobs for the month. This was better than the 32,000 that economists were looking for. Not only that, October was the first month since July, according to this series, that the U.S. economy actually added private sector jobs. Both August and September had printed in negative territory.

While 42,000 is not a strong number, and not even close to being a strong number, it is a positive number. A cautionary tale, though, was told by the numbers within the numbers. The Leisure & Hospitality sector, which had been the strength behind the job creation of the post-pandemic era, actually printed at -6,000 jobs for October. One must ask honestly, if hotels, restaurants and bars are shedding jobs, just what does that say about consumer health nationally?

Mixed Service Sector Performance

On Wednesday, the Institute for Supply Management released their service sector or non-manufacturing PMI for October. The headline print landed at 52.4, surfing back into expansionary territory after fence sitting (printing precisely at 50) for September. The numbers within these numbers tell a mixed story, though. While New Orders hit the tape at 56.2 and spent a fifth straight month in a state of expansion, Backlog of orders dropped all the way to an anemic 40.8 and spent an eight straight month in a state of contraction. Hmm...

Looking deeper into the data, service-related employment crossed the tape in a state of contraction for a fifth month in a row, at 48.2. Readers may recall that on Monday, the ISM Manufacturing PMI showed that manufacturing-related employment had printed in contraction for a ninth-straight month. Despite the headline number, it is difficult to be optimistic about seeing contracting employment across both the manufacturing and services sectors for multiple months consecutively as a positive.

Then there are prices. Oh boy. Prices. While on Monday, manufacturing prices hit the tape at 58, in expansion for a 13th consecutive month, prices across the service sector really took the prize. Better sit down for this one. October service sector prices crossed the tape at white hot 70, making for an incredible 101 consecutive months in expansionary territory. That's almost eight and a half years, gang. That's all of Trump 2 so far, all of Biden and almost all of Trump 1. Gee whiz.

Tough Day in Court...

For the president's team, it would seem. I don't know if I have seen the word "skeptical" ever in one day as much as I saw that word on Wednesday. Literally every media outlet described the Supreme Court justices as being skeptical that the president's global tariffs are completely lawful. Yes, even the politically conservative justices appeared "skeptical."

That said, the Court gave little indication on when a ruling might come down on the matter. It could take weeks. It could take the rest of this calendar year. The court did show some awareness that unwinding what has been done, should that be legally necessary, would be incredibly complex. Like I mentioned on Tuesday, I would not be surprised to see a compromised solution come to the fold at the time of decision.

There are certainly some aspects of the president's regime of tariffs that would fall under some kind of description of being a response to national security concerns, such as those tariffs related to fentanyl. The president does have that authority. The reciprocal tariffs exist in an area shaded gray, however, and the tariffs imposed on different nations' exports all exist in several shades of gray. I did notice that on the prediction market, Kalshi, the probability for the Supreme Court completely backing the president's schedule of tariffs dropped on Wednesday from a hair under 48% all the way to 30%.

Green on the Screen

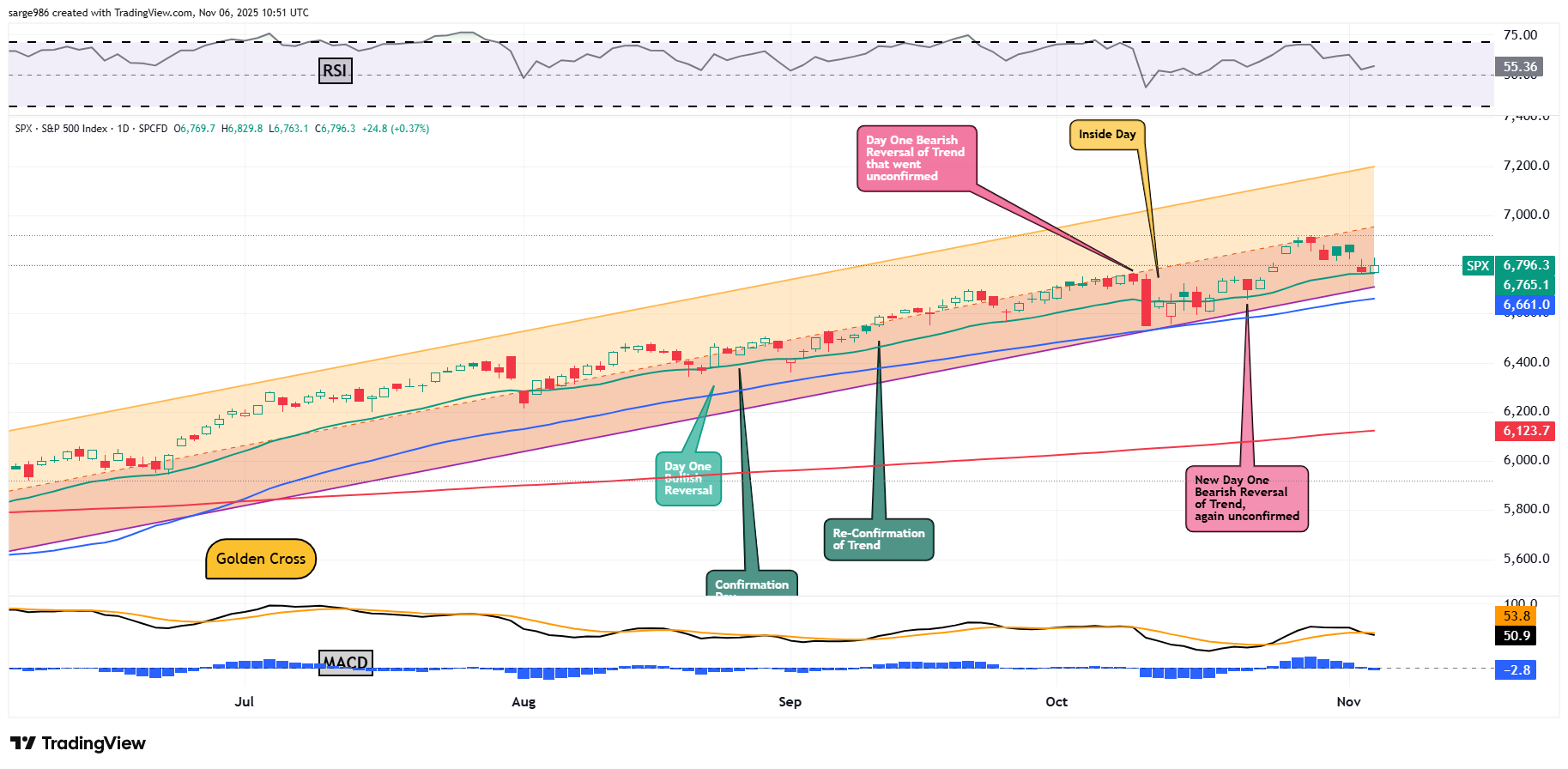

What a pleasant day after the Tuesday beat-down. Relief rally? Nah. Dead cat bounce? You know that I don't believe in those and never have. There's always a reason and that's not a reason. I really think that profit-taking was the primary reason for the pressure on Tuesday and the market has taken its pound of flesh. For now. Nothing broke, technically. In fact, take a look at this...

Just look at that consistent respect for the trend. Just look at the way the swing crowd defended the S&P 500 at the 21-day exponential moving average. Two days in a row, the market has hit the 21-day exponential moving average and stopped like it hit a brick wall, reversing higher on Wednesday. The trick now is to get that little black line (12-day EMA) in the daily Moving Average Convergence Divergence back above the little gold line (26-day line). If the market can do that, while pulling the histogram of the 9-day exponential moving average out of negative territory, and all of these conditions are close, then the trend can continue as if Tuesday was nothing more than a bad dream. Fail to turn these indicators? Well, then the nasty dream starts to become reality.

Every single major to mid-major equity index that I follow closed in the green on Wednesday, from the S&P 500 to the Nasdaq Composite to the Dow Transports to all of the small- and mid-cap indexes. The Philadelphia Semiconductor Index led the way at +3.02%, led by Micron (MU) at +8.9%, Marvell Technology (MRVL) at +6.1% and Lam Research (LRCX) at +6%.

Interestingly, it was Micron that led the losers for this group on Tuesday at -7.1%. Those Irish, Italian and Jewish kids that I mentioned earlier? They did not sell a stock down 7.1% on Tuesday only to buy it up 8.9% on Wednesday. Ever. If they did, it would have been investigated. An intra-day move of 2% for a single security back when humans were still in charge would have been major news. Hey, but execution costs are down. The heck with a fair, well developed process for centralized price discovery that actually saved investors' money.

Breadth

Nine of the 11 S&P sector SPDR ETFs closed out the Tuesday session in the green, with the Discretionaries (XLY) and the Materials (XLB) leading the way. These are the two mist tariff-impacted sectors, underscoring the Supreme Court's impact on equity markets on Wednesday. The bottom three spots on the daily performance tables were all defensive in nature, but nothing was down sharply. The Staples (XLP) finished the day in eleventh place, down just 0.07%.

Winners beat losers at the NYSE by a rough 11 to 5 and at the Nasdaq by about 9 to 5. Advancing volume took a 64.9% share of composite NYSE-listed trade and a 56.8% share of composite Nasdaq-listed trade. As for aggregate trading volume, there was a 3.5% day over-day-increase across NYSE-listings and across the membership of the S&P 500. Aggregate trade, however, dropped 2% across Nasdaq-listings and that prevents us from proclaiming that all is well in Whoville.

News

- The FAA (Federal Aviation Administration) is ordering airlines servicing U.S. routes, starting this Friday, to reduce air traffic by 10% to 40% as air-traffic controllers continue to work without pay through the government shutdown. Air-traffic controllers, quite understandably, have been calling in sick, in many cases to work in some capacity somewhere else in an effort to produce income.

- On Wednesday, Nvidia (NVDA) CEO Jensen Huang, in an interview with the Financial Times at the FT's Future of AI Summit, predicted that China will likely surpass the U.S. in the race to dominate AI. Huang credited Beijing's potential to dominate the space to that nation's more favorable regulatory environment and lower energy costs. Interestingly, this morning, Huang tried to clarify what he supposedly meant. Huang posted to his Twitter or X account, "As I have long said, China is nanoseconds behind America in AI. It's vital that America wins by racing ahead and winning developers worldwide."

- The Fed will be out in force on Thursday. See below.

Economics

(All Times Eastern)

10:30 - Natural Gas Inventories (Weekly): Last +74B cf.

The Fed

(All Times Eastern)

11:00 - Speaker: New York Fed Pres. John Williams.

12:00 p.m. - Speaker: Cleveland Fed Pres. Beth Hammack.

3:00 - Speaker: Reserve Board Gov. Christopher Waller.

3:30 - Speaker: Philadelphia Fed Pres. Anna Paulson.

5:30 - Speaker: St. Louis Fed Pres. Alberto Musalem.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (BDX) (3.91), (COP) (1.41), (DDOG) (.46), (DD) (1.11), (MRNA) (-2.14), (RL) (3.45)

After the Close: (ABNB) (2.31), (XYZ) (.64), (DKNG) (-.38), (IREN) (.14), (MP) (-.16), (PTON) (.01), (TTWO) (.93), (TTD) (.44)

At the time of publication, Guilfoyle was long PTON, MU, NVDA equity.