Market Tripwire, 'The Pea', Rare Earths, China's Ace Card?, The Week Ahead

You can always be surprised. Headline risk will matter just as much as anything else now, even corporate earnings and guidance.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Have you seen a pea roll off of a table? I mean lately. If you happen to work in, or trade our financial markets for a living, then you have. As recently as Friday.

It had been for some time now that value investors had been concerned about equity valuations. It had been for some time now, though I had not, that many market technicians focusing on indicators not among my favorites had viewed U.S. equities as being broadly overbought.

I had acknowledged that the indicators that I most often use showed a market quite strong, but not quite technically overbought. Regardless, it became clear on Friday that professional money was indeed "scared" money, and in their collective fear, there was a willingness to quickly turn assets into cash.

All that was needed was a catalyst. A catalyst was exactly what "they" got.

Tripwire

Forty-something years ago. Camp Lejeune. Training. It was pitch black. I was on point. Completely blinded by the lack of moonlight, I was inching my way through the woods. I knew the trail that I was trying to stay parallel to was booby-trapped. I also knew that the woods around the trail were booby-trapped to try to catch guys like me who would make an attempt to bushwhack their way around being detected.

Crawling on my belly, groping in the darkness, I felt something akin to a fishing line to my immediate front. Signaling with a double flash of red light under my cupped hand (this is before night-vision and before headsets) to my team to follow... up and over I went. That's not so bad. Again. Then, again. Every eight feet or so. One more time, up and... boom! Two lines had been about 12 inches apart. I came down with my combat boot on the second tripwire. The triggered booby trap sent up a flare. (In training, booby traps don't blow you up, they expose you.) My entire team was "pretend" wiped out by machine gun fire (blanks). Lessons learned. You're never as good as you think you are. You can always be surprised.

What finally triggered a significant market selloff on Friday was President Trump's reaction to the news on Thursday that Beijing was going to tighten its export rules for rare-earth minerals and metals. China has of late, acted as if they could take U.S. technology or leave it. That advantage in the technology space is or was an ace card for the U.S. The Chinese ace card has been that the U.S does not at present have the ability to refine rare earths at scale.

Calculated move by China? Perhaps. Only if they are so confident in their domestically designed AI-capable chips and AI-capable software as to not need the U.S.

Foolish move by China? Perhaps. Especially if Beijing is playing "chicken" with the tech/rare-earth trade-off that balances the relationship between the world's two largest economies. Especially if China puts itself at risk of losing the U.S. market. The U.S. has more than one ace card and may just have the ultimate ace card.

That said, the introduction of uncertainty to the relationship between the U.S. and mainland China just a couple of weeks ahead of a planned meeting between President Trump and his Chinese counterpart, Xi Jinping, was definitely a risky move that has reintroduced volatility to U.S. financial markets. Will the two sides even meet? On Friday, President Trump publicly doubted it.

On Friday, President Trump imposed an additional 100% tariff on Chinese goods imported into the U.S., effective November 1, in addition to existing tariffs. The president also announced that there would be increased restrictions placed upon sales of technology, including critical software to Chinese-based customers.

Hmmm...

The effective tariff rate on Chinese imports is already roughly 40%, according to the economics team at Wells Fargo. Of course, that's an average, and every class of import is different. Tacking on 100% on top of 40% would for all intents and purposes put China out of business while crushing margins for U.S. companies as they scramble to find workarounds.

So, why would China make such an aggressive move going into a crucial meeting with their largest customer who is trying to nail down a trade deal? Leverage? That would be some chance to take, again, unless Beijing is sure that they have an advantage in the above-described balance.

That would mean that Beijing knows that their technology has caught up to or almost caught up to U.S.-based tech design. Then again, the U.S. is not short of rare earths, the U.S. is short of rare-earth mining and refining capabilities for ecological reasons only. Push the U.S. in that direction and need you less than they ever have, they will. That still leaves U.S. consumption unaccounted for. Heard a rumor that they can "make stuff" all over the world, even here at home.

This thing is far from decided.

Then Came Sunday

Sunday afternoon. President Trump posted to his Truth Social account...

"Don’t worry about China, it will all be fine! Highly respected President Xi just had a bad moment. He doesn’t want Depression for his country, and neither do I. The U.S.A. wants to help China, not hurt it!!! President DJT"

Earlier that morning, Vice President JD Vance appeared on the Fox News show "Sunday Morning Futures" with Maria Bartiromo and said, “It’s going to be a delicate dance, and a lot of it is going to depend on how the Chinese respond. If they respond in a highly aggressive manner, I guarantee you, the president of the United States has far more cards than the People’s Republic of China.”

Voila! At 6 p.m. on the East Coast on Sunday night, U.S. equity index futures opened for the Monday session. They immediately shot higher, but not nearly as far as the haircut taken by the markets on Friday.

Can the Sunday night rally hold? Or, have we just entered a new era of undefined length of increased volatility? I think we all know that for now, headline risk will matter just as much as anything else, even corporate earnings and guidance.

Breaking!

It appears that as I finish up this morning note that all 20 surviving Israeli hostages have been released by Hamas to the Israeli military. Another 28 bodies will be handed over later on. Once all survivors and bodies are returned, Israel will release 250 Palestinians from its prisons and as many as 1,700 detainees in Gaza.

A cease-fire is in effect in the region. Israeli Defense Forces have retreated to their pre-designated areas and humanitarian aid is flowing into the area.

The Week That Was

What the mid-major to major U.S. equity indices did last week, as tech sold off and more than a few feathers were ruffled...

- The S&P 500 lost 2.71% on Friday swinging to a loss of 2.43% for the week.

- The Nasdaq Composite gave up 3.56% on Friday, swinging the week to a loss of 2.53%.

- The Nasdaq 100 gave back 3.49% on Friday landing down 2.27% for the week.

- The Russell 2000 surrendered 3.01% on Friday and lost 3.29% for the week.

- The S&P Smallcap 600 gave up 3.18% on Friday and an ugly 4.94% for the week.

- The S&P Midcap 400 lost 2.84% on Friday and 3.86% for the week.

- The Dow Transports were hit for 3.31% on Friday smacked for 4.88% for the week.

- The Philly Semis surrendered a stunning 6.32% on Friday but "just" 2.68% for the week.

- The KBW Bank Index lost 3.45% on Friday and a nasty 5.02% for the week.

On Friday, 10 of the 11 S&P sector SPDR ETFs closed out the session in the red, led lower by Technology (XLK) and Energy (XLE) . The Staples (XLP) were the day's only winner thanks to PepsiCo (PEP) as the four defensive sectors took the top-four slots on the daily performance tables.

For the week, nine of the 11 S&P sector SPDR ETFs traded lower with Energy leading three cyclical sectors to the bottom of the weekly performance tables. Only the Utilities (XLU) and the Staples (surprise, surprise) ended the week in the green.

The Chart...

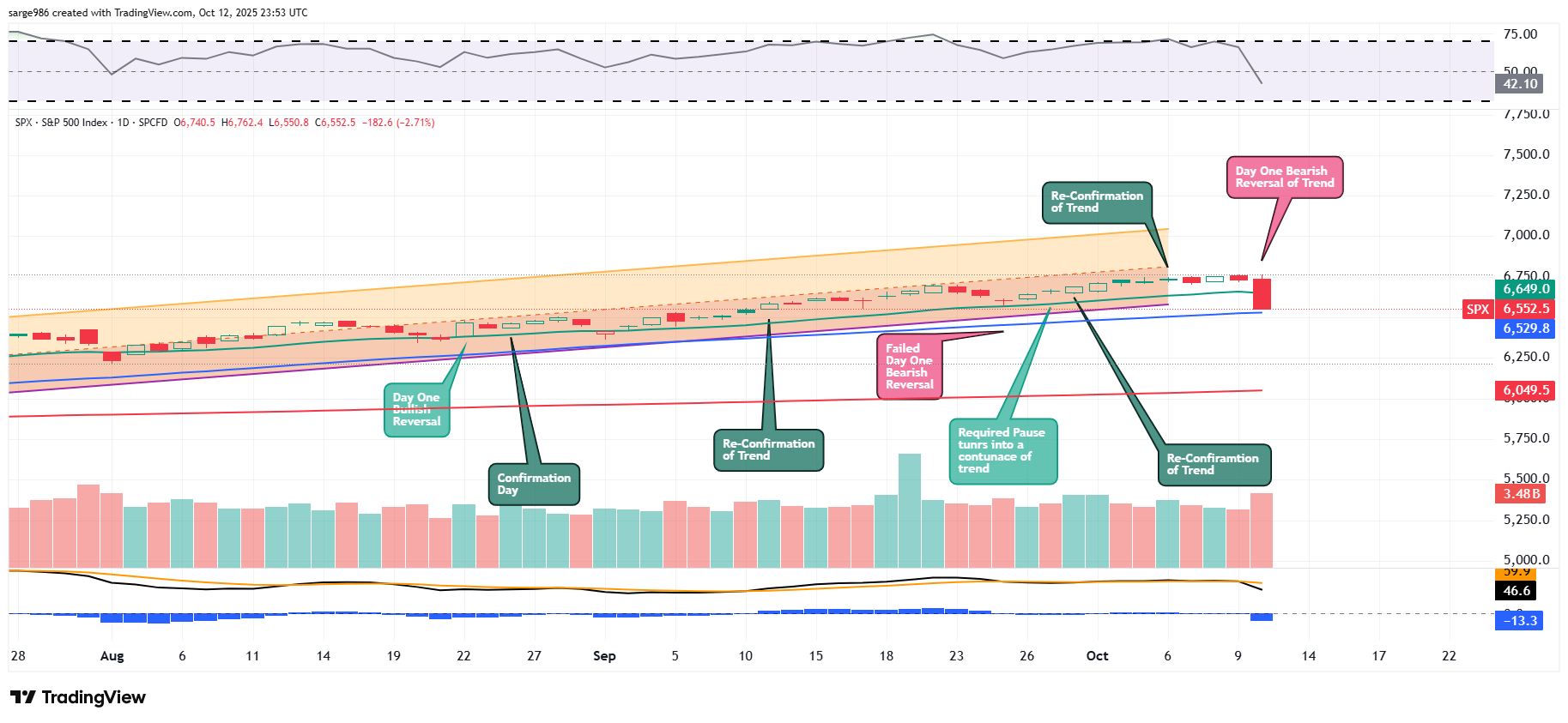

No doubt about it. Our chart has started to get sort of messy.

Readers will see that last week, not only did the S&P 500 close in the red for three of the past four days, but on Friday, the pressure was overwhelmingly to the downside, and it came on a notable increase in trading volume too. Not what the bulls wanted to see.

That Sunday night rally in the futures markets? Unless there are some positive headlines that reverse last week's China-related news, that could simply be the necessary pause in between a day of reversal and a day of confirmation. We'll know more soon enough. Remember, though, that today is a federal holiday. The banks are closed as is the bond market, so trading volume will be artificially light.

Readers will note that on Friday, while relative strength for the S&P 500 crossed into sub-neutral territory, the daily moving average convergence/divergence (MACD) for the index took a fairly severe hit as well. The histogram for the 9-day exponential moving average (EMA) crossed below the zero-bound, while the 12-day EMA crossed below the 26-day EMA. These are short to medium-term bearish signals.

Is there a positive signal? Yes. On Friday, the S&P 500 (and Nasdaq Composite) found support above its 50-day simple moving average (SMA). There could have been an algorithmic bloodbath had that line not held.

Earnings

Today is a holiday, but the third-quarter earnings reporting season will begin in earnest starting tomorrow. According to FactSet, for the third quarter, Wall Street is looking for earnings growth of 8%. Wall Street also expects to see revenue growth of 6.3%. Both of those expectations remain unchanged from where they were last week at this time.

Technology and Utilities are expected to be the outperformers, with projected earning growth of 17% or more. Four sectors are now predicted to suffer a year-over-year earnings contraction led to the downside by Energy. The Health Care sector surprisingly saw consensus for its y/y earnings growth for the quarter fall from +0.1% a week ago to -1.7%.

For the full calendar year of 2025, Wall Street sees S&P 500 earnings growth at 10.9% on revenue growth of 6.1%. This is also in line with last week's expectations.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 22.8 times 12 months' forward-looking earnings, in line with where that metric was a week ago. This still stands well above the five-year average of 19.9 times for the index as well as its 10-year average of 18.6 times. The S&P 500 also ended last week trading at 28.9 times trailing 12 months' earnings, up slightly from 28.8 times a week ago. That also stands well above the five-year (25 times) and 10-year (22.7 times) averages for the index.

Ten of the 11 sectors are now trading above their five-year average valuations, led by Tech (31 times) and Consumer Discretionaries (29 times). Only the REITs (17.5 times), remain undervalued relative to their five-year averages.

The GDP Game

Last week, the Atlanta Fed left their GDPNow model for third-quarter growth unrevised at 3.8% (q/q, SAAR), largely due to a lack of reported macroeconomic data. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth now stands at 2.34%, down slightly from 2.35%. The Cleveland Fed's model for the third quarter also remained unrevised at growth of 1.99%. Lastly, the St. Louis Fed model was revised upwards to a still weak looking 0.42% from last week's 0.18%.

There remains nothing close to a Fed consensus on just how robust economic activity was during the third quarter. It will be interesting, at least to me, to see if these regional Fed districts stop updating their models without a ton of underlying macroeconomic data to rely on. It looks like Atlanta may have already stopped and New York may be close to doing so.

Fed Funds Futures

Fed Funds futures trading in Chicago are now pricing in a 97% probability for a 25-basis point rate cut on October 29 and an 88% likelihood for another 25-basis point cut on December 10th.

Those probabilities are up from 95% and 84% a week ago. At present, there are now 75-basis points worth of additional rate cuts fully priced in (52% chance) for all of calendar 2026. This is up 25-basis points from where this likelihood stood last week at this time.

On The Docket...

For the third week in a row, without a lot of macroeconomic data to look at, the Fed will be out in force, making an obvious attempt to be seen and heard.

-- Today (Monday) is a federal holiday. The banks are closed, but there is still one Fed official on my radar. New Philadelphia Fed Pres. Anna Paulson will speak this afternoon. Tomorrow, Fed Chair Jerome Powell headlines a lineup of public speakers that also includes Fed Governors Michelle Bowman and Christoper Waller., both of whom are front runners to take his job as soon as this May. This Wednesday, Fed Governor Stephen Miran and Waller will both speak as the Fed releases its updated Beige Book ahead of the October 29 policy decision. Thursday will be the last "big" Fed day this week as Miran speaks twice, Waller speaks for a third day in a row and Bowman speaks for the second day in three.

-- As far as the macroeconomic calendar is concerned, don't get your hopes up. Anything released by the Fed or regional agencies will likely still hit the tape. Everything else will likely be delayed.

-- The earnings calendar will finally get hot this week. On Tuesday morning, we'll hear from BlackRock (BLK) , Citigroup (C) , Domino's Pizza (DPZ) , Goldman Sachs (GS) , Johnson & Johnson (JNJ) , JPMorgan Chase (JPM) and Wells Fargo (WFC) . These names will be followed on Wednesday morning by Bank of America (BAC) , Morgan Stanley (MS) and Abbott Labs (ABT) . Thursday morning brings us numbers from Bank of New York Mellon (BK) , KeyCorp (KEY) and M&T Bank (MTB). Lastly, American Express (AXP) and SLB (SLB) will report on Friday. SLB is the old Schlumberger.

-- As far as non-earnings-related corporate events are concerned, Salesforce (CRM) will hold its annual Dreamforce conference in San Francisco this week from Tuesday to Thursday. This is a big deal for Salesforce, which appears to have fallen behind in what it needs to be strong in, agentic AI. The stock closed on Friday down more than 34% from its January peak.

Economics (All Times Eastern)

No significant domestic macroeconomic data-points scheduled for release.

The Fed (All Times Eastern)

12:55 - Speaker: Philadelphia Fed Pres. Anna Paulson.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: (FAST) (.30)

At the time of publication, Guilfoyle was long PEP, JPM, WFC, KEY equity.