Overwhelming Force, Bessent's 'Bombs,' Something to Build On? Tesla and Musk

Equities brought overwhelming force to the marketplace on Tuesday. Let's examine what transpired and whether we have 'a ballgame' now. Plus, the IMF, WEF, Intel and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Children played outside on Tuesday. Lovers walked hand in hand along sandy beaches. Oh, what joy.

The sun came out, flowers bloomed, and birds sang their songs. Did I mention that the New York Mets have already put together their second six-game winning streak of the season... with more than a week left in April? Rock on.

Twenty-four hours ago. Remember? Just twenty-four hours ago, we decided that what we had witnessed on Monday afternoon came pretty close to a full-on panic. We did mention that panics are more difficult to identify now that trading is close to fully electronic and decisions are made via algorithm, instead of by Irish, Italian and Jewish kids from the neighborhood. Be that as it may, at least for now, that panic may have been an attempt at a market bottom.

Those same keyword-reading algorithms react to supportive headlines just as aggressively as they do to less than supportive headlines. That said, plenty of positive headlines ran across the tape on Tuesday and the good news or rumors of good news kept on rolling overnight.

Most financial media outlets credited the Tuesday morning rally to what happened at a closed-door meeting hosted in Washington, D.C. by JPMorgan Chase JPM. It was at that meeting that Treasury Secretary Scott Bessent spoke on trade conditions between the U.S. and China. He told the room, "No one thinks the current status quo is sustainable" and "We have an embargo now, on both sides, right?" Bessent then dropped a couple of positivity bombs.

While admitting that negotiating with China is probably going to be "a slog," Bessent added that President Trump's intention "isn't to decouple" the world's two largest economies. Bessent also said that the prospect of de-escalating tensions between the two nations "should give the world, the markets, a sigh of relief." Barron's reported that Bessent added that this de-escalation should begin in the "very near future."

More To It

Probably even more significant and possibly more impactful on markets than the Bessent news, were rumors running up and down Wall Street on Tuesday, and finally reported on by Politico later on, that the White House could very well be closing in on general trade agreements with both Japan and India. It could take weeks or months to finalize any documents, but a general agreement could be enough to delay or reduce tariffs between the U.S. and those two nations.

Memorandums of understanding are supposedly being put together between the U.S. and Japan and between the U.S. and India. These memorandums are said to be a broad architecture or framework for future deals. At least 18 nations, including those two countries, are said to be engaged at some stage of serious trade negotiation with the U.S.

The President

President Trump added to all of the market positivity with more than one comment made from the Oval Office on Tuesday.

On Fed Chair Jerome Powell

"I have no intention of firing him."

"I would like him to be a little more active in terms of his idea to lower interest rates. It's a perfect time to lower interest rates. If he doesn't, is it the end? No, it's not. But it would be good timing."

On China

"We're doing fine with China."

The president added that final tariffs on Chinese imports won't be "anywhere near" the 145% level where they are now. The president added, "It will come down substantially, but it won't be zero. We're going to be very nice and they're going to be very nice, and we'll see what happens."

Let Me Hear You Roar

Financial markets had a very strong day on Tuesday ahead of having a very strong overnight session as Tuesday night melted into Wednesday morning. The yield paid by the U.S. 10-Year Note actually dropped a bit. The U.S. Dollar Index moved higher. Gold actually took a breather. Stocks? Yeah... stocks roared. Let me hear your blood-curdling war cry. That's right, come get some.

The S&P 500 gained 2.51% on Tuesday as the Nasdaq Composite popped from a run of 2.71%. All of the small-to mid-cap indexes gained between 2.55% and 2.71% as the Philly Semiconductors took back 2.14% and the KBW Banks screamed 3.28% higher. Go banks! The KBW Regional Banking Index (smaller banks) was even hotter, up 3.41%.

All eleven S&P sector SPDR ETFs closed out the Tuesday session well into the green, led obviously by the Financials XLF at +3.31%, and followed by the Discretionaries XLY at +3.16%. Even the defensive-minded Staples XLP were up 1.42% on the day despite an eleventh-place finish on the daily performance tables.

Overwhelming Force

We all know that the surest way to existential peace is the ability to bring overwhelming force to the table. Equities brought overwhelming force to the marketplace on Tuesday.

Winners beat losers at the NYSE by roughly 10 to 1 and at the Nasdaq by about 9 to 2. Advancing volume took a commanding 88.9% share of composite NYSE-listed trade and an almost just as commanding 81.2% share of composite Nasdaq-listed activity.

Now, this is the best part. Aggregate trade increased by 10.4% on a day-over-day basis across NYSE listings and by 4.5% across Nasdaq listings. Aggregate trade was also up more than 10% across the membership of the S&P 500.

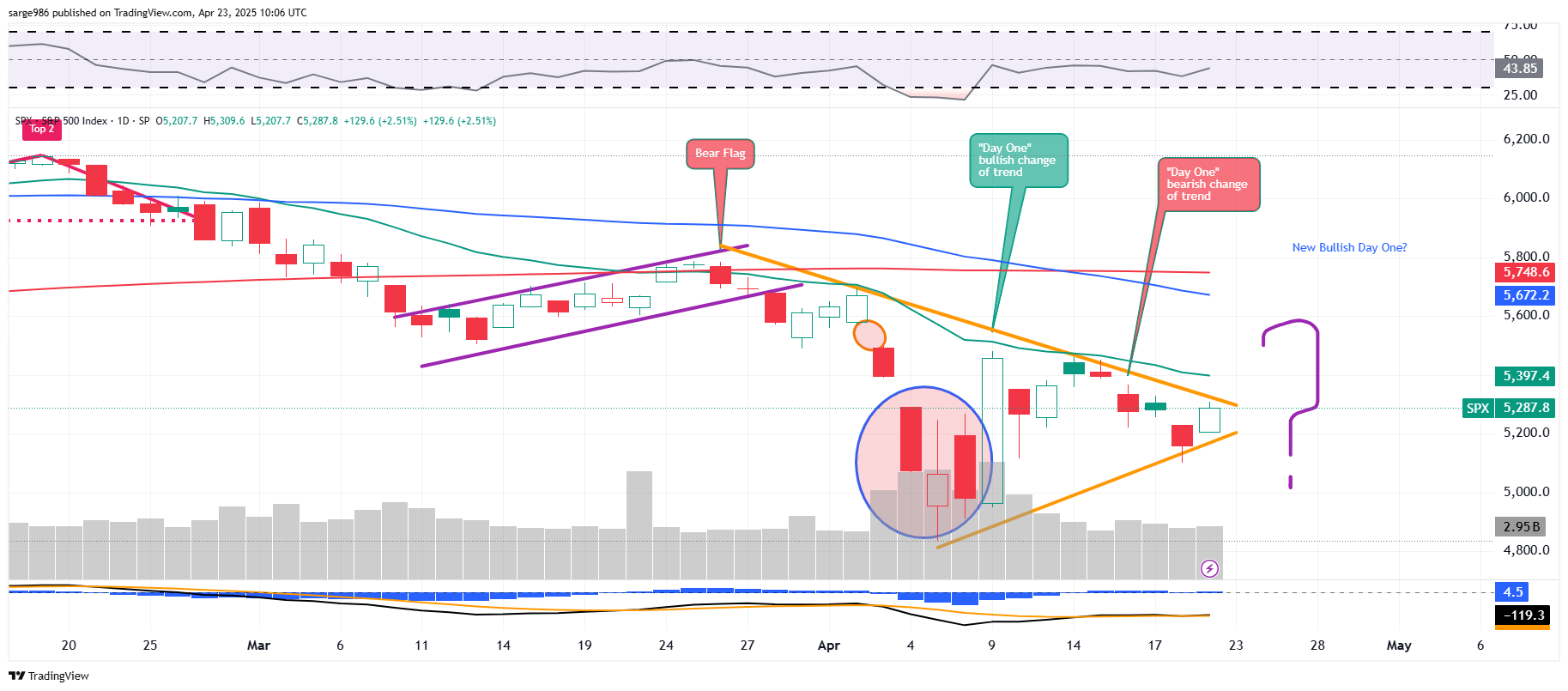

So, the big question is this: Do we have a ballgame? Do we have something to build on? Or was that a dead cat bounce? Psst... don't tell the goons on FinTV that there's no such thing as a dead cat bounce. That's just what talking heads say when they can't explain a rally. Everything happens for a reason.

So, what did we have on Tuesday? Was there too much time in between the bullish "day one" on April 9 for this to be a confirmation? Unfortunately, yes. Not only that, but the confirmation day has to extend the movement, and though we did experience an increase in trading volume, the index is still lower than it was two weeks ago.

Does this at least put the bearish "day one" of April 16 to bed, unconfirmed? The good news is that yes, that "day one" also dies in silence. Essentially, Tuesday, becomes the new bullish "day one."

Readers should note that a continuance of Wall Street's rally on Wednesday could force a breakout from the existing pennant formation that has been closing. Closing pennants are non-directional in that they often produce violent moves when there is a breakout.

Drum Roll, Please

I almost reacted with joy when I saw that the IMF (International Monetary Fund) downgraded their outlook for U.S. 2025 GDP growth to 1.8% from 2.7% (in January). Not that estimated economic growth of 1.8% is not realistic. It most certainly is. It's just that the IMF is almost always a day late and a dollar short.

Once that crew of economic misfits acknowledges a problem, it would not be surprising at all to see the football start moving in the other direction.

Send in the Clown

The clown show of the elites continues at the World Economic Forum. WEF founder Klaus Schwab is now under investigation by the very organization that he created after an anonymous whistleblower letter reached the Forum's board last week.

The letter raised concerns that the Schwab family may have mixed their personal affairs with the Forum's resources without proper oversight. The board decided to open an investigation during an Easter Sunday emergency meeting. Schwab opted to resign as chairman immediately, instead of staying on for what had been a planned period of transition.

Tesla Pops

Beleaguered electric vehicle manufacturer Tesla TSLA reported its quarterly financial results on Tuesday evening. The company had a lousy quarter. Nobody cared.

What mattered to investors was the return of CEO Elon Musk, or at least the return of his focus as a priority to Tesla's future success. Musk said, "DOGE work is mostly done and beginning in May, my time allocated to DOGE will drop significantly."

I did not go into those earnings long the stock, but I did grab some for an overnight rental as soon as I heard Musk's comments. I expect to take that quick profit this morning.

Layoffs

Intel INTC is up more than 4% overnight as Bloomberg News has reported that the firm is looking to reduce its headcount by more than 20% and that these plans will be announced this week. That would come to a rough 21,780 individual jobs lost, if my math is correct, and comes after the firm cut roughly 15,000 positions in 2024.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.81%.

07:00 - MBA Mortgage Applications (Weekly): Last -8.5% w/w.

09:45 - S&P Global Manufacturing PMI (Apr-Flash): Expecting 49.4, Last 50.2.

09:45 - S&P Global Services PMI (Apr-Flash): Expecting 52.6, Last 54.4.

10:00 - New Home Sales (Mar): Expecting 680K, Last 676K SAAR.

10:30 - Oil Inventories (Weekly): Last +515K.

10:30 - Gasoline Stocks (Weekly): Last -1.985M.

The Fed (All Times Eastern)

09:00 - Speaker: Chicago Fed Pres. Austan Goolsbee.

09:35 - Speaker: Reserve Board Gov. Christopher Waller.

14:00 - Beige Book.

18:30 - Speaker: Cleveland Fed Pres. Beth Hammack.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: T (.53), BA (-1.28), CME (2.79), GEV (.35), GD (3.48), NSC (2.68)

After the Close: CMG (.28), IBM (1.43), LRCX (1.00), LVS (.58), ORLY (9.87), NOW (3.84), TXN (1.10), URI (8.92)

At the time of publication, Guilfoyle was long LRCX, JPM and TSLA equity.