Nvidia Steps Up to the Plate

The chip maker releases perhaps the most important earnings report of the quarter tonight, the market rallies big Tuesday, and we chart what could be a 'New Day One' reversal.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Tonight's the night. Racy hit song sung by Rod Stewart in the mid-1970s? No. Possibly the most important earrings release of the entire quarter? Winner, winner... chicken dinner. Tonight, a day after Wall Street experienced a roaring stock market rally, the chip designer that had become synonymous with gaming, crypto-currency mining, then the data center and cloud computing and now generative artificial intelligence will go to the tape with its fiscal first quarter numbers.

For that three-month period, which closed in late April, Nvidia NVDA is expected to have generated an adjusted earnings per share of $0.75 on revenue of roughly $43.25 billion. If matched (unlikely), results like this would be good enough for earnings growth of 23% on revenue growth of 66%. That would be, by most measures, simply outstanding, even if decelerating on a year-over-year basis, quarter after quarter. I suppose that cannot be helped, given the law of large numbers. We went into this yesterday in my piece here at the TheStreet Pro.

Perhaps, from a markets-based perspective, the key items will be, the reality (or not) of the company's April projection of a $5.5 billion inventory-based charge after Pres. Trump tightened export controls for high-technology type products headed for mainland China that could be used for military purposes. Does the new chip that Nvidia recently announced it created just for China change that projection? Or beef up guidance for revenue generation? Soon enough, we'll find out. Salesforce CRM may release in near obscurity tonight, which would be a bit odd.

Marketplace

On Tuesday, in response to the president having delayed the increase of tariffs on imports from the European Union from June 1 to July 9, capital that had been withdrawn from U.S. financial markets on Friday, returned. In fact, more capital returned than had left. Tuesday was a huge day. Treasury debt securities rallied, compressing yields, as by day's end, the U.S. Ten-Year Note paid just 4.45%. This allowed for flows to move back into stocks as well.

The S&P 500 gained 2.05% for the session, as the Nasdaq Composite rallied for a run of 2.47%. Tuesday's rally was quite broad in nature as the Dow Transports gained 2.03%, the KBW Banks popped for 2.28% and all of the small to mid-cap indexes ran anywhere from 2.14% to 2.57%. The semiconductors were strongest of all with the Philadelphia Semiconductor Index up 3.38% and the Dow Jones US Semiconductor Index up 3.23%. The group was led by Teradyne TER, Arm Holdings ARM, and Marvell Technology MRVL, all of whom gained more than 5%.

Breadth

All 11 S&P sector SPDR exchange-traded funds closed out the Tuesday session well into the green, led by the Discretionaries XLY at +2.95%, and followed by Technology at +2.38%. The Utilities XLU finished in 11th place for the day and still rallied for 0.75%. Defensive sectors took three of the bottom four rungs on the daily performance tables. This probably had something to do with the surprisingly strong May result for the Conference Board's Consumer Confidence survey.

Winners beat losers at the NYSE by better than a 6-to-1 margin and at the Nasdaq by a rough 5 to 2. Advancing volume dominated the day, taking an 82.9% share of composite Nasdaq-listed trade and an 82.4% share of composite NYSE-listed activity. On a day-over-day basis (from Friday), aggregate trading volume increased by 15.1% across NYSE-listed securities and by 2.3% across Nasdaq-listed securities. Trading volume across the membership of the S&P 500 also reached its 50-day simple moving average for the first time since May 13.

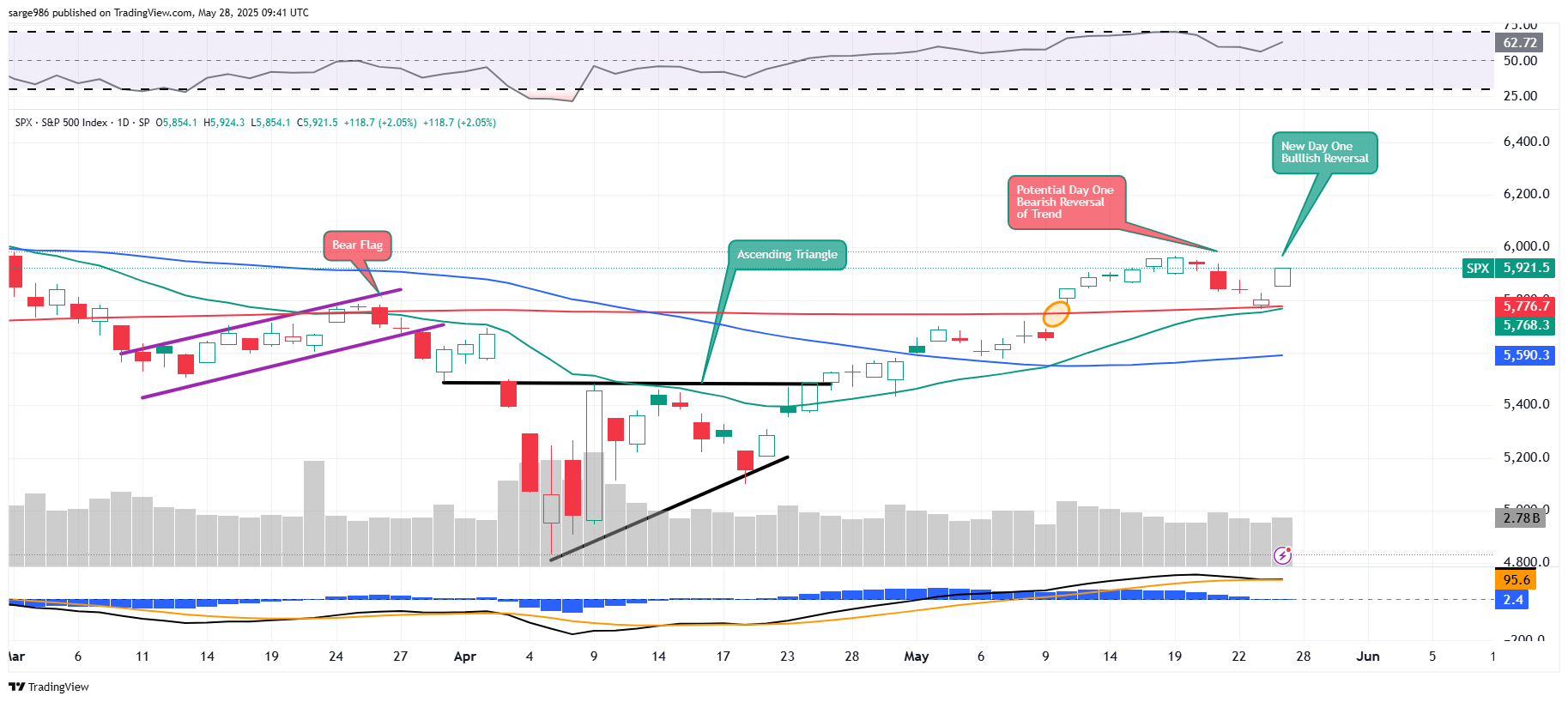

New 'Day One'?

You bet your tail that Tuesday was a new potential "Day One" bullish reversal:

Readers understand that Tuesday terminated the bearish set-up created last Wednesday. Now, as investors and traders, we hope for or look forward to a pause and then a second convincing rally on volume as confirmation that an upward change of trend after just four "down" days has indeed occurred. Nvidia will likely have something to say about this. So might the "Big Beautiful Bill" which is big, but whose beauty is debatable.

Tomorrow

The sun'll come out

Tomorrow

Bet your bottom dollar

That tomorrow, there'll be sun

Just thinkin' about

Tomorrow

Clears away the cobwebs

And the sorrow 'til there's none

- Charnin, Strouse (1977), from "Annie"

Confidence Soars

You kids see that Consumer Confidence survey for May released by the Conference Board on Tuesday? Wow! The headline number increased by 12.3 points to 98, making May the largest increase from the month prior for the series in four years. Not only was this result significantly higher than consensus view, which was down around 87, but this was well above the highest projection made that I saw anywhere, which was 91.3.

While, within the survey, consumer opinion on their present situation improved nicely, it was consumer expectations for the next six months that really took off, surging by the most since the year 2011. The improvement in confidence was clear from April to May across all age, and income demographics as well as across all political affiliations. That last one is a sharp change from recent trends. Additionally, inflation expectations dropped from 5.9% to 5.3%. Rock on.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.92%.

07:00 - MBA Mortgage Applications (Weekly): Last -5.1% w/w.

08:15 - ADP Employment Report (Dec): Expecting 145K, Last 127K.

08:55 - Redbook (Weekly): Last 5.4% y/y.

10:00 - Richmond Fed Manufacturing Index (May): Expecting -9, Last -13.

4:30 p.m. - API Oil Inventories (Weekly): Last +2.499M.

The Fed (All Times Eastern)

04:00 - Speaker: Minneapolis Fed Pres. Neel Kashkari.

2:00 p.m. - FOMC Minutes.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ANF (1.37), DKS (4.38), M (.15)

After the Close: HPQ (.80), NDSN (2.36), NVDA (.73), CRM (2.55), S (.02)

At the time of publication, Guilfoyle was long NVDA equity.