More Than Citrini, Beyond Cybersecurity and What to Do Now

After a destructive Monday, let's examine the '2028 Global Intelligence Crisis', Anthropic's 'Claude Code' and the danger that still lurks.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Good morning. That was ugly.

If one was out shoveling snow on Monday or somehow never made it to work and that someone just looked at those numbers at the day's end... that someone was lucky. That person probably escaped feeling just how destructive Monday was in terms of risk asset performance.

The financial media spent most of the day blaming the ongoing circus around President Trump's attempts to preserve his tariffs and that certainly was a negative catalyst. That, however, was just the knockdown pitch.

The "Ugly Stick" was out and about on Monday. Everything that stick touched was hurt and that stick was driven by fears centered on what generative and agentic artificial intelligence will do to the economy. What AI will do to labor markets. What AI will eventually do to the U.S. and global consumer. Ugly.

'The 2028 Global Intelligence Crisis'

Citrini Research released a memo over the weekend that made the rounds on Wall Street throughout the day on Monday. The memo discusses the impacts of artificial intelligence from 2026 through June 2028. Basically, it discusses fears that we have discussed here for quite some time but imagines a specific timeline instead of just theorizing.

In a social media post, Citrini Research wrote, "It's a scenario, not a prediction like most of our work. But it was rigorously constructed, dismissing it outright requires the kind of intellectual laziness that tends to get expensive." The piece illustrates how the ongoing adoption of artificial intelligence could possibly trigger much higher levels of unemployment and negatively impact companies that cater to the consumer-driven economy as well as those consumers themselves.

The memo adds that when cracks did appear in that consumer-driven economy, the term "Ghost GDP" became popularized, as a means towards describing output or economic activity that shows up in national accounts but never circulates on Main Street. We have referred to that condition here as non-labor market reliant GDP. No... this is not good, and it has the potential for an "ugly" reality. We talk about the "ugly stick" touching stocks on down days for the markets. What about when the ugly stick touches entire industries? Entire regions? Entire populations?

Citrini's piece goes on to mention that the beatdown that we have witnessed across "software as a service" was just the beginning. The same logic that helped certain types of firms reduce payrolls eventually applies to every single company across the economy with a "white collar"-focused cost structure.

More Than Citrini

The overt pressure placed upon the more productive parts of our marketplace on Monday did not all come from Citrini Research or even from President Trump's tariffs. Once again, a tech start-up (is it really still a start-up?) by the name of Anthropic was behind a large part of the equity market bloodshed.

The Monday selloff that appeared to center on cybersecurity stocks actually began on Friday (in an "up" market) after Anthropic announced "Claude Code," which is an AI-powered assistant designed to scan data bases for security vulnerabilities and then suggest corrections or "patches" for human review. Industry leader CrowdStrike Holdings (CRWD) gave up 8% on Friday.

I had to sell some, though I did not want to, ahead of earnings, but at that point it was self-defense. Good thing. The stock was down another 9.9% on Monday. I do still have some in inventory. Earnings are due next week. Palo Alto Networks (PANW) , Zscaler (ZS) , and Fortinet (FTNT) , all felt the pain.

In defense of legacy cybersecurity as a service, CrowdStrike CEO George Kurz posted to social media that he prompted "Claude" to build a tool that could replace CrowdStrike. According to Kurz, Claude responded, "I appreciate the ambition, George, but I have to be straightforward: building a replacement for CrowdStrike isn't something I can do here, and it wouldn't be responsible for me to suggest otherwise." So, investors have that.

Beyond Cybersecurity

Anyone else notice that IBM (IBM) was down 13.2% on Monday or that MongoDB (MDB) was off 11.4%? Anthropic, yes that same Anthropic, announced on Monday that this same "Claude Code" could be used to automate the exploration and analytical work that drives most of the complexity in COBOL modernization.

For those unaware, COBOL is the programming language that had been designed decades ago for high-volume, batch processing business data and still powers roughly 90% of top U.S. companies, specifically in finance as well as in government. Is this the end of the IBM mainframe? How about the end of traditional banking and some of its ability to generate fees? 95% of ATM machines rely on this technology.

While the Dow Jones U.S. Software Index, which includes cybersecurity, gave up 3.93% on Monday, the Dow Jones U.S. Bank Index was stung for a loss of 4.26%. The KBW Bank Index surrendered 4.4%. None of the large money centers were spared. Citigroup (C) , JPMorgan Chase (JPM) , Wells Fargo (WFC) , and Bank of America (BAC) were tagged for losses of 4.5%, 4.2%, 4% and 3.8%, respectively.

The Fall of the House of Usher

I rushed from the room; I rushed from the house. I ran. The storm was around me in all its strength as I crossed the bridge. Suddenly a wild light moved along the ground at my feet, and I turned to see where it could have come from, for only the great house and its dark ness were behind me. The light was that of the full moon, of a blood red moon, which was now shining through that break in the front wall, that crack which I thought I had seen when I first saw the palace. Then only a little crack, it now widened as I watched. A strong wind came rushing over me — the whole face of the moon appeared. I saw the great walls falling apart. There was a long and stormy shouting sound — and the deep black lake closed darkly over all that remained of the House of Usher.

- Edgar Allen Poe (the final paragraph), 1839

Marketplace

For those readers who also manage (or have someone else manage) semi-large to large bond trading accounts, at least there were sizable gains made across that market on Friday. That likely kept you afloat.

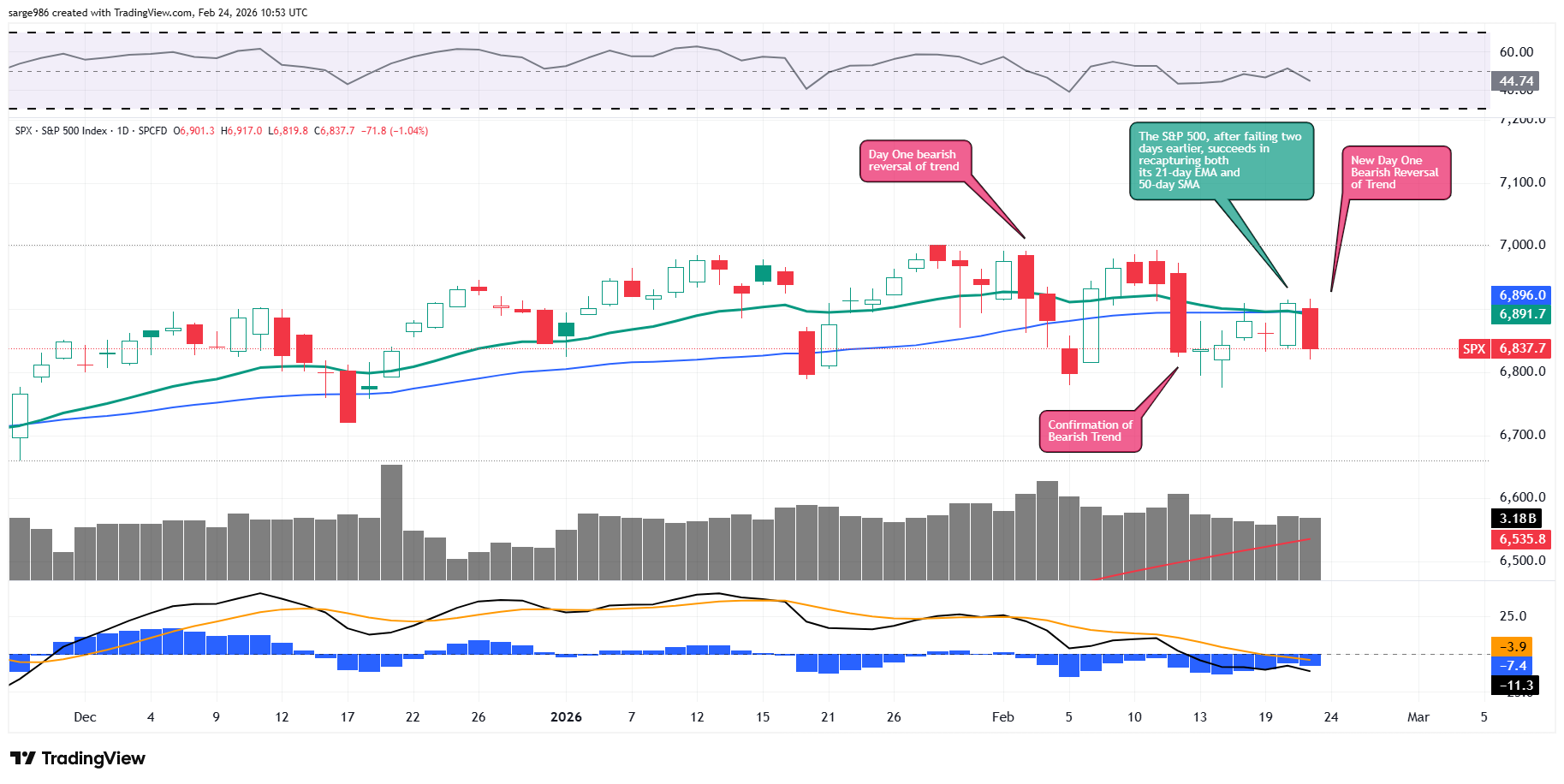

The U.S. Ten-Year Note pays just 4.04% Tuesday morning, nearly dropping all the way to 4.02% overnight. For equity markets, Monday was nasty. The S&P 500 gave up 1.04%, while the Nasdaq Composite gave back 1.13%. Both are now negative for the year 2026 to date.

The small-to mid-cap indexes all underperformed the broader marketplace. That means that they got slapped around pretty good. The Dow Transports were simply pummeled.

Interestingly, five of the 11 S&P sector SPDR ETFs managed to close out the day in the green. Unfortunately, the top-three performers among those funds and four of the top five were defensive in nature, led by the Staples (XLP) and Health Care (XLV) . The cyclical and growth type sectors were roasted.

Danger!

Losers beat winners by nearly a 3 to 1 margin at the NYSE and by about 9 to 4 at the Nasdaq. Advancing volume took just a 29.4% share of composite NYSE-listed trade and a 42.3% share of composite Nasdaq-listed trade.

It gets worse.

On a day-over-day basis, aggregate trade expanded by 3.8% across NYSE listings and by 2.5% across Nasdaq listings. Activity also picked up across the membership of the S&P 500. You all know what that means...

After four green-candle sessions in five and for the S&P 500, the actual retaking of both the 21-day exponential moving average and 50-day simple moving average on Friday, Monday presents as a brand new "Day One" bearish reversal of trend, or if you will, a re-conformation of the bearish trend in place since very early February.

The only bright spot might be that the index has not yet lost contact with its all-important 50-day SMA, but it would take a significant rally to retake that thin blue line from here. Moving on to the indicators, Relative Strength is back below the neutral bound and the daily MACD (moving average convergence divergence) is sporting a bearish posture across all three of its components.

What to %$&#ing Do Now?

Stay skinny, gang. It's okay to react late to a bottoming. It's not okay to stay heavy and broad and take on exponentially large losses because you hoped that there would be a quick turnaround or you stuck your head in the sand. If one is not diversified across asset classes, that would be a mistake.

As equities and debt securities appear to be battling for the same capital at the moment, it makes sense for those not exposed to the bond market, to get exposed. I would think one would need exposure to both short and long duration for safety and potential capital appreciation.

As for alternative investments, silver may or may not have had its day, but gold appears to still have room to the upside, at least in dollar terms. Bitcoin and cryptocurrencies are, for now, nothing more than a wasteland of bag-holders. It is more than okay to miss that bottom and chase once that market turns, if it turns.

Turning to equities... Every trade for a reason. Reduce the breadth of one's exposure. Target prices on everything. Panic points on everything. This is not our first rodeo. We know how to traverse difficult times.

Be disciplined in all that you do. There is no excuse for failing to live by your code, both in life and in how you support those you love. Make your standards high. Aspire to be that shining beacon of ethical purity that you were meant to be, both at home and at work.

Always ask yourself, if my (mother, father, son, daughter, etc.) could see me now, would they be embarrassed? Helps in all situations. Now, get out there and fight like you mean it.

Sarge out.

Economics (All Times Eastern)

08:15 - ADP Employment Change (weekly): Last +10.25K.

08:55 - Redbook (Weekly): Last 7.2% y/y.

09:00 - Case-Shiller HPI (Dec): Expecting 1.4% y/y, Last 1.4% y/y.

09:00 - FHFA HPI (Dec): Expecting 0.3% m/m, Last 0.6% m/m.

10:00 - CB Consumer Confidence (Feb): Expecting 86.8, Last 84.5.

10:00 - Richmond Fed Manufacturing Index (Feb): Expecting -4, Last -6.

10:00 - Wholesale Inventories (Dec): Expecting 0.2% m/m, Last 0.2% m/m.

16:30 - API Oil Inventories (Weekly): Last -609K.

The Fed (All Times Eastern)

08:00 - Speaker: Chicago Fed Pres. Austan Goolsbee.

09:00 - Speaker: Atlanta Fed Pres. Raphael Bostic.

09:00 - Speaker: Boston Fed Pres. Susan Collins.

09:15 - Speaker: Reserve Board Gov. Christopher Waller.

09:30 - Speaker: Reserve Board Gov. Lisa Cook.

15:15 - Speaker: Richmond Fed Pres. Tom Barkin.

15:15 - Speaker: Boston Fed Pres. Susan Collins.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: (HD) (2.53), (PLNT) (.79)

After the Close: (HPQ) (.77), (MATX) (3.69), (WDAY) (2.32)

At the time of publication, Guilfoyle was long CRWD, JPM equity.