Nasdaq 100 Heading Lower as Market Seeks Concrete Evidence of Trump 'Wins'

Investors have a hard time factoring in political intervention and government policy is driving the headlines.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We listed some current concerns about the direction that policy is taking and the potential impact on markets on Friday in our post-NFP missive.

I want to expand on that and take it in a slightly different direction, but let’s set the stage for my current thinking:

We are in a moment where government policy is driving headlines. While not as extreme as either the Great Financial Crisis (GFC) or European Debt crisis, it is starting to resemble that and has the potential to increase in terms of moving markets.

Around the time of the GFC (actually, in 2007) one of the biggest and best quant funds told me something that is crucial here. They said that they can model a lot, but they are not good at modeling government intervention. It is both unpredictable and has huge size associated with it — really driving markets. With AI, maybe it is easier, but I think that we tend to underestimate the power and that means things like technical analysis and other tools may be less useful as they are not designed to work around government intervention. While you might argue that tariffs and wars aren’t government intervention, it isn’t too far off.

Intervention often needs to happen. Initially the threat of it can work, but ultimately it tends to reach a point where it needs to be implemented to sustain markets positively. Think about the TARP vote, but if you lived through it, you saw each attempt to soothe markets provide less of a lift and last for a shorter period of time. The same happened in Europe during the European Debt Crisis. Admittedly, Mario Draghi finally won with his “whatever it takes” moment, but you saw the same pattern of jawboning being less and less effective.

So my mindset is that technicals are apt to break and we need to see really positive headlines to propel markets higher — not the mere promises of good things to come (which is what we have been largely getting). I want to be clear on my mindset as it will help you interpret my views and determine whether you agree with them and think they will continue to be useful navigating this market (at its simplest it has been short QQQ and long FXI and KWEB) and own muni-closed end funds in your income portfolio.

I need concrete evidence of “wins” to change my view, or for some reason the market to accept that Trump’s steps will lead to massive success. Though even there, I think the success might be a return of industry and rebuilding the middle class, which might not do much for equity valuations.

Market Risks of Deglobalization

We have already addressed the risk that the positive side of negative trade balances may have been capital flows, allowing U.S. markets to prosper. Could that be changing?

Somewhere between 25% and over 40% of revenue for the S&P 500 companies comes from outside the U.S. AI came up with 28% and someone I know well (and trust more than AI) Torsten Slok produced a slide published on February 5, showing “41% of revenue in the S&P 500 companies comes from abroad."

We haven’t even begun to see how the rapid changes in tariffs and even potential in geopolitical alliances will affect companies. I think that is the potential next leg to drop in markets. As time goes by, we will be made painfully aware that U.S. Corporations and the U.S. government are not one in the same, and corporations may find it increasingly difficult to manage in this rapidly evolving world.

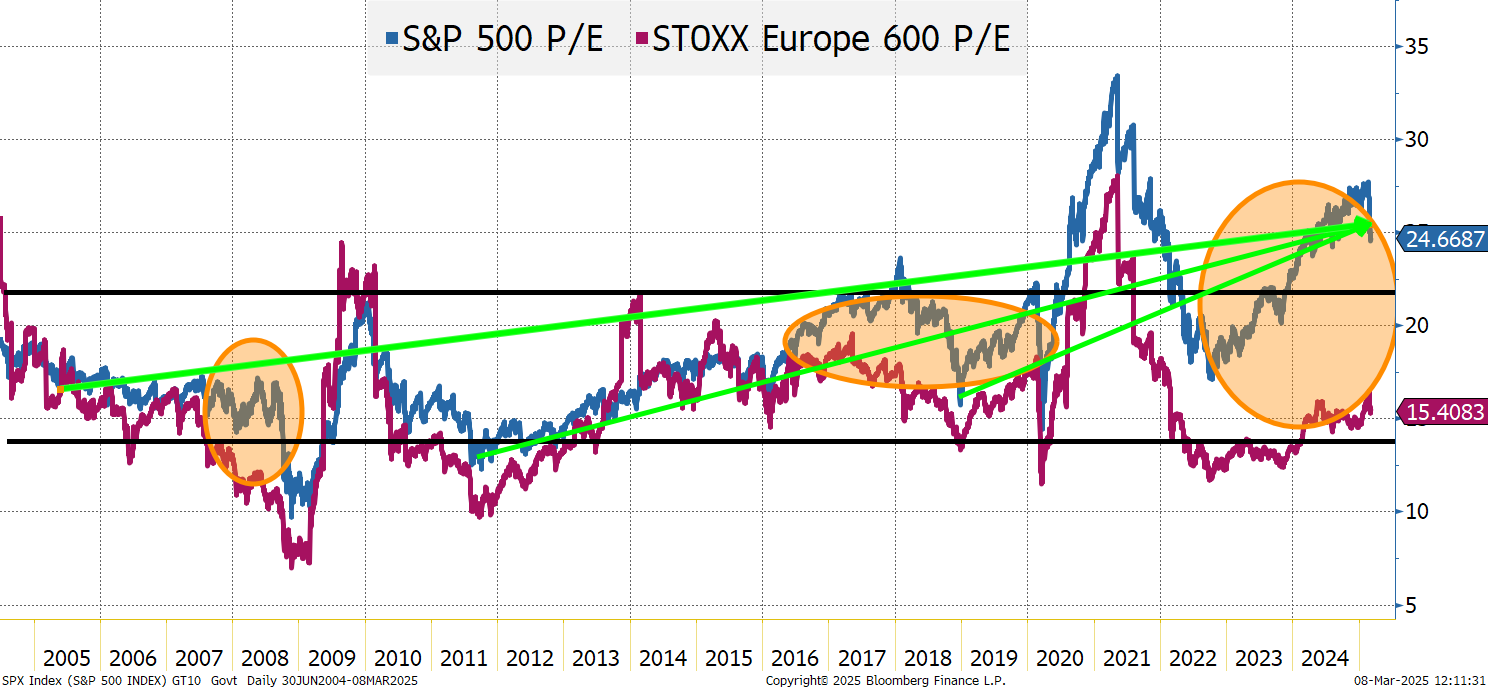

I rarely think in terms of P/E rations, but it seemed important to bring up here.

There have been a few periods where the average P/E ratio between the S&P 500 and the STOXX 600 has diverged. The ones where the U.S. was significantly higher than Europe have been highlighted in orange. The recent divergence has lasted longer and is significantly higher than the other two periods of divergence since the early 2000s.

P/E ratios, especially for the U.S., but also for Europe (at least until 2022) have been drifting higher.

There are several reasons for this that have nothing to do with deglobalization:

- More wealth chasing fewer public investment options

- A higher percentage of tech companies in the U.S. indices

But what if globalization also allowed P/E ratios to rise? That the benefits and efficiencies of globalization helped investors get comfortable paying more for stocks? That companies being able to optimize their businesses globally supported higher P/E ratios?

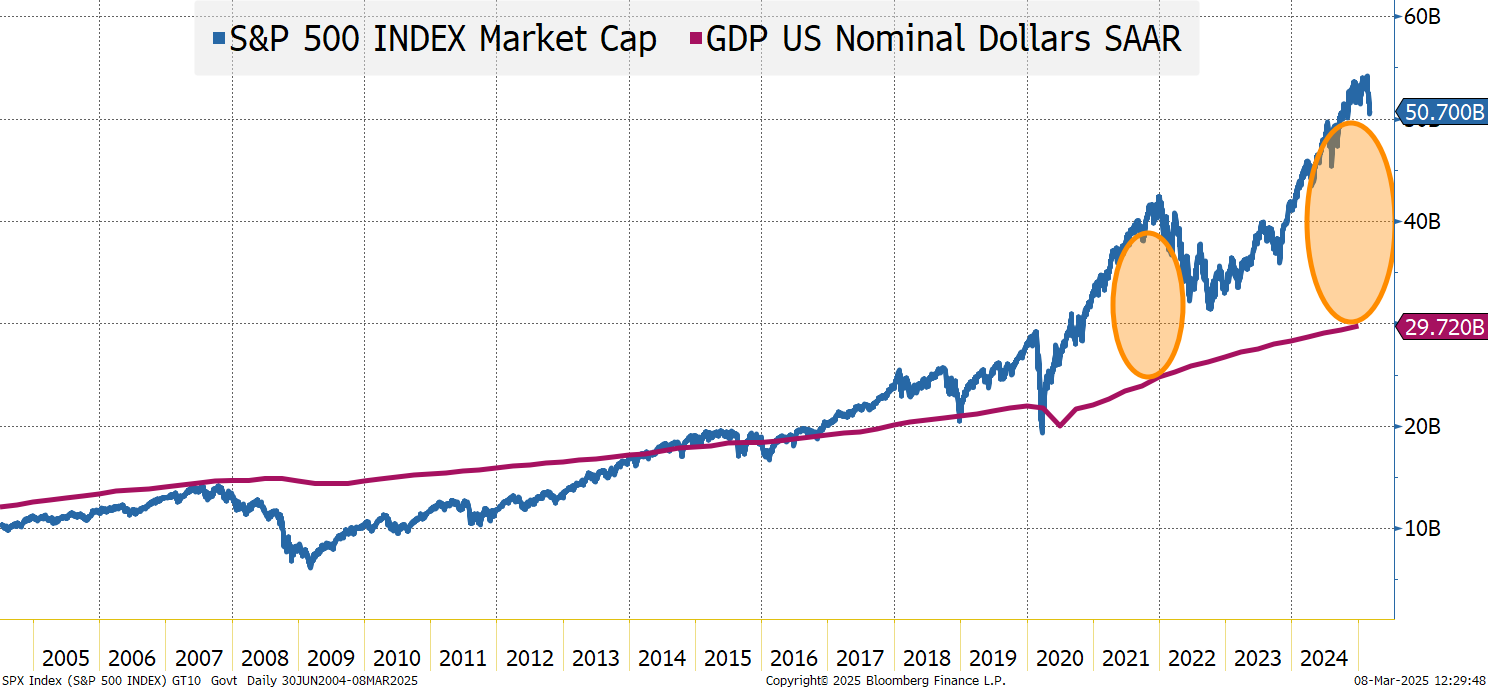

I never really think in terms of U.S. equity market caps and U.S .GDP (though I think Warren Buffett does).

I’ve largely dismissed any comparison between U.S. GDP and the S&P 500 market cap because — you guessed it — about one-third of revenue comes from overseas!

Comparing global equity market cap to global GDP makes more sense, but nothing I spend much time thinking about, until recently.

I think it is more difficult to argue that globalization hasn’t played a role in this divergence! Again, lots of other factors at work, but how much of that orange oval, is linked to the benefits of globalization that may be getting disrupted?

Bottom Line

I’m not “buying the dip,” at least not in a meaningful way.

I think the Nasdaq 100 will trade lower than where it closed Friday. I’m not quite as bearish as a week ago, as we’ve had a significant move to the downside, but I’m selling bounces and keeping my longs controlled (predominantly in Chinese ETFs, and sectors that should benefit from production and refining in the U.S.).

I’m cautious on credit products (IG and HY) as they are starting to leak wider and that will accelerate as the recession risk fears grow.

I’m more or less neutral on rates. The economy is pulling yields lower. The deficit, keeps them from getting too low, and I think there is a risk we see a “foreign buyers strike” which would push them higher.

I could be wrong, and these could be “normal” times, but that is not how I’m trading this market. I’m trading it that we can lurch from headline to headline, but will sell any headline that isn’t connected to actual action!

At the time of publication, Tchir was short QQQ and long FXI and KWEB.