Peace Sells (Except for Palantir)

Military contractors were down on the Ukraine news, while PLTR was up; now it's rebuilding time; also, ouch! That CPI could fry an ... egg.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The news that so many people had waited so long to hear made headlines just before lunchtime on the east coast of the U.S. on Wednesday. Equity markets, which opened on weakness in the wake of a red-hot January consumer price index print, moved higher, and hit their apex for the regular session about an hour later. Then, as if reality hit, that weakness seeped back into trader sentiment. Though traders and investors had bought into that early weakness, they also sold this rather moderate mid-day strength.

U.S. President Donald Trump agreed in a phone call with Russian President Vladimir Putin to begin negotiations to bring an end to Russia's three-year war in Ukraine. The U.S. president referred to the phone call as "lengthy and highly productive." President Trump spoke with Ukrainian President Volodymyr Zelenskiy after speaking to the Russian president. Apparently, Zelenskiy has told U.S. officials to begin talks on ending this war.

Elsewhere, U.S. Secretary of Defense Pete Hegseth, speaking in Brussels, told Ukraine's NATO allies that a return to pre-2014 borders for Ukraine (involving the Crimean Peninsula) was unrealistic and that the U.S. would not contribute boots on Ukrainian ground to secure peace. Hegseth also stated that NATO membership for Ukraine was unlikely, and that Ukraine would probably have to trade some occupied territories with Russia.

Needless to say, all of the major U.S. defense contractors with the obvious exception of Palantir Technologies PLTR traded lower on the day. The big data / AI / analytics king was up 4.24% on the day, while all of the purveyors of military hardware traded into the red on Wednesday.

It's Rebuilding Time...

So, start thinking not of who manufactures and sells missiles, anti-tank weapons, radars, drones and fighter aircraft, but of who is going to pay for the rebuilding of Ukrainian cities and farms. What companies are going to receive large contracts? Don't worry about national security. Demand for that kind of hardware will be there, especially for the NATO countries who still have Russian forces on their doorstep.

That said, the Ukrainian rebuild will place a fiscal burden on the EU and perhaps the U.S. economies, while demand will increase greatly for tractors, construction equipment, concrete, steel and the like. U.S., Chinese, and European companies will be vying for that business. Among U.S. firms, think Caterpillar CAT, think Deere DE, think United Rentals URI. URI only has 38 locations in Europe (of more than 1,600 globally). That will have to change.

Hot, Hot, Hot

It's kind of difficult to understand how so many economists were caught off guard by January's hot consumer price index print. They live in this economy, don't they? I had told all who would listen that the Hedgeye model, which is something I find great value in paying for, that consumer prices were likely up 3% or more from where they were a year ago. That call by Hedgeye was practically spot on.

For the January, headline CPI printed at month-over-month growth of 0.5%, up from 0.4% growth in December and well above Wall Street's expectations for 0.3% growth. On a year-over-year basis, headline consumer prices for January were up a precise 3%, which was an acceleration over the 2.89% December pace and above the consensus view for growth of 2.9%.

At the core, January CPI printed at growth of 0.4% m/m and 3.3% y/y, up from December's 0.2% and 3.2% respectively and above the 0.3% and 3.1% that most economists had projected (hoped for). The heat came from gasoline, fuel oil, piped gas, used vehicles, medical care commodities, transportation services and of course eggs. Eggs were up 15% month over month after the culling of millions of chickens due to the threat from the avian flu.

A break in rising prices? It's coming. According to both Hedgeye and the Cleveland Fed, consumer prices are already expected to have experienced a slowdown in the pace of inflation for January. That does not mean prices will contract. It means that prices will rise more slowly. As for March, the jury is still out, but it looks like inflation will accelerate again into the fourth quarter of 2025 after February. We'll see.

This makes February sort of dangerous. Though slowing inflation is a positive for struggling consumers, Q4 gross domestic product printed at annualized q/q growth of 2.3% in late January coming off of 3.1% Q3 growth. There is almost no environment more dangerous for risk asset valuations than one where the pace of both inflation and economic activity slow down. Consensus currently calls for first-quarter GDP growth of roughly 2.1%, which would be a continuance of this deceleration in activity. That said, Hedgeye's model, which I trust, does not show this deceleration occurring until Q2.

Financial Markets

Treasury yields soared in response to the consumer price index print alongside the U.S. Dollar Index. This is largely because rising inflation makes it nearly impossible for the Fed to reduce short-term interest rates. The U.S. Dollar Index rapidly sold off after that spike, but the yield for the U.S. Ten Year Note ran up to 4.64% for the day as Fed Funds futures trading in Chicago moved the timing for any next quarter-percentage point reduction to the target range for the central bank's benchmark interest rate out to September from July.

For the Wednesday session, the S&P 500 gave up 0.27%, while the Nasdaq Composite squeezed out a gain of 0.03% (essentially unchanged). Smaller caps struggled more so did the large caps as smaller caps rely more heavily on borrowed capital. The Russell 2000 surrendered 0.87% as the S&P Midcap 400 gave up 0.7% and the S&P Smallcap 600 gave up 1.3%.

Among the 11 S&P sector SPDR exchange-traded funds, only Communication Services managed to close in the green at +0.11%, while 10 of these funds closed lower. Energy XLE was pounded for a loss of 2.41%, while sectors more defensive in nature appeared to outperform more cyclical sectors.

As far as breadth is concerned, losers beat winners by more than 2 to 1 at the NYSE and by more than 4 to 3 at the Nasdaq. But the breakdown in trading volume was not all that awful. Hence, U.S. equity markets again avoided the marking of a "day one" downward reversal of trend. Advancing volume took a 45.6% share of composite NYSE-listed activity, but a surprising 62.4% share of composite Nasdaq-listed trade.

While aggregate trading volume expanded across both those names listed at the NYSE and across the membership of the S&P 500, volume contracted across names domiciled at the Nasdaq MarketSite.

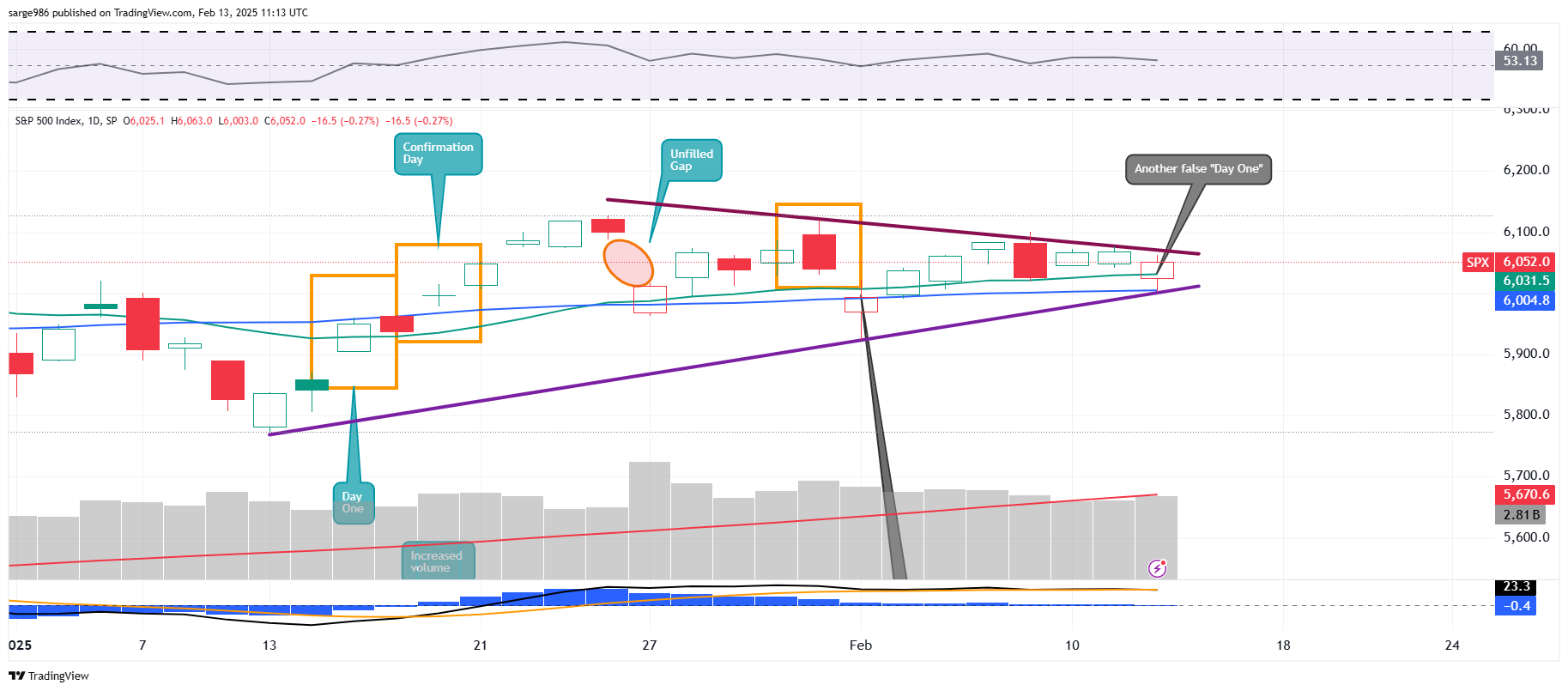

Chart

The closing pennant formation continues on its collision course. Once closed, the likelihood of a violent move one way or the other increases.

Relative strength remains neutral. The daily Moving Average Convergence Divergence is almost indiscernible at this point. What was impressive on Wednesday was the support shown for the S&P 500 at its own 50-day simple moving average. That suggests that more than just retail investors bought the CPI-inspired dip. Now, on to the produce price index.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 215K, Last 219K.

08:30 - Continuing Claims (Weekly): Last 1.886M.

08:30 - PPI (Jan): Expecting 0.2% m/m, Last 0.2% m/m.

08:30 - Core PPI (Jan): Expecting 0.3% m/m, Last 0.0% m/m.

08:30 - PPI (Jan): Expecting 3.4% y/y, Last 3.3% y/y.

08:30 - Core PPI (Jan): Expecting 3.5% y/y, Last 3.5% y/y.

10:30 - Natural Gas Inventories (Weekly): Last -174B cf.

1:00 p.m. - Thirty Year Auction: $25B.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CROX (2.26), DDOG (.43), DE (3.26), ZTS (1.35)

After the Close: ABNB (.58), PANW (.78), ROKU (-.43), TWLO (1.03)

At the time of publication, Guilfoyle was long PLTR equity.