Nvidia, AMD to Give Up Chunk of Chip Revenues, Intel CEO Goes to D.C., Bowman Speaks

Let's take stock of a reported plan for Nvidia and AMD to share some chip revenues from Chinese exports; also more Fed chatter, an S&P chart and the week ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The Financial Times reported Sunday that last week both Nvidia NVDA and Advanced Micro Devices AMD had obtained export licenses for their respective, Biden-era compliant, AI-capable processors, for Chinese customers. That was expected. What was not expected was that the FT reported that Nvidia had agreed to pay 15% of revenues driven by exports of its H20 chips to China. Apparently, AMD has agreed to those same terms for exports of that its MI308 chips to Chinese customers as well.

The Financial Times had reported earlier that the Commerce Department had started issuing licenses for such exports this past Friday. As of Sunday evening, neither Nvidia or AMD has confirmed nor denied the story. I have not been able to confirm this, but according to the Financial Times story, no U.S. company had ever agreed to split revenue with the federal government before as a condition of gaining access to a foreign market through an export license.

In addition, Reuters reported on Sunday morning that an article from a Chinese state media-affiliated source had stated that Nvidia's H20 chips pose a security risk as there is a "backdoor" through which the chips could be shut down remotely. Remember, Nvidia designed these chips specifically for Chinese markets, and on that count, the company did respond. In an emailed statement on Sunday, Nvidia stated, Cybersecurity is critically important to us. Nvidia does not have 'backdoors' in our chips that would give anyone a remote way to access or control them."

In Other Semiconductor-Related News....

Intel INTC CEO Lip-Bu-Tan is expected to be in Washington on Monday to visit the White House. This comes after Pres. Trump called for his dismissal or resignation last week in response to rumors of his ties to Chinese businesses. The president and the CEO are expected to have a broad-based conversation.

Tan will try to explain his professional background and demonstrate to the president his commitment to the security of this country. Tan is a Malaysian-born U.S. citizen who led Cadence Design CDNS until 2021. Cadence Design agreed to plead guilty last week and pay more than $140 million to resolve charges made by the Department of Justice that the company had sold chip-design products to a Chinese military university.

Let's Go

She's drivin' away

With the dim lights on

And she's makin' a play

She can't go wrong

She never waits too long

- Ric Ocasek (The Cars), 1979

She Said...

Fed Gov. Michelle Bowman spoke to the Kansas Bankers Association summit in Colorado Springs on Saturday. Readers will remember that Bowman was one of two members of the Fed Board of Governors who dissented in favor of cutting short-term interest rates from the Federal Open Market Committee decision on July 30 to hold rates steady.

First she set up her case and then explained why Powell's FOMC made the wrong policy choice despite the fact that two governors dissented and three failed to agree (Kugler abstained and then later resigned her position) with the consensus. On Saturday, Bowman said, "Although the unemployment rate remained historically low at 4.2 percent in July, the latest employment report confirmed some of the signs of fragility and reduced dynamism in the labor market that I discussed at last week's FOMC meeting without the benefit of having seen the July report. Taking action at last week's meeting would have proactively hedged against the risk of a further erosion in labor market conditions and a further weakening in economic activity."

Then Bowman commented on inflation, which is something we'll learn more about this week and balancing policy: "In terms of risks to achieving our dual mandate, as I gain even greater confidence that tariffs will not present a persistent shock to inflation, I see that upside risks to price stability have diminished. With underlying inflation on a sustained trajectory toward 2 percent, softness in aggregate demand, and signs of fragility in the labor market, I think that we should focus on risks to our employment mandate."

Finally, Gov. Bowman throws down the gauntlet, "My Summary of Economic Projections includes three cuts for this year, which has been consistent with my forecast since last December, and the latest labor market data reinforce my view."

Last Week...

Domestic equity markets enjoyed their best week, at least at the headline level since late June, just one week after suffering their worst week last week since late May. What happened? The macroeconomic calendar was light. That said, the Institute for Supply Management did release some rather nasty looking service sector survey results for July, coming off of a truly awful looking July labor market report the Friday prior to last. This pushed the markets forward with increased expectations for lower short-term interest rates by mid-September.

After that, in addition to an earnings season that has been much, much better than expected, Apple AAPL patched things up with Pres. Trump by pledging an extra $100 billion in domestic investment on top of the $500 billion already promised, while also agreeing to manufacture more parts for its mobile devices in the U.S.

By week's end, hopes for peace were abundant and put nearly all investors in a better mood as Pres. Vladimir Putin of Russia had agreed to meet with Pres. Trump to speak on a potentially peaceful resolution to the Russo-Ukrainian War. This came just after the U.S. president had brokered a peace deal between Armenia and Azerbaijan.

Weekly Numbers

What the major to mid-major U.S. equity indexes did last week markets, after failing to confirm a bearish change of trend, headed back in a northerly direction...

- The S&P 500 gained 0.78% on Friday and 2.43% for the week.

- The Nasdaq Composite gained 0.98% on Friday and 3.87% for the week.

- The Nasdaq 100 popped for 0.95% on Friday and gained 3.73% for the week.

- The Russell 2000 nudged just 0.17% higher on Friday but gained 2.38% for the week.

- The S&P Smallcap 600 gained just 0.25% on Friday, gaining 2.19% for the week.

- The S&P Midcap 400 lost 0.01% on Friday, but gained 0.63% for the week.

- The Dow Transports lost 0.41% on Friday, but added 1.56% for the week.

- The Philly Semis gained 0.79% on Friday and 2.72% for the week.

- The KBW Bank Index oared 1.19% on Friday, flipping the week to the upside by 1.05%.

On Friday, nine of the eleven S&P sector SPDR ETFs closed out the session in the green, led higher by Technology XLK. the Financials XLF and Health Care XLV. The REITs XLRE were the day's losers on Friday. For the week, eight of the 11 S&P sector SPDR ETFs traded higher, led in that direction by the Discretionaries XLY, followed by Tech. Energy XLE and Health Care struggled over the five-day period.

Valuation

Using data provided by FactSet, the S&P 500 went into this weekend trading at 22.1- times forward looking earnings, down from 22.2-times the week prior. This is still well above the five-year average of 19.9-times and the ten-year average of 18.5-times for the index. The S&P 500 is also trading at 27.7-times trailing earnings, down from 27.8- times last week. This is also well above the five-year and ten-year averages of 25-times and 22.6-times respectively.

Q2 Earnings

Second quarter earnings season is now nearly completed though we are still waiting on most of the retailers and some tech stocks including Nvidia. According to FactSet, for the second quarter, with 90% of S&P 500 member companies having already reported, 81% of member companies have beaten earnings expectations, while 81% have also surprised the street on revenue generation.

Consensus for Q2 SPX-wide year over year earnings growth is currently at 11.8%, which is up sharply from 10.3% last week and up from just 4.8% a few weeks ago. Q2 revenue growth is now seen at growth of 6.3%, up nicely from 6% last week and 4.2% a few weeks back. For the second quarter, Communication Services are easily leading the way, having grown earnings by a whopping 45.8%, followed by Tech at +21.3%. Just two sectors are still projected to have suffered a year over year contraction in earnings, easily led lower by Energy (-17.6%). The Utilities and now the Staples have moved from contraction to growth over the past two weeks.

For the full calendar year of 2025, Wall Street now sees S&P 500 earnings growth at 10.3%, up from 9.9% a week ago. Expectations for full year revenue growth are now at 5.8%, up from 5.6% the week prior.

Interestingly, FactSet pointed out this weekend that the term "recession" has been cited on just 16 earnings calls across the S&P 500 this earnings season. During the Q1 earnings season, the term was cited on 124 calls. The five year average is 74 times. Better times ahead? Black swan coming? I'll go with door number one.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the third quarter up to growth of 2.5% (q/q, SAAR) from 2.1% last week. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth now stands at 2.02%, down from 2.12%, while the Cleveland Fed's model for the third quarter stands at growth of 1.93%. The St. Louis Fed has still not yet released an initial GDP estimate for the third quarter.

Fed Funds Futures

The next scheduled FOMC policy decision is still more than a month away and will not take place until Sept. 17. That said, the symposium at Jackson Hole is scheduled for next week, Aug. 21 through the 23rd. If the Fed Chair is going to pivot publicly, it will happen at Jackson Hole.

Fed Funds Futures markets trading in Chicago are currently pricing in an 88% probability for a quarter point rate cut on Sept. 17, and a 57% likelihood for an additional quarter point cut on Oct. 29. These markets are now pricing in just a 45% probability for a total of three-quarters of a point worth of rate cuts by year's end, down from 53% at this time last week. This week's data on July inflation is going to really matter.

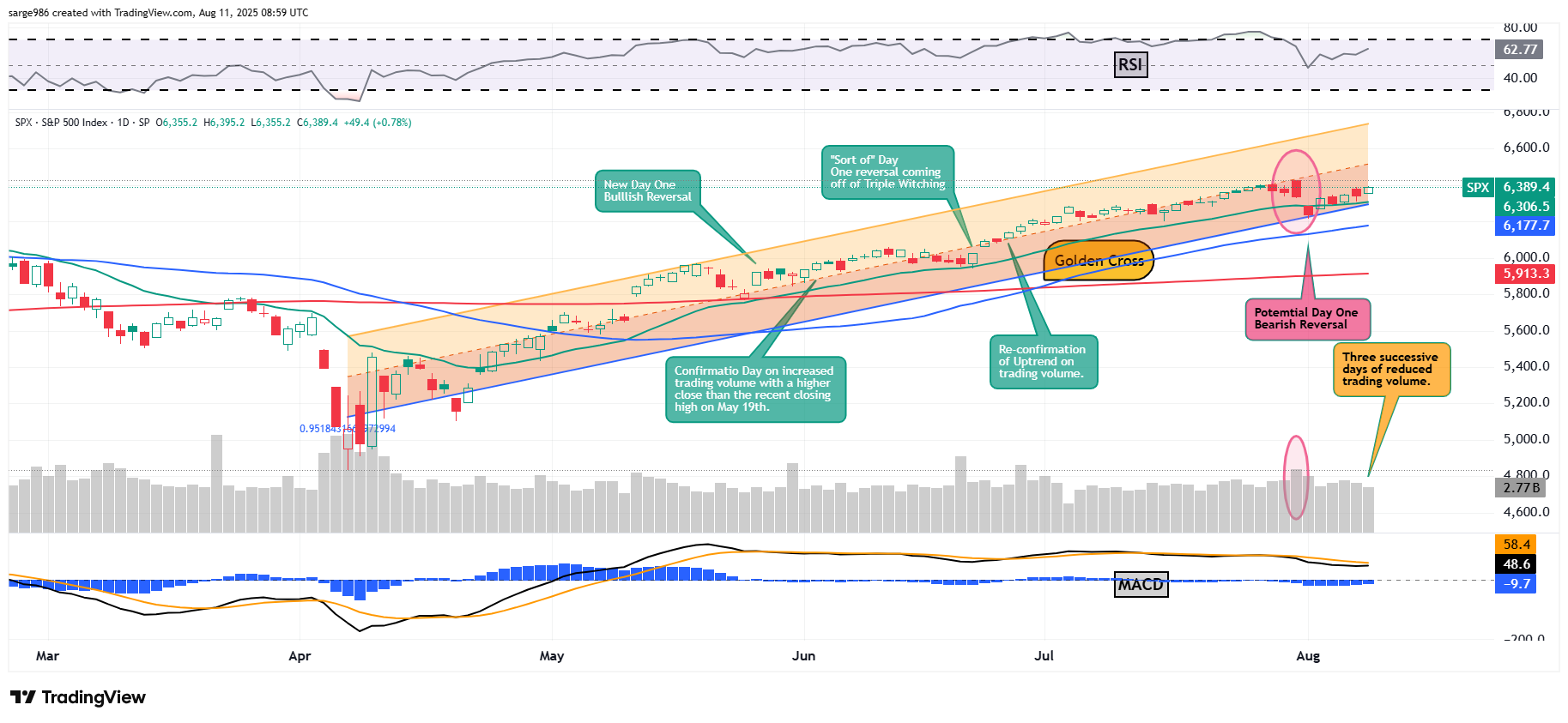

The Chart...

Domestic equity markets went into this weekend bearing much better sentiment than had been expressed a week prior. On Friday, Aug. 1, the S&P 500 tumbled after that weak July jobs report that turned out to be a surprisingly weak report covering three months after those huge revisions. That was a potential "Day One" bearish reversal of trend.

I reminded readers a week ago that for a bearish change of trend to be confirmed, we needed to see a pause, before experiencing a renewal of selling pressure on increased volume. The markets got more than a pause as readers can see above. Throughout the entirety of last week, even on the red candle days, every single day of last week resulted in a higher high and a higher low than the day prior. That's bullish. However, readers will also notice that from Wednesday into Friday, aggregate trading volume across the membership of the S&P 500 ebbed. That's kind of bearish. Hmmm.

Interestingly, the index did regain its 21-day exponential moving average last Monday after finding support on August 1st at the lower trendline of our Raff Regression model. Those are positives. Relative Strength has recovered and is once again quite robust without ever dropping below a neutral reading. The daily Moving Average Convergence Divergence is now in much better shape as well. That said, within that daily MACD, the histogram of the 9-day exponential moving average is still in negative territory, which could be short-term bearish.

Additionally, while the 26-day EMA is currently above the 12-day EMA, that 12-day EMA (black line) curled upward going into the weekend. Traders should find out early this week, just how meaningful that curl is. In short, the bulls need to see that black line move above the gold line while the blue field inched up towards the zero-bound.

What's Ahead?

Interesting week ahead for us traders and investors. Earnings season will take something of a break this week ahead of heating back up next week. However, this will be an important week macroeconomically, with a focus on the current state of inflation. That matters with the Fed's Jackson Hole shindig lined up for next week. Additionally, peace has at least a chance of making headlines this week. How that does or does not work out may be how this week is remembered in hindsight. Trade deals are also said to still be trickling in for those nations that got left behind last week.

The domestic macroeconomic calendar will be hot this week. The focus will be on inflation. The beleaguered Bureau of Labor Statistics will release its July consumer price index data on Tuesday morning followed by that same agency's publication of July producer price index on Thursday morning. On Friday morning, the Census Bureau will publish July Retail Sales. Later that same morning, July Industrial Production and Capacity Utilization will cross the tape courtesy of the Federal Reserve Bank. Later Friday, the University of Michigan will release the preliminary results of its August survey on Consumer Sentiment and consumer inflation expectations. The Atlanta Fed will revise their Q3 GDPNow model late this Friday morning.

The Federal Reserve appears to be rather quiet this week. I currently have just six public appearances to be made by Fed officials on my radar for this week. Not a single one of them is to be made by a member of the Board of Governors. The headliners this week, unless there is a change to the schedule, are probably Kansas City Fed Pres Jeffrey Schmid on Tuesday morning and Chicago Ged Pres Austan Goolsbee on Wednesday afternoon as both Kansas City and Chicago hold policy voting rights this year.

The earnings calendar will thin out this week. That does not mean that there will be no headline level firms reporting, just a lot less of them. Former meme stock AMC Entertainment AMC will go to the tape this afternoon followed by CoreWeave CRWV on Tuesday afternoon. On Wednesday afternoon, we'll hear from Cisco Systems CSCO followed by Deere & Company DE and Tapestry TPR on Thursday morning. Finally, Applied Materials AMAT will wrap up the week's earnings on Thursday evening.

Finally, the week's main event will occur this coming Friday when Russian Pres. Vladmir Putin travels to Alaska to meet with Pres. Trump. This is quite an overture by the Russian president to travel to U.S. soil, which would be a huge win for the Trump administration if the U.S. president can broker the start of an actual lasting truce in eastern Europe. The Energy sector will certainly be impacted by the perceived outcome of this meeting as will defense and aerospace stocks as an industry

Economics

(All Times Eastern)

No significant domestic macroeconomic data scheduled for release.

The Fed

(All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: FNV (1.12)

After the Close: AMC (-.08), CE (1.40)

At the time of publication, Guifoyle was long NVDA, AMD, CSCO equity.