Markets Make U-Turn, Oil Cools, President Signals Success in War

But here's why the instant rally on Monday doesn't have me calling a 'day one' bullish reversal of trend in real time.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Market_Recon_TSP1_KL

Market_Recon_TSP1_KL

In Spite of War

The clouds are romping with the sea,

And flashing waves call back to me

That naught is real but what is fair,

That everywhere and everywhere

A glory liveth through despair.

Though guns may roar and cannon boom,

Roses are born and gardens bloom;

My spirit still may light its flame

At that same torch whence poppies came.

Where morning's altar whitely burns

Lilies may lift their silver urns

In spite of war, in spite of shame.

- Angela Morgan, 1918

Just Like That...

Equities roared. Treasury debt securities popped. Crude oil sold off quite sharply. It was a reversal for the ages. All because there was some hope. Hope for a quick resolution to the hostilities in the Middle East. On Monday, U.S. Pres. Donald Trump told a reporter at CBS News that the war with Iran was "very complete, pretty much," The president stressed that Iran no longer has a navy or an air force, nor is able to communicate.

The president added "We're achieving major strides toward completing our military objective" and said that the war will be over "very soon." This occurred despite the fact that for the second time since the start of this war, Iran unsuccessfully tried to attack Turkey with a ballistic missile, which was intercepted. Turkey is the only traditionally Islamic nation that is also a member of NATO.

Separately, Pres. Trump mentioned that the U.S. would be waiving oil-related sanctions on certain nations in an effort to ease elevated prices for crude. While not naming those nations, the president said, "So, in some countries, we're going to take those sanctions off until this straightens out."

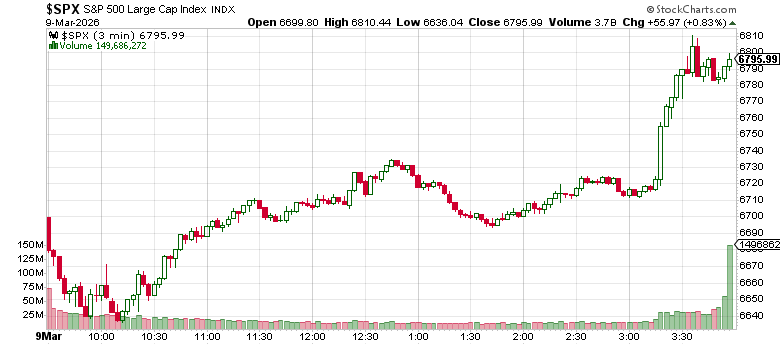

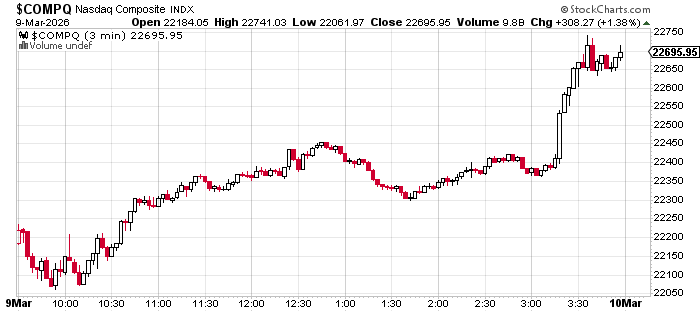

One can see that the S&P 500 reacted to the president's comments about 40 minutes ahead of the closing bell in New York. The one-day chart for the Nasdaq Composite, where the rally was slightly more pronounced, looks much the same.

What about Oil?

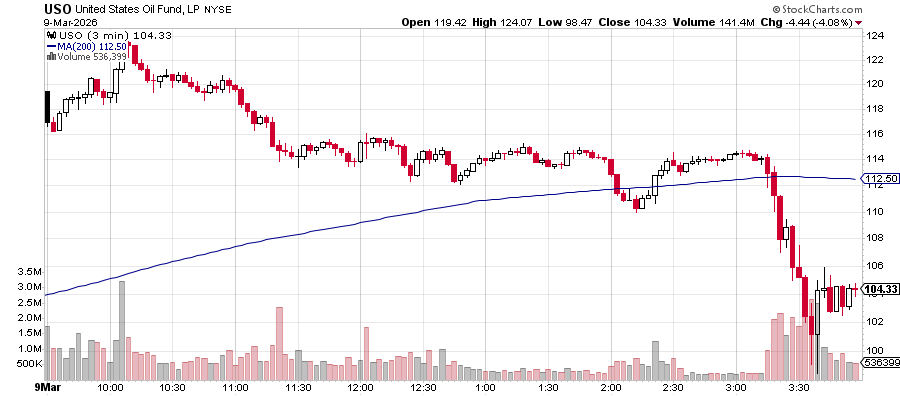

Crude oil obviously moved in the other direction. Ahead of the U.S. open, WTI Crude briefly hit a high of $119.48 before cooling off after G-7 leaders announced that they may discuss releasing strategic reserves in order to ease prices. That was up more than 30% from Friday's closing price of $90.90 for the sweet stuff. Here is a glimpse of how the United States Oil Fund (USO) behaved as the president's words made the rounds:

I see WTI Crude trading with an $87 handle through the zero-dark hours on Tuesday morning, down more than 27% from the Monday high, but off of the overnight lows.

Related: From Market Disaster to Relief in 24 Hours: What Changed and What Hasn't

We All Have...

That one person that makes every single day better in an instant. On Monday, so did the financial markets.

Marketplace

One has to remember that markets were negative and then rallied ferociously. Hence, the data concerning breadth and the size of the day's gains might not be as impressive (though they are impressive) as some might think. This was truly an incredible day for the financial markets. The S&P 500 gained 0.83% for the regular session on Monday, while the Nasdaq Composite surged 1.38%.

The small to mid-cap indexes all closed in the green as well, as did the Dow Transports. The KBW Banks were the only mid-major equity index on my radar to close in the red, down 0.31%, but the Philadelphia Semiconductor Index absolutely roared. That index gained 3.93% for the day, led by SanDisk (SNDK) , KLA Corp (KLAC) and Lam Research (LRCX) .

Breadth

Nine of the 11 S&P Sector SPDR exchange-traded funds closed out the day in the win column, easily led by technology (XLK) thanks to the semiconductors. Health care (XLV) also had a nice day. Financials (XLF) and of course, energy (XLE) were the only losers. For those who may care, because we did get one email asking, our Exxon Mobil (XOM) short is a little better than 1% in our favor at the moment.

Losers beat winners by a five-to-four margin at the NYSE, while winners beat losers by a similar margin at the Nasdaq. Advancing volume took a 57.8% share of composite NYSE-listed trade and a commanding 71.5% share of composite Nasdaq-listed trade. Trading volume increased over Friday's levels. On a day-over-day basis, aggregate trade was up a whopping 15.8% for NYSE-listings and up 5.3% for Nasdaq-listings. Trade increased across the membership of the S&P 500 as well.

A 'Day One' Reversal?

Was Monday a "day one" bullish reversal of trend? Actually, I regret informing excited traders that it was not. Why? The major indexes were higher on increased trading volume. True. There was a major reversal that may have been quite meaningful. Understood. Also, true. Losers outnumbering winners at the NYSE prevents me from calling Monday a true "day one" with any certainty.

If we see a "pause day" and a day of confirmation, I still may back date a "day one" to Monday, but in real time, it is difficult to make this call.

One thing does stand out to me though. Check this out:

The S&P 500 experienced an "outside day" on Monday. An outside day, as readers may recall, is a one-day pattern where the activity for a given session completely envelops the activity for the day prior. This signals increased volatility for the coming sessions more than it does direction. Readers will note the outside day of March 2nd and what came after.

Readers also need to be fully cognizant that the S&P 500 barely snuck back above the line of support for the basing period that had been in place for most of 2026. The index still has to make contact with its 21-day exponential moving average and ultimately its 50-day simple moving average to try and accomplish anything serious technically. That is where the confrontation between bulls and bears will occur. Until then, this is just trading, not investing.

Note to Readers...

I have to get an MRI on my knee this morning. Ticked off a bunch of falcons on one of my wilderness excursions. I was able to keep the birds away from my head, but I twisted my knee defending myself and something cracked. I will not very likely be writing a second piece this morning but will make an effort to keep my third piece (which would be today's second) on schedule.

Economics

(All Times Eastern)

06:00 - NFIB Small Biz Optimism Index (Dec): Expecting 99.7, Last 99.3.

08:15 - ADP Employment Change (weekly): Last 12.75K.

08:55 - Redbook (Weekly): Last 7.0% y/y.

10:00 - Existing Home Sales (Feb): Expecting 3.9M, Last 3.91M SAAR.

4:30 p.m. - API Oil Inventories (Weekly): Last +5.6M.

The Fed

(All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: (KSS) (.84)

After the Close: (AVAV) (.69), (ORCL) (1.70)

At the time of publication, Guilfoyle was short XOM equity.