Odd End-of-Shutdown Rally Raises Questions About a Trump Liquidity Boost

Investors could be expecting the presidential administration to flood the market with money before midterm expectations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Well, we had a large “end of the shutdown” rally. Or maybe it was the “stimulus check” rally? Or maybe it was just pent up demand, China easing export controls on a few key rare earths/critical minerals, or simply dip buying after a relatively weak week for markets?

In any case, it was strong, but “slightly odd,” that reopening beneficiaries lagged the overall market (and even stimulus beneficiaries lagged).

Or maybe, and this makes the most sense, there is a view that the administration will do everything it can to flood markets and consumers with money and liquidity coming into the midterm elections.

I am not sure I agree with it, but for all the explanations of Monday's move (and what moved) it might make the most sense. I need to think about this, as any reason for caution would likely be outweighed by this “flood” of money and liquidity. I am not there yet, but I’m wondering if I’m just being stubborn. It seems too early to bet on this, but there were some indications that this theory merits attention.

Away from the re-opening (or “flood” of money and liquidity), there were several question marks facing this market that have not been resolved:

Seasonality is turning positive (but this market seemed to defy seasonality in September and October)

The AI valuation story: This has been the biggest question mark for a number of weeks. Mega caps dropping 10% or rising 10% based primarily on the market’s assessment of the value it is getting for its AI spend. The market is still largely behaving as though China offers no competition for the foreseeable future. It might be true, but it is a very consensus bet and doesn’t seem to account for the fact that China is better prepared on the electricity-generation side.

Slightly Higher Yields

The market (according to the WIRP function on Bloomberg) is down to pricing a 63% chance of a cut at the December Federal Reserve meeting. Coming into the October meeting, that was at 92%. It dropped to a 73% chance after the Fed meeting and press conference.

While 63% is still high enough and the Fed probably won’t disappoint markets, there is increasing risk that we get a pause.

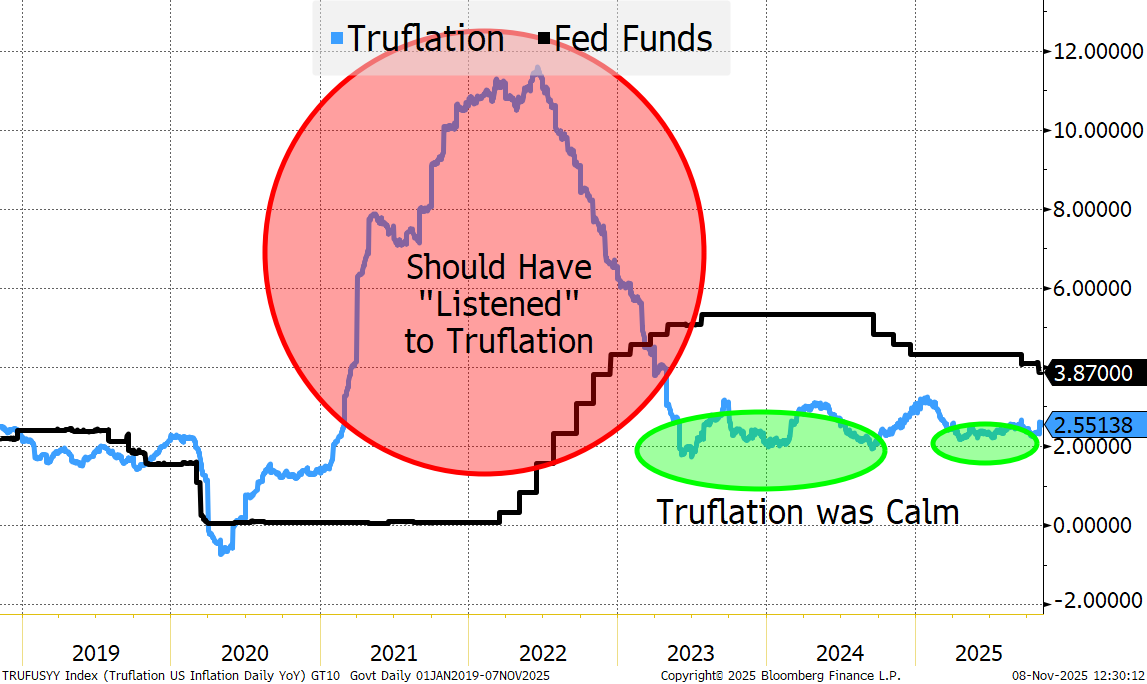

Inflation Is a Bit Stubborn

I keep a close eye on "truflation" as I think it is better at “real-time” inflation than the CPI data. It was showing inflation well before CPI was when the Fed was chanting “transitory.” It is ticking back up to 2.5% after being close to 2% for much of 2023 and 2024 and even parts of 2025.

Jobs data was “only” weak. ADP, at 42,000 jobs, might be close to the replacement rate on jobs (the number of jobs that need to be created to keep unemployment unchanged). Yes, the Challenger layoff numbers were awful, but that has never been a report that really drives markets (and would have been largely ignored if we had NFP on Friday, like we normally would have).

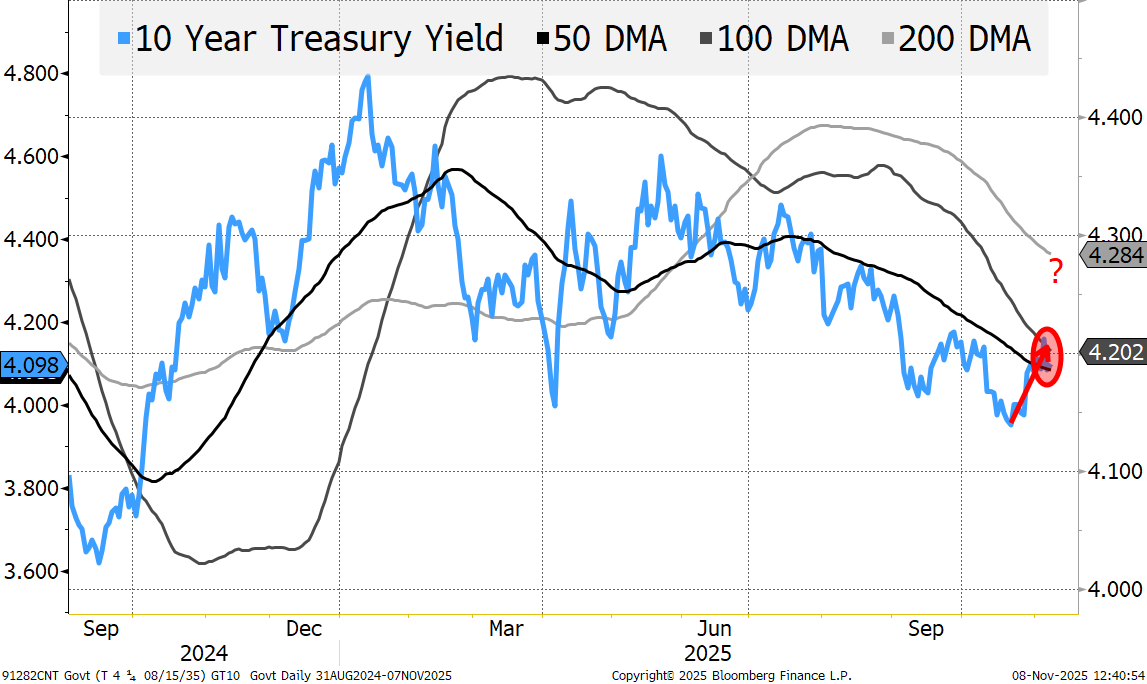

While I think the administration will do a lot to try and drive 10-year yields lower, they are poised, I think, to move higher.

As we break some resistance at the 50-day moving average, we could get to the 200-day which is “only” at 4.3%. Not a huge move, but potentially enough to disrupt the ongoing rally.

Finally, we have seen realized volatility increase, particularly in equities. And we are seeing some shifts in cross correlation between asset classes.

That combination could lead to some risk production from risk-parity strategies (strategies that try to manage a portfolio of stocks, bonds, commodities, and even crypto) to a certain level of volatility.

Monday’s “re-opening” rally, or whatever you want to call it (and I think it has more to do with expectations of a lot of government support), is too strong to ignore. But I think we will revisit some of the issues listed above and renew the weakness we saw the past week (or two).

Any weakness will create buying opportunities, especially in the "production for security" (ProSec) names.

I did reduce my exposure to closed-end muni funds — I was pretty much “max long” them in my income portion and think there will be a better opportunity to buy them back. I’m still overweight, just not “max” long them any longer.