Market Marches Higher

Let's set our scopes on the relief rally and see why military-related stocks have mud on their faces right now -- and why my fave might get out of ... 'DOGE' ... unscathed.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

They moved into position quietly. Low crawl. Slow crawl. Foliage in socks, socks over boots, no discernible tracks to follow. Covered in mud and slime to disguise the scent that all humans trail. They watched from the perimeter. Alert. Silent. Weapons off safe. Barely a muscle moving. Regulated breath. So ... slow. Eyes alive. Fix bayonets.

The momentum built. Financial markets had started the Thursday session close to where they went out on Wednesday. There was a scent of caution in the air. The January consumer price index, released on Wednesday morning, had landed like a band aid ripped off of a hairy patch of skin. The produce price index, released Thursday morning, had been hot as well, but less hot. Markets were waiting upon the President of the United States. Word was that "reciprocal" tariffs were about to be implemented via executive order. Word was wrong.

The president surprised the marketplace by signing not an executive order announcing the launch of those reciprocal tariffs, but a memo directing both the Commerce Department and the U.S. Trade Representative to outline steps that would be taken for the U.S. to adjust tariffs on imports to proportionally match those tariffs and barriers to trade already in place on U.S. exports to individual nations.

The memo is meant to begin the process of ensuring fairness for U.S. businesses in cross-border commerce by adjusting for all factors (not just tariffs, specifically) that disadvantage American businesses. The reason for the positive surge across U.S. financial markets was the fact that nothing was implemented immediately, as had been anticipated. It could take the U.S. Trade Representative and the Department of Commerce as much as six weeks (maybe more) to come back to the president with something concrete.

Adding fuel to the markets' fire, after the Senate had passed a resolution that would lift the federal debt limit, House Republicans unveiled their own plan that would both extend the Trump tax cuts, while also increasing the debt ceiling. It doesn't hurt that the peace process appears to be gaining momentum in both Israel and eastern Europe, either.

Thursday!

The strength was not just in equities on Thursday, though the major U.S. equity indexes rallied throughout the day and closed at their highs. As the U.S. Dollar Index relaxed a bit in response to the delayed tariffs and the potentially higher debt ceiling, gold and silver rallied. Bitcoin remains in a technical state of consolidation and continues its sideways move. U.S. Treasuries were hot on Thursday as the yield for the Ten-Year Note dropped 10-basis points to 4.53%, as the U.S. Two Year Note paid 4.32% (-4 bps) by day's end.

As for stocks, the Thursday regular session was especially strong. The Nasdaq Composite gained 1.5% as the S&P 500 ramped up 1.04%. Small- to mid-cap stocks kept up for a nice change as well. The Russell 2000, S&P 600 and S&P 400 gained 1.17%, 1.45% and 0.92% respectively. The wealth was spread across sector groups as well.

All 11 S&P sector SPDR ETFs gained ground on Thursday with five of them up more than 1% for the day. Materials XLB and Discretionaries XLY led the northerly trek, as Utilities XLU and Industrials XLI lagged. Cyclical and growthy type sectors outperform defensive sectors for the session. As it is important to note that the weaker dollar helped the Materials stocks, the Industrials were held back by a sell-off across aerospace and defense stocks.

Breadth

Winners beat losers at the NYSE by greater than 7 to 2 and at the Nasdaq by more than 5 to 2. Advancing volume took a commanding share of composite trade for names listed at both exchanges (76.2% at the Nasdaq, 73.7% at the NYSE). In addition, aggregate trade increased on a day over day basis, across the listings of the NYSE, the listings of the Nasdaq and the membership of the S&P 500. Thursday counts as a technical confirmation of a continuance of an already confirmed upward trend for the major indexes.

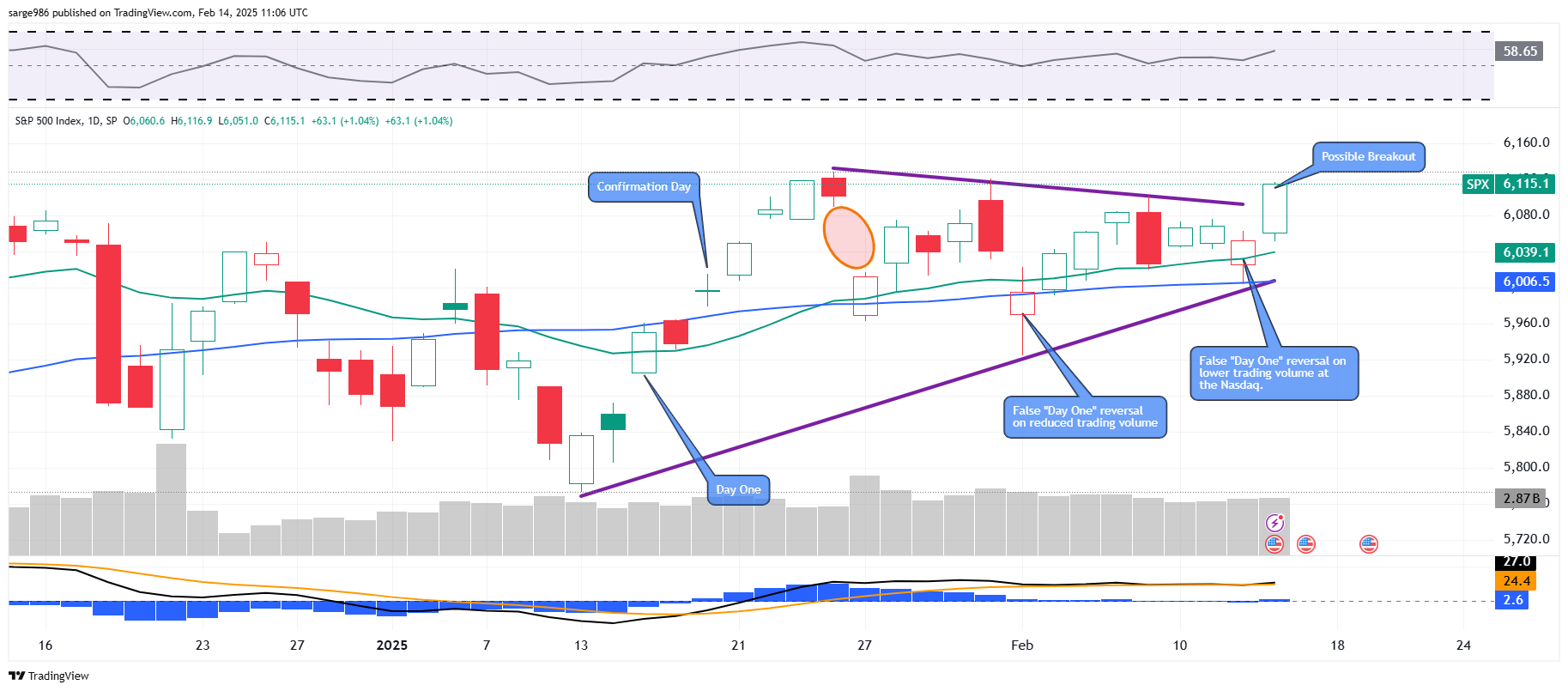

Readers will note that on Thursday, the S&P 500 poked its head above the line of resistance in place as the series of lower highs that had been running for about a month, came to an end. The S&P 500 found support precisely at its 50-day simple moving average during Wednesday's sell-off, which may have been key.

Relative strength has now moved higher from the neutral reading where it has been throughout the development of the pennant formation that may have cracked to the upside on Thursday. Within the daily Moving Average Convergence Divergence, the relationship of the 12-day exponential moving average to the 26-day exponential moving average remains indistinguishable, but the histogram of the 9-day EMA has moved back above the zero bond, which would be seen as a bullish development.

About Those Defense Stocks...

Not like we did not warn about this coming. On Thursday, President Trump made clear that as he and his DOGE team look under every rock in their attempt to find waste, abuse and fraud in government spending that defense spending is going to be a focus. You kids know this space has at times been my domain and for many years, my reputation for trading the space had done me well. Things have changed. This administration is serious about finding savings and improving the nation's fiscal imbalance.

I don't think it's any secret that budget overruns and stupid prices for many items have long been a hallmark of defense spending in this country. The president said on Thursday, "One of the first meetings I want to have is with President Xi of China and President Putin of Russia. I want to say, let's cut our military budget in half."

That's what did defense stocks in on Thursday, but the whole group has been trending lower since it became quite obvious last autumn that the U.S. election in November was going to take both executive and legislative power away from the left.

My quick thoughts on the matter? Lockheed Martin LMT, purveyor of a number of very high-ticket items such as the F-35 fighter aircraft, is going to have issues. Readers know that I have been reducing that long position, I sold more yesterday. I have also reduced my long position General Dynamics GD. GD sells nuclear powered submarines, guided missile destroyers, and main battle tanks.

I have not reduced Northrop Grumman NOC of late, nor RTX RTX. RTX is simply great at everything they do and I believe that NOC has a leg up in the development of hypersonic weapons, which I would expect will be exempt from spending cuts. Kratos KTOS is a curious case of course. I may cut this at some point, but I do believe that the recent announcement that the firm is knee-deep in the hypersonic weapons program as a supplier might work out well for this name. Of course, Palantir Technology PLTR provides invaluable intelligence, analytical and AI services to the U.S. military and her allies. I do not think funds spent on what Palantir does will be found wasteful.

Short-Term Trading

On Thursday afternoon, I covered my long position in Tesla TSLA and my short position in AppLovin APP, both laid out in Wednesday and Thursday morning pieces here at TheStreet Pro. Both were very successful rental trades producing gains of 5.3% and 8.5% respectively.

Economics (All Times Eastern)

08:30 - Retail Sales (Jan): Expecting 0.0% m/m, Last 0.4% m/m.

08:30 - Core Retail Sales (Jan): Expecting 0.3% m/m, Last 0.4% m/m.

08:30 - Export Prices (Jan): Expecting 0.3% m/m, Last 0.3% m/m.

08:30 - Import Prices (Jan): Expecting 0.5% m/m, Last 0.1% m/m.

09:15 - Industrial Production (Jan): Expecting 0.3% m/m, Last 0.9% m/m.

09:15 - Capacity Utilization (Jan): Expecting 77.7%, Last 77.6%.

10:00 - Business Inventories (Dec): Expecting 0.1% m/m, Last 0.1% m/m.

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 586.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 480.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ESNT (1.65), MRNA (-2.70)

At the time of publication, Guilfoyle was long LMT, GD, NOC, RTX, PLTR equity.