Market Rotation Gives Small, Medium Caps a Turn

Let's see how Oracle might be its own problem, chips took it on the chin, Disney shows some 'character' with OpenAI, and AI is still alive and kicking.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Despite a negative market reaction to Oracle (ORCL) earnings on Wednesday afternoon that carried into Thursday, equity markets broadly enjoyed a significant comeback throughout the day. Sure, AI-related stocks showed some weakness, but the marketplace, in general, recovered quite nicely after bottoming shortly after the opening bell.

So, Oracle would go on to surrender a gnarly looking 10.8% on the day. We had warned readers three months earlier that this stock's share price had been built upon a house of cards -- a sloppy looking balance sheet. Did the entire AI-focused trade need to get punished? Maybe not. I'm not going to complain though, especially if that acts as a springboard for the rest of our beloved marketplace.

As James "Rev Shark" DePorre mentioned in his note last night, the Roundhill Magnificent Seven (MAGS) did close out the day in the red, -0.74%, but both blue chips and small caps were strong. Are we headed into a third day of this kind of action going into the weekend? It would not surprise me. After reporting on Thursday evening, Broadcom (AVGO) is trading sharply lower overnight, while Lululemon Athletica (LULU) and RH (RH) are trading higher. Of course, Lulu's surge had a little something to do with a huge repurchase authorization and the departure of a chief executive known more for underperformance than anything else.

Rally Caps

While it is true that the Nasdaq Composite gave up 0.25% on Thursday, depressed by a 0.75% setback for the Philadelphia Semiconductors, the rest of the U.S. equity marketplace did quite well. Before moving on, we'll acknowledge that on Thursday, among the semis, Arm Holdings (ARM) , Marvell Technology (MRVL) and Intel (INTC) all took beatings of greater than 3%.

The pressure on the tech trade kept gains for the S&P 500 subdued. Our broadest large cap equity index gained just 0.21% for the session. Beyond the majors, the Dow Industrials gained 1.34%, led by a 6.1% run by Visa (V) . The small- and mid-cap indexes did well too, with the S&P 400, S&P 600 and Russell 2000 posting gains of 0.98%, 1.13% and 1.21% respectively. Oh, did we mention that the banks did well? On Thursday, the Dow Jones U.S. Bank Index ran 1.55% as the KBW banks popped for 1.16%.

Breadth

Eight of the 11 S&P sector SPDR ETFs closed out the day on Thursday in the green, led by the Materials (XLB) and the Financials (XLF) . Obviously, Technology (XLK) brought up the rear. While cyclical sectors out-performed for the day and that could be seen as a positive for both the market and the economy, the one warning sign taken could be that all four defensive sectors out-performed both growth sectors for the session.

Winners beat losers by better than a two-to-one margin across the NYSE and still beat losers (by a rough five to four) at the Nasdaq. Advancing volume took a commanding 67.7% share of composite NYSE-listed trade and still a majority share (51.5%) of composite Nasdaq-listed activity. The one hiccup? While aggregate trading volume did grow by 4.4% on a day over day basis across Nasdaq-listing, trade was down 9.1% across NYSE-listings where more of the market strength was visible. Aggregate trade also receded across the membership of the S&P 500.

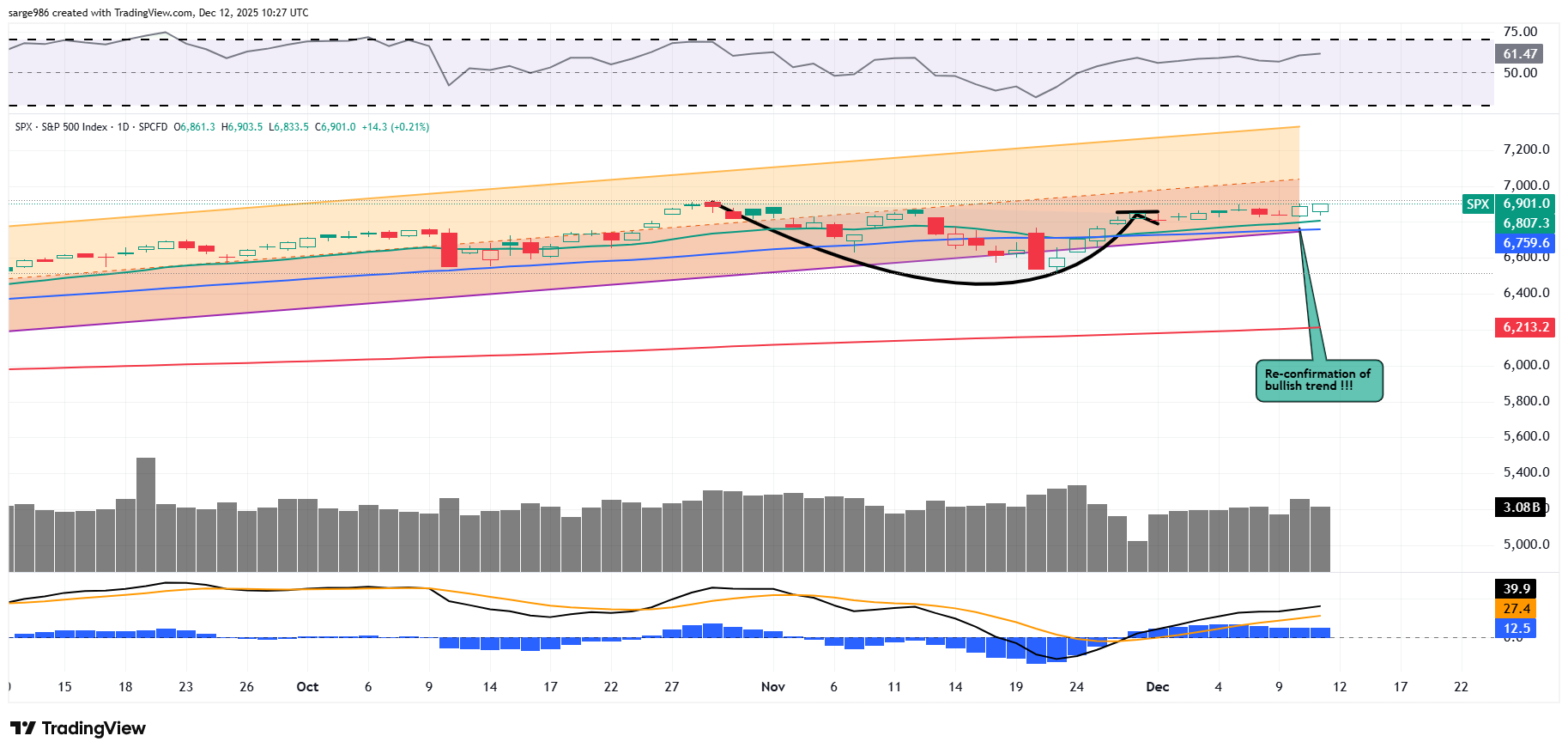

The Chart

As of now, the reconfirmation of the bullish trend by volume that markets experienced on Wednesday stands and was reinforced by the action witnessed on Thursday.

In addition, both the reading for relative strength and especially the daily Moving Average Convergence Divergence remain postured extremely bullishly.

Even as the AI Trade Waffles...

The Walt Disney Company (DIS) announced a $1 billion investment in OpenAI on Thursday, after Disney had sent a "cease-and -desist" letter to Alphabet's (GOOGL) Google, accusing Google of "infringing" on Disney's copyrighted properties "on a massive scale." The letter includes images and screenshots of videos using Disney characters created using Google's Gemini, Nano Banana, and Veo.

OpenAI will pay Disney to use up to 200 Disney characters from across the broad spectrum of Disney franchises in Sora to generate user-prompted short-form videos. On top of the $1 billion investment, Disney will receive warrants to purchase more stock in OpenAI based on its current $500 billion valuation. That does not sound like the death of the AI-focused up-spend to me.

Maybe Oracle's problems, as we told readers in September, are unique to Oracle. If anything, I see the AI-trade broadening to include names that had not previously been associated with that trade.

That might slow down the names that had already prospered from what had been a rather narrow trade. That does not, however, mean that the trade reverses. While it may be a net negative for humankind, in terms of purpose-driven employment, there is simply too much to gain from a corporate perspective in terms of decreased overhead, increased margin and increased productivity to let investment in this trade linger. The AI-trade does not falter. The AI-space becomes more competitive.

Economics

(All Times Eastern)

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 549.

1:00 p.m. - Baker Hughes Oil Rig Count (Weekly): Last 413.

The Fed

(All Times Eastern)

08:30 - Speaker: Philadelphia Fed Pres. Anna Paulson.

08:30 - Speaker: Cleveland Fed Pres. Beth Hammack.

10:35 - Speaker: Chicago Fed Pres. Austan Goolsbee.

Today's Earnings Highlights

(Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long INTC equity.