Powell Holds Steady, While Vance Talks Chips

What counts as American-made chips and how could that hit or help Taiwan Semi, Foxconn, Intel, Nvidia and more?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We came into Tuesday morning looking for a selloff, hoping it would be mild to moderate in nature, and that was exactly what we got. Fed Chair Jerome Powell testified on monetary policy before the Senate Banking Committee, and sat for a few hours, fielding questions from largely (economically) under-qualified individuals. He'll go through the same dog-and-pony show before the House Financial Services Committee this morning where the questions tend to be even more amateurish, if that's even possible.

Powell made himself clear on Tuesday. Barring some kind of economic shock, monetary policy and short-term interest rates will be sitting where they are now for some time. (But don't forget, the January consumer price index report will cross the tape this morning, followed by January retail sales and January industrial production on Friday.) More than halfway into his opening address, Powell stated:

"With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance. We know that reducing policy restraint too fast or too much could hinder progress on inflation. At the same time, reducing policy restraint too slowly or too little could unduly weaken economic activity and employment. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the FOMC will assess incoming data, the evolving outlook, and the balance of risks."

Then Powell wrapped up his song and dance:

"Let me conclude by emphasizing that at the Fed, we will do everything we can to achieve the two goals Congress set for monetary policy—maximum employment and stable prices. We remain committed to supporting maximum employment, bringing inflation sustainably to our 2 percent goal, and keeping longer-term inflation expectations well anchored."

My Take

What's clear is that Powell considers existing threats to the economy, consumer-level inflation and potential weakness in labor markets to be roughly in balance with one another. While that might be seen in a positive light, the negative takeaway is that the central bank will wait until something breaks before taking action.

Either the central bank will raise interest rates in response to an unwelcome surge in inflation or will cut interest rates in response to an unwelcome surge in the unemployment and underemployment rates. Essentially, there is no way to win, as our central bankers will not be proactive ahead of hitting either one wall or the other.

Some on Wall Street (not most) had hoped for a clue on whether a rate cut was in the cards for the first half of 2025. It did not sound like it and that is why Treasury yields worked their way higher (The U.S. Ten Year Note paid 4.54% by day's end) and some stocks struggled as the tape meandered laterally through the session after opening on weakness.

Interesting Development on Chips

Vice President JD Vance spoke from the Artificial Intelligence Action Summit in Paris on Tuesday. Vance said bluntly: "To safeguard America's advantage, the Trump administration will ensure that the most powerful AI systems are built in the U.S. with American-designed and manufactured chips."

What's interesting is that the planet's dominant semiconductor chip foundry business is Taiwan Semiconductor TSM, and that Taiwan Semi has built and is building new facilities with some Chips Act funds in Arizona in anticipation of such a U.S.-centric development. Don't forget that the Biden administration was working toward a similar conclusion on high end chips and had implemented a ban on sales of those AI-capable chips to Chinese customers.

Does a plant owned by a Taiwanese company in Arizona count as American manufactured? I'm not sure. TSM was up small (+0.38%) on Tuesday, while the shares of the only U.S.-headquartered foundries, Intel INTC and GlobalFoundries GFS both soared. INTC was up 6.07% while GFS was up 6.25%. INTC is up another 1.8% or so overnight. Does this matter to me? Yes. As readers well know, I am long some INTC, taking advantage of weakness going into and out of the firm's separation from CEO Pat Gelsinger in early December.

Intel does not have a major AI-capable chip of its own right now, but the company has been contracted by Amazon AMZN to manufacture that company's own Tranium chips that power the AWS cloud. Could a company like Intel, which has lagged badly in recent years, without a CEO and without an AI offering of its own, steal market share in the foundry business from Taiwan Semi when it comes to high-end AI chip designers such as Nvidia NVDA and Advanced Micro Devices AMD?

I'd like to think so. The fact, though, remains that Nvidia CEO Jensen Huang and AMD CEO Lisa Su are both Taiwanese immigrants to the U.S. How strong are their ties to, and their relationship with Taiwan Semiconductor? I guess we're about to find out.

On That Note

News broke overnight that Chairman Young Liu of Taiwan-based Foxconn Technology, a major supplier to U.S. consumer electronics giant Apple AAPL said that the company can plan to work around the new U.S. tariffs enacted by the Trump administration. Liu told reporters that Foxconn has the ability to manufacture its products in the U.S., and "depending on the tariffs, we will plan different production capacities accordingly."

Liu added, "For the company, if we don't manufacture here, we can do it there, so the impact is not too great." Things that make you go hmmm...

Marketplace

On Tuesday, the S&P 500 closed up 0.03%. We used to call that "unchanged" back in the days of yore when the trading was done in Spanish pieces of eight by very handsome and very smart humans wearing colored jackets. Algorithms trading in decimals don't really do "unchanged." The Nasdaq Composite surrendered 0.36% for the session, as the small to midicap indexes also closed in the red.

Nine of the 11 S&P sector SPDR exchange-traded funds managed to close in the green though, led by the Staples XLP, a defensive sector, while the Discretionaries XLC, which are cyclical in nature... led to the downside. That may or may not be interesting.

Winners beat losers by just a smidgen at the NYSE as losers beat winners by a 3-to-2 margin at the Nasdaq MarketSite. Advancing volume took a 46.9% share of composite NYSE-listed trade and a 48.4% share of composite Nasdaq-listed activity. Trading volume contracted on a day over day basis across the listings of both the NYSE and Nasdaq and across the membership of the S&P 500. The implication there? Traders, halfway through the twin Powell testimonies are waiting on this morning's CPI report.

Anyone Else Notice That...

On Tuesday, Rich Ross, who is head of technical analysis at Evercore ISI, said that breakouts for the S&P 500 and Nasdaq 100 to all-time highs are "imminent." Ross added that he felt that Nvidia had bottomed and that the US Dollar Index and yield for the US Ten Year Note were peaking. Ross sees NVDA, which closed at $132.80 on Tuesday, and is down 1.4% year to date, reaching $200 per share.

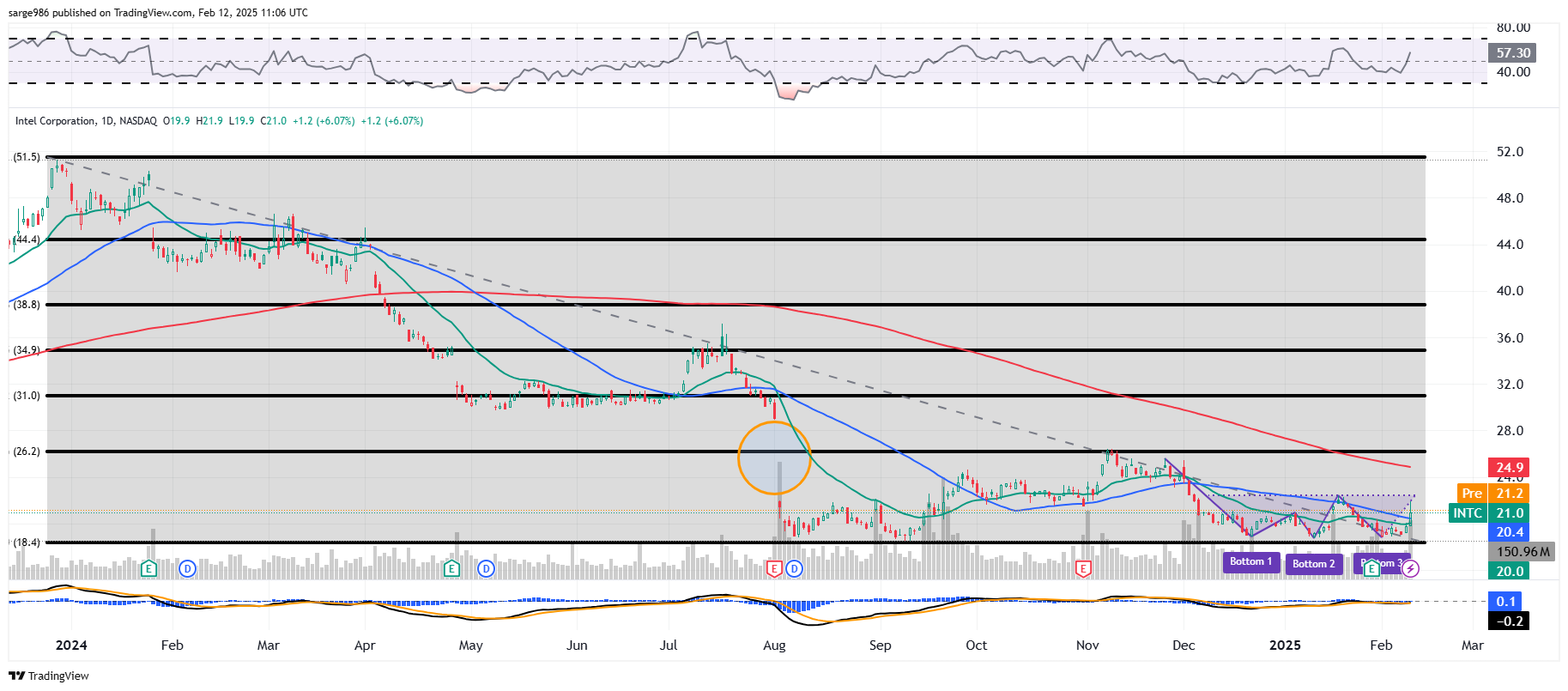

On Chips

Note that INTC in early November had hit resistance at a precise 23.6% Fibonacci retracement of the late 2023 through September selloff.

The stock then sent on to develop a triple-bottom pattern (potentially signaling a bullish reversal) with a $22.50 pivot. Relative Strength and the daily Moving Average Convergent Divergence indicator are both showing signs of improvement, and if the stock can get through that November resistance, the unfilled gap from this past summer would require a tick at $28.90, or better, to fill. That would be a 38% move from last night's closing auction price.

Meanwhile, NVDA is sending mixed messages. The stock has put in a double-top pattern of bearish reversal, which appeared to work well, but has since reclaimed its 200-day simple moving average only to hit resistance at its 50-day simple moving average. Taking that blue line would bring on more long-side exposure by professional managers. Meanwhile, with a neutral looking Relative Strength Index, or RSI, reading, the still bearishly postured daily MACD is suddenly looking a little better as that 12-day exponential moving average has poked its ugly head above the 26-day exponential moving average with the histogram of the 9-day EMA now in positive territory.

Good Luck Today, Traders

.... May the force be with you. Rock on.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.97%.

07:00 - MBA Mortgage Applications (Weekly): Last 2.2% w/w.

08:30 - CPI (Jan): Expecting 0.3% m/m, Last 0.4% m/m.

08:30 - Core CPI (Jan): Expecting 0.3% m/m, Last 0.2% m/m.

08:30 - CPI (Jan): Expecting 3.0% y/y, Last 2.9% y/y.

08:30 - Core CPI (Jan): Expecting 3.1% y/y, Last 3.2% y/y.

10:30 - Oil Inventories (Weekly): Last +8.664M.

10:30 - Gasoline Stocks (Weekly): Last +2.233M.

1:00 p.m. - Ten Year Note Auction: $42B.

2:00 - Federal Budget Statement (Jan): Last $-87B.

The Fed (All Times Eastern)

10:00 - Speaker: Federal Reserve Chair Jerome Powell.

12:00 noon - Speaker: Atlanta Fed Pres. Raphael Bostic.

5:05 - Speaker: Reserve Board Gov. Christopher Waller.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CME (2.45), CVS (.94), MLM (4.56)

After the Close: ALB (-.66), APP (1.79), CSCO (.91), HOOD (.52), TTD (.57)

At the time of publication, Guilfoyle was long INTC, AMZN, NVDA equity.