Nothing Good Happens for Crude Oil Bulls Under $65

We've received a plethora of pushback on our bearish crude oil thesis, so let's address many of the standard arguments being made by crude oil bulls.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The oil market is popular among speculators due to its volatility, liquidity, and familiarity, but it is one that often confounds even the most astute analysts. There are two primary reasons for this: the supply of oil is at least partially dictated by a cartel, and it is primarily produced by a region of the world prone to unpredictable political violence.

Sometimes analysts get caught up in the supply side of the equation and ignore the simple fact that demand is not guaranteed. We are only five years away from the pandemic-induced government shutdown of the global economy, in which demand disappeared overnight. We will probably never see that again in our lifetimes, but a recession is somewhat likely, and that is all it will take to thwart energy demand.

Lastly, technology is deflationary. Even in the absence of a recession, electric and hybrid vehicles are continually improving and will eventually offer genuine competition to combustion engines. Similarly, gas-powered cars now come with an Eco Mode and are generally more fuel-efficient in all driving modes. Meanwhile, Artificial Intelligence may create a resurgence in the work-from-home trend or may even replace workers who currently travel to the office or distant locations to conduct business.

We don’t believe oil prices will remain low forever, but commodities tend to experience bear markets more frequently and for more extended periods than bull markets. We aren’t prepared to put this bear market into hibernation.

In recent months, we have been receiving a plethora of pushback on our bearish crude oil thesis. In this article, we will address many of the standard arguments being made by crude oil bulls.

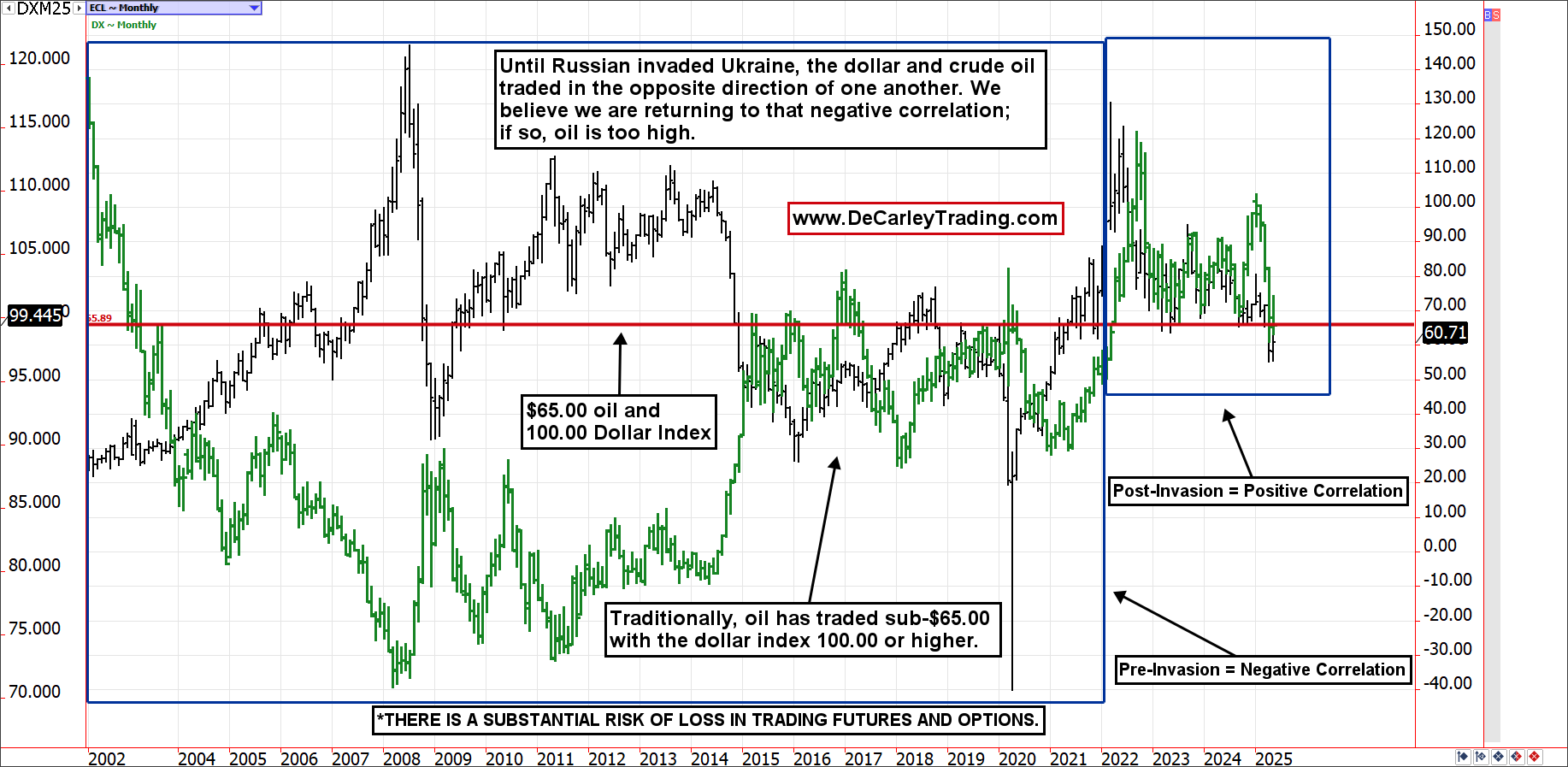

$65 Was the Floor. Now It Is the Ceiling.

Since the March 2022 highs were posted, the oil market has been in a failed rally mode. However, for years, selloffs were contained at $65.00 per barrel compliments of technical support, but more importantly, the OPEC put.

Like clockwork, OPEC production cuts were extended, or the extension was vocalized each time prices approached the mid-$60.00s, this jawboning habitually reversed prices higher. There is a good reason for this: OPEC knows that nothing good happens for the crude oil bulls when the price is below $65.00.

Historically, $65.00 per barrel has been a pivotal price for the crude oil market. The 2014 break below $65.00 continued into the high $20.00s, and the 2018 break eventually ended with the plunge into negative crude oil prices a few years later, in April 2020.

If the oil market can’t climb meaningfully above $65.00, gravity will come into play. We expect the low-$50.00s to high-$40.00s to be seen. After all, during Trump 1.0, the oil market spent most of its time trading below $65.00.

What About the Weaker U.S. Dollar?

The correlation between crude oil and the U.S. dollar has been abnormally positive since the Russian invasion of Ukraine. Still, it seems to finally be normalizing to a negative correlation (dollar up, oil down, and vice versa). For instance, if I examine the correlation between these two assets over the past 180 trading days, they have been trending in the same direction approximately 70% of the time. Conversely, if I examine the data from the last 30 days, they are almost exactly uncorrelated, with a correlation coefficient of zero.

I suspect the data is shifting back to the historical norm; if so, we should see this relationship fall into negative territory by next month. This would mean continued weakness in the greenback would be supportive for oil, but dollar strength would pull oil prices lower. The U.S. dollar appears to be setting up for a significant rally, which could hinder any attempts at a crude oil rally (read our previous article for details on this opinion).

What About the Cost of Production?

The market doesn’t care about the cost of production; nobody is guaranteed a profit. Therefore, for some producers, oil being below the cost of production is irrelevant.

U.S. producers face a cost of about $43 for offshore drilling and moderately higher for shale and conventional oil ($46 to $50). Yet, some operators believe the cost is closer to $60.00 to $65.00.

I have some opinions on this. My parents were in the oil business, and my brother still is. It has been my observation that the oil industry is far from efficient. There are contractor kickbacks, overcharges, and irrational decisions made by middle management, who prioritize quarterly bonuses over operating efficiency. I concede that all large businesses and industries have this issue. Yet, from my perspective, the oil industry often operates in obscene Cost of Goods Sold (COGS) territory for no particular reason other than it has gotten away with it for decades.

Obviously, if a producer truly can’t sell oil at a price that exceeds their cost of production, they will hold back. However, the U.S. is the largest producer in the world, but it also incurs the highest production costs. Some Middle Eastern producers have the luxury of lower extraction costs. Saudi Arabia is believed to have a breakeven point of $42.00 per barrel, but fringe producers are said to have costs as low as $10.00 to $20.00.

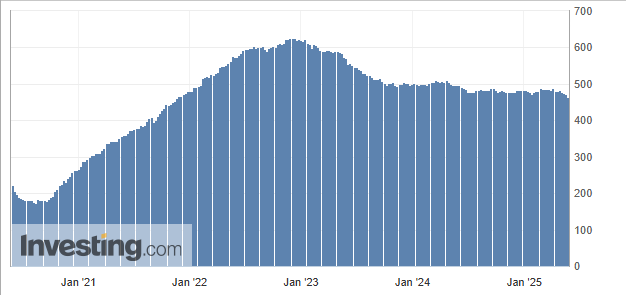

What About the Rig Count?

U.S. shale producers have started to lightly tap the brakes; we can see this from the Baker Hughes rig count, which has been tapering off. Yet, we don’t believe this changes the narrative for oil.

For starters, crude oil rigs in the U.S. have fallen to 465, down from 473 in the previous week, the lowest since November 2021; yet they are still double what was seen in 2020 and only a mere handful of fewer rigs in operation relative to what has been a stable count since late 2023. Furthermore, production remains at or near all-time highs, despite a moderate decline in the number of rigs.

Even more compelling, the U.S. has been bringing more barrels to market with 490 rigs than it has with almost double that pre-2020. In short, technology enables us to produce more with less. Only a dramatic decrease in rig count would lead me to believe that data point was bullish for the price of oil.

What About AI Demand for Energy?

In the macro view, AI will require energy, however, nuclear power is suddenly a real competitor to fossil fuels, including uranium and thorium. The U.S. is behind the curve in this department. Multiple nuclear plants were shuttered in the hope that solar and wind energy would offer a safer alternative, but this premise has not materialized as some had expected.

The Trump administration is attempting to revive nuclear power, but the reality is that even if the regulatory burden is eliminated, the time to build, test, and employ such a facility is likely 10 to 15 years. There are SMRs (Small Modular Reactors) that will speed up the process to 4 to 6 years, but even those are far from an overnight solution. Nevertheless, the AI demand for energy might also emerge 5 to 10 years down the road, rather than being an immediate phenomenon.

Don’t forget the lessons learned in the dot-com bubble. Like AI, the internet was expected to change the landscape as we knew it. It did, but only after an initial boom and bust cycle.

Another take on this is AI and technology are deflationary; more efficient vehicles, fewer workers traveling to the office or distant locations, etc. In short, AI alone is not a reason to be an oil bull at this time, in my eyes.

Will Deregulation Matter?

The U.S. has a debt problem, we are spending more than we are taking in. Yet, the only thing going for us is our balance sheet, which has not been monetized to its potential.

The United States is sitting on substantial resources, including rare earth minerals and fossil fuels. Much of these resources have been untouchable due to environmental regulations but if there is some reasonable easing in this category and federal lands are opened for mining and drilling, the country has an off ramp to the debt crisis, and the U.S. will be well-supplied with energy sourced from uranium, thorium, and fossil fuels. This is not only deflationary but also bearish for the oil market.

Whether or not this is a good idea from an environmental standpoint is up for debate. I have had a front-row seat to this argument for years, due to my upbringing in the oil industry in the southeastern corner of Utah. This part of the country is resource-rich, boasting an abundance of uranium, natural gas, and crude oil, and is also one of the world's largest sources of helium gas. Yet, it happens to be (arguably) one of the most beautiful landscapes in the country, home to multiple national parks and an unfathomable amount of federally owned land that has been mostly blocked from public or private use.

In some instances, the government blocked mining and drilling but openly promoted the land as a tourist destination, which seems to have done significant harm to the land they aimed to protect. I don’t know what the correct answer is, but it is probably somewhere in the middle of the current scenario and what the oil and gas companies would hope for. In any case, the U.S. has financial and national security incentives to tap into natural resources, and if it does, supply will be ample for years to come.

The Bottom Line

As the adage goes, picking bottoms leads to stinky fingers. If oil goes up from here, it will likely be due to an unforeseen catalyst. For now, the die has been cast, and the bear market is likely to continue.

Even if we are wrong about a near-term U.S. dollar rally, the price of crude oil has historically traded between $30.00 and $65.00 in a high-dollar environment, not $65.00 and $100.00. Despite the recent plunge, the U..S dollar is at a relatively high valuation compared to previous decades. This alone is justification for lower oil prices.

Furthermore, the chart shows little promise unless oil prices rise above $65.00 in the coming days. The longer oil trades below this level, the heavier the market will become.