Powell Sets Off Rally With 'Close to Perfect' Change of Tone

The Federal Reserve chair changed his dovish tune in comments from Jackson Hole and the market is responding.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The Captive Dove

"Poor restless dove, I pity thee;

And when I hear thy plaintive moan,

I mourn for thy captivity,

And in thy woes forget mine own.

To see thee stand prepared to fly,

And flap those useless wings of thine,

And gaze into the distant sky,

Would melt a harder heart than mine."

-Anne Bronte (1846)

Powell Speaks

He spoke just a few minutes later than his slotted 10 a.m. ET start time. He did what he had to do. He spoke at length on labor market health. He spoke at length on the rate of inflation and inflation expectations. Most importantly, Jerome Powell, whether he felt pressured or not, opened the cage of Anne Bronte's "Captive Dove" and let that bird fly.

The statement heard around the world was this:

Powell did make an effort to sound balanced. After all, he acknowledged that there is now upside risk to inflation and currently downside risk to employment. On those notes, Powell said that the inflationary impacts of tariffs "are now clearly visible." However, and he had not done this before, Powell also acknowledged that he now has greater confidence that the inflationary effects on tariff-impacted goods prices will be relatively short in nature.

No, I did not hear the word "transitory" and Powell did back away from calling this price increase a "one-time thing" as it may take time for those increases to completely work their way through the economy. He did caution that, should inflation lead to wage growth, then that could force a lengthier process. Powell did add that the FOMC would likely be quick to move on tempering inflation expectations for both businesses and consumers should they start to really move notably higher.

All that said, in the end, Powell admitted that a still resilient but softening of U.S. labor market had put the Fed in a "challenging position." Powell, as always, it seems, stated that the Fed would have to, "Proceed carefully as we consider changes to our policy stance."

Fed Funds Futures

Coming out of the event, federal funds futures trading in Chicago are now pricing in an 89% probability for a 25 basis point rate cut on September 17. That's up from 71% earlier on Friday morning.

According to these markets, there is now a 46% likelihood for a second 25 basis point rate cut on October 29. That's up from 35% ahead of the speech. The prospects for a second 25 basis point rate cut by December 10 have moved up to 87% from 72%, while this market is now pricing in a 40% chance for 75 basis points worth of rate cuts in 2025, up from 26% earlier.

Markets

Since Friday morning, the yield paid by the U.S. 10-year note has moved from 4.34% down to 4.26%, its lowest level of the week. The two-year note now yields 3.69% down from 3.81% on Friday morning. Looking at the shallow end of the pool, U.S. 90-day paper now pays 4.19%, down from 4.24%.

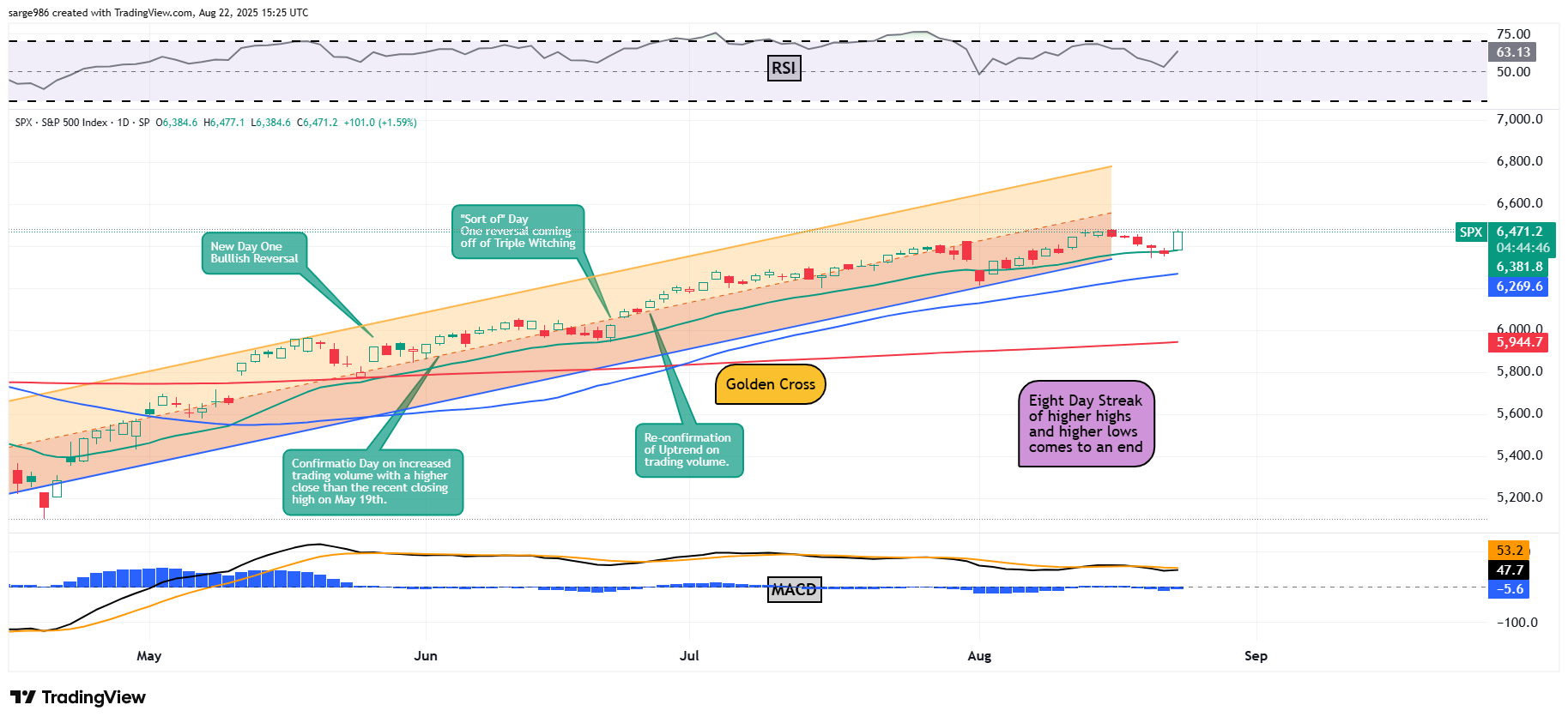

As for equities, the rally is on. The Nasdaq Composite is now up more than 2% as the S&P 500 has gained 1.6%. Ten of the 11 S&P SPDR ETFs are in the green, led by the Discretionaries XLY and the Materials XLB as the U.S. Dollar Index has weakened.

Are consumers going to be alright? The three leading industries within the Discretionaries late Friday morning are Recreational Products, Furnishings and Automobiles.

Technology XLK is strong as both the semiconductors and software stocks are rallying. Mortgage companies and Asset Managers are flying. The Banks are acting well too. What's not so hot? The Defensive sectors. Health Care XLV, the Utilities XLU, which are considered bond proxies, and the Staples XLP are all at the bottom of the performance tables.

My Thoughts

I think Powell was as close to perfect as he gets today. As I have said, after arrogantly calling for a 100 basis point cut earlier this month, after the hot July PPI print, I reeled that in as much as I could. I still think that the spread between the yields paid by U.S. three-month T-bill and the U.S. 10-year note is too narrow and that the fed funds rate is too high.

That said, a series of 25 basis point rate cuts starting in September, taking a month off here or there when appropriate depending on the data, is probably fine by me. Of course, if either side of the Fed's dual mandates of price stability or full employment requires rapid attention, then the Fed had best be able to respond like lightning. Any dilly-dallying under those circumstances and I'll go right back into jerk mode.

The S&P 500 is now trading at its highs for the week after five straight down days. Good thing we bought those dips in our favorite names, huh, gang?

Palantir PLTR, SoFi SOFI and Rocket Lab RKLB are all way, way off of their mid-week lows.

At the time of publication, Guifoyle was long PLTR, SOFI and RKLB equity.