Peace Talk Trouble, Trump 'No More Mr. Nice Guy,' Earnings Bonanza

Let's see where we stand with the talks with Iran after fighting in Hormuz, chart the 'mini-golden cross' on the S&P, and check on the earnings for the week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Last week was wonderful for U.S.-based investors. It's been more than that. It's really been three weeks, or April to date, that's been wonderful. Record highs for the major equity indexes had bundled with pressure on Treasury yields and much lower prices for crude oil to create a perfect recipe for higher risk asset prices. On Friday, the euphoria came to a head. This was in response to a declaration made by the Ports and Maritime Organization of the Islamic Republic of Iran. That agency stated that the Strait of Hormuz would be "completely open" to commercial vessels at least for the remainder of the 10-day ceasefire agreed to on Thursday between Israel and Lebanon.

That joy lasted but a day. A U.S. delegation is still expected to arrive in Pakistan this week and peace talks between the U.S. and Iran are still expected to continue. That said, the weekend just completed was a rough one for the peace process. Some Iranian authorities disputed claims made last week by Pres. Donald Trump covering what had been agreed to so far. The Wall Street Journal among other outlets, is reporting that the Iranian military fired upon two commercial ships after abruptly reversing course concerning the re-opening of that maritime passage.

After that, the Iranian-flagged cargo ship Touska tried to run the U.S. naval blockade in the Gulf of Oman. That ship was intercepted by the guided missile destroyer USS Spruce. The Spruce fired several rounds of simple 5-inch naval artillery (the cheap stuff) at the engine room of the Iranian ship, disabling that vessel. The ship was then seized by a team of U.S. Marines who, according to the president, "have custody of the vessel."

In response, front-month WTI Crude futures are trading with an $89 handle overnight into Monday morning. While this is up sharply from a low in the $82-area on Friday, that is still far lower than the $113 or so paid by some traders less than two weeks ago. U.S. equity index futures are trading sharply lower as well but appear to be off of the overnight lows and this comes after a long winning streak that had lasted for all of April and had taken U.S. stocks to those already mentioned record highs.

Where We Stand

On Sunday, Pres. Trump said that there would still be peace talks between the U.S. and Iran on Monday (today). Iran is supposedly making public that side's intent not to attend after this weekend's events. The U.S. president has again threatened to “Knock out every single Power Plant, and every single Bridge, in Iran.” The president posted to social media, “NO MORE MR. NICE GUY! They’ll come down fast, they'll come down easy and, if they don’t take the DEAL, it will be my Honor to do what has to be done, which should have been done to Iran, by other Presidents, for the last 47 years.”

Mean Street

And we don't worry 'bout tomorrow 'cause we're sick of these four walls

Now what you think is nothin' might be somethin' after all

Now you know this ain't no through street, the end is dead ahead

The poor folks play for keeps down here, they're the living dead

Come on down, huh, down to Mean Street.

- E. Van Halen, A. Van Halen, Anthony, Roth (Van Halen), 1981

The Past Week

What at the time were improving prospects for peace in the Middle East dominated the past week for U.S. traders and investors. That was not all though. There was plenty of good news. First quarter earnings season is off to a good start. On top of that, some of the recent macroeconomic releases have hit the tape at much better levels than expected. Last week, March producer price index, which measures inflation at the producer / wholesale level, was much cooler than had been projected, surprising economists. In addition, U.S. export prices (thanks to oil) for March were much hotter than import prices. Finally, regional manufacturing surveys conducted by both the New York and Philadelphia Feds showed much stronger conditions and expectations in April than had been the consensus view.

Related: If You Want to Be a Good Investor, Listen to the Indicators and Not Your Emotions

Week Ahead

What matters moving forward...

- The Situation in Iran: As has been the case, nothing matters more right now than the peace process, the ability to reopen the Strait of Hormuz to commerce and the market price of crude oil.

- Macro: For a second straight week, this will not be an exceptionally heavy week for the U.S. domestic macroeconomic data-point release schedule. March retail sales will cross the tape on Tuesday morning. That does matter and will be the headline macroeconomic event of the week. Just a heads up, there is a lot of optimism circulating among professional economists concerning this particular report. Then, S&P Global will release their Flash PMIs for both the US manufacturing and service sectors for the month of April on Thursday morning. Finally, on Friday morning, the University of Michigan will revise its initial April survey release covering consumer sentiment and inflation expectations.

- The Federal Reserve: This will be a very happy week for most of us. The Federal Reserve has gone into its "media blackout" period ahead of the U.S. central bank's scheduled April 29 policy decision. What does that mean to you and I? It literally means that the clown car has stopped. All of the career academics short on actual life experience (PhD economists) posing as officials at the Federal Reserve bank will have to keep their traps shut until their policy statement is released a week from this Wednesday. Rah.

- Earnings: First-quarter earnings season is now well under way. A number of key names are set to release their financial results for the early part of 2026 this week. On Tuesday morning, 3M (MMM) will lead-off along with GE Aerospace (GE) , Halliburton (HAL) , Northrop Grumman (NOC) , RTX Corp (RTX) \ and UnitedHealth Group (UNH) . Wednesday will bring numbers from AT&T (T) , Boeing (BA) , GE Vernova (GEV) , IBM (IBM) , Lam Research (LRCX) , and Tesla (TSLA) . Over Thursday and Friday, we'll hear from Honeywell (HON) , Lockheed Martin (LMT) , Intel (INTC) , Procter & Gamble (PG) and SLB (SLB) .

- Other Events: Investors will have to keep at least one eye and one ear focused upon two corporate events this week. Alphabet's (GOOGL) Google Cloud Next 2026 conference will be held this Wednesday through Friday in Las Vegas, Nevada. Also in Las Vegas, perhaps to less fanfare, Adobe (ADBE) is holding its Adobe Summit 2026 conference as we write and read this note. That conference began last night and runs through Wednesday.

The Week That Was

U.S. financial markets posted a third consecutive winning week going into what was a tough weekend for the peace process:

- The S&P 500 gained 1.2% on Friday and 4.54% for the week.

- The Nasdaq Composite added 1.52% on Friday, and 6.84% for the week.

- The Nasdaq 100 tacked on 1.29% on Friday and 6.2% for the week.

- The Russell 2000 ran 2.11% on Friday AND 5.56% for the week.

- The S&P Small Cap 600 gained 2.06% on Friday and 4.04% for the week.

- The S&P Midcap 400 added 1.97% on Friday and 3.51% for the week.

- The Dow Transports surged 2.79% on Friday and soared 10.24% for the week.

- The Philly Semis popped for 2.43% on Friday and for an impressive 7.49% for the week.

- The KBW Bank Index gained 1.41% on Friday and 2.38% for the week.

On Friday, nine of the 11 S&P sector SPDR exchange-traded funds closed out the session in the green. The winners were led higher by the discretionaries (XLY) and the industrials (XLI) . Energy (XLE) led the losers. Breadth was impressive for the day as was trading volume.

For the week, eight of the 11 S&P sector SPDR ETFs closed out the session in the green. The winners were led higher by technology (XLK) , the discretionaries and communication services (XLC) as energy led the losers. Growth stocks were clearly where the positive action was for the period.

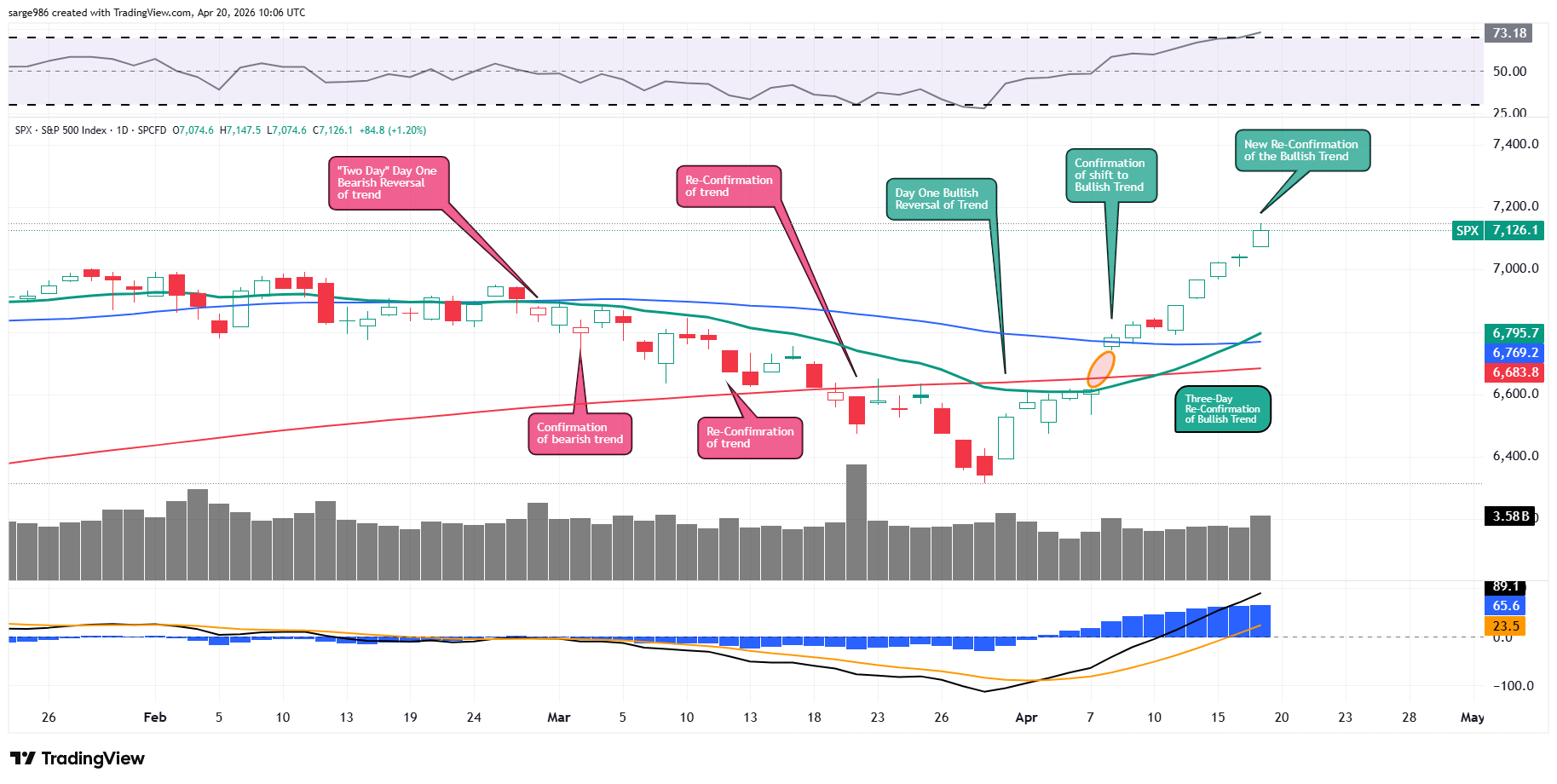

The Chart

Incredibly, the S&P 500 reconfirmed the bullish trend yet again on Friday. The S&P 500 has now posted 12 winning sessions in 13 as the Nasdaq Composite has put together a 13-day winning streak. Both of those indexes closed out the week at all-time highs. The S&P 500 enjoyed that "mini-golden" cross last week. Let's see if it can hold through this morning's selloff.

The indicators are all rocking. Relative Strength is now in a technically overbought state so this pause in the bullishness could actually be healthy and give investors a chance to buy stocks they missed at lower prices. The daily moving average convergence divergence has now moved into an overtly bullish posture with all three components now set up for higher asset prices.

Earnings

As of April 17, according to FactSet, for the first quarter, Wall Street now expects to see a year-over-year blended (results & expectations) earnings growth for the S&P 500 of 13.2%, up from 12.6% last week, and up from 11.6% more than a month ago. Wall Street also sees revenue growth of 9.9%, up from 9.8% a week ago. With 10% of the S&P 500 having reported, 88% of companies have beaten earnings expectations, while 84% have beaten sales projections.

For the full year of 2026, Wall Street now looks for earnings growth of 18%, up from 17.6% last week, and up from 14.7% more than a month back, on revenue growth of 9.2%, up from 9% last week and up from 7.7% more than a month ago. The outlook for the second quarter also continues to improve quite dramatically. Psst... corporate America is kicking some tail in 2026. Stay invested, buckaroos.

At the moment, the Technology sector is projected to have grown earnings a stunning 45.1% for the first quarter with the Materials in second place at growth of 21.6%. Three sectors, health care, communication services and energy are projected to have suffered a Q1 earnings contraction.

The Flower

Once in a golden hour

I cast to earth a seed.

Up there came a flower,

The people said, a weed.

To and fro they went

Thro' my garden bower,

And muttering discontent

Cursed me and my flower.

Sow'd it far and wide

By every town and tower,

Till all the people cried,

'Splendid is the flower! '

- Alfred lord Tennyson, 1864

'Don't give up on peace' ... your pal

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 20.9-times 12 months' forward-looking earnings, up from 20.4 times last week, but still down from 21.6 times more than a month prior. This is above the five-year average of 19.9 times for the index as well as being well above its ten-year average of 18.9 times.

The S&P 500 also ended last week trading at 27.8-times trailing 12 months' earnings, up from 27.2-times one week ago, and even with the 27.8 times that the index reached more than a month ago. This also stands well above the five-year (24.7 times) and ten-year (23.2 times) averages for the index.

Seven of the 11 sectors are now trading above their five-year average valuations, led by the discretionaries (28.2 times), the industrials (25.8 times) and technology (23.2 times). Only tech and the REITs closed out last week undervalued relative to their five-year norms.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in a 100% probability for no change to be made to the target range for the Fed Funds Rate at the next federal open market committee policy meeting on April 29. Unlike last week, there are no rate hikes priced in at any point in the future looking out over almost two years' time.

That said, there are still no rate cuts priced in for calendar year 2026. In fact, no cuts are priced into these markets until July of 2027. Understand though, that we can expect that everything will change several times over, as the year progresses, especially as the midterm elections approach.

Economics

(All Times Eastern)

No significant domestic macroeconomic data-points scheduled for release.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (CLF) (-.42)

After the Close: (ALK) (-1.59)

At the time of publication, Guilfoyle had no position in any security mentioned.