Market Checkup: Assessing the Santa Rally, January Barometer, and ISM New Orders

Also, let's chart the S&P 500 and Nasdaq, large-cap action, and check on CES and its likely star, Nvidia.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

You can almost feel the excitement build. Equity markets roared on Friday after suffering a year-end losing streak. That came one day ahead of Consumer Electronics Show 2025 in Las Vegas. The CES runs through this Friday, but the main event may be the keynote address delivered by Nvidia NVDA CEO Jensen Huang. Other daily keynotes will be delivered by leadership representing Delta Air Lines DAL, Volvo, the Waymo division of Alphabet GOOGL and X, the privately owned social media company formerly known as Twitter. X is owned and operated by Tesla TSLA CEO and President Elect Donald Trump-ally Elon Musk.

Some say that Santa never showed up on Wall Street this year. While it's true that the S&P 500 gave up 0.5% over the course of the traditional Santa Claus rally period, that same S&P 500 gained 23% for 2024, while the Nasdaq Composite ran 30% for the year. This was the second-straight year that there was no Santa rally and a second straight year that large cap stocks broadly ran more than 20%. That my friends, is a trade-off that I will make every single time. Even if it kills the legend of the Santa Claus rally.

More importantly than the Santa Claus rally, both the First Five Days Indicator and the January Barometer are still in play. Friday's rally, which was enhanced by the first ballot re-election of Louisiana Rep. Mike Johnson as Speaker of the House and the positive print for New Orders within the November release for the ISM Manufacturing Report. Never mind that manufacturing-based employment continued to shrink in November, if new orders keep growing, that alone will carry the entire sector.

Check This Out...

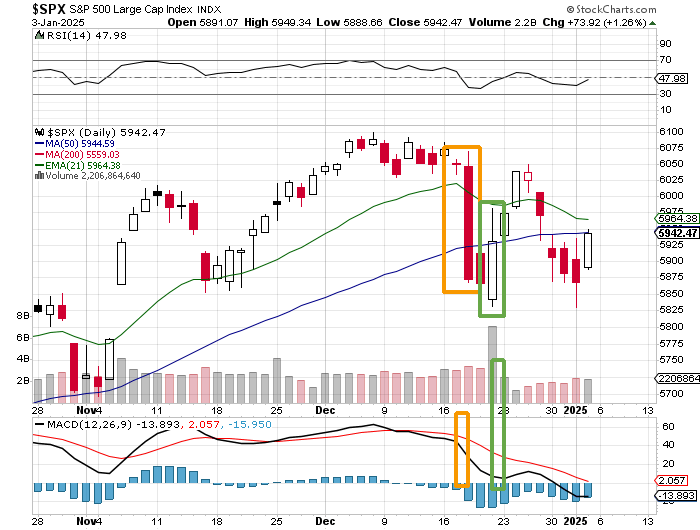

So, we see that the Dec. 20 low for the S&P 500 was taken out on Jan. 2. That technically ended the "up" trend that traders had tried to play going into the above-mentioned Santa rally. Now, the question becomes: Did Friday create a new Day One in search of an upside confirmation? While certainly better than a sharp stick in the eye, not really, or not yet.

While aggregate trading volume was fractionally higher across the S&P 500 on Friday from Thursday, it was not convincing. Take a look below...

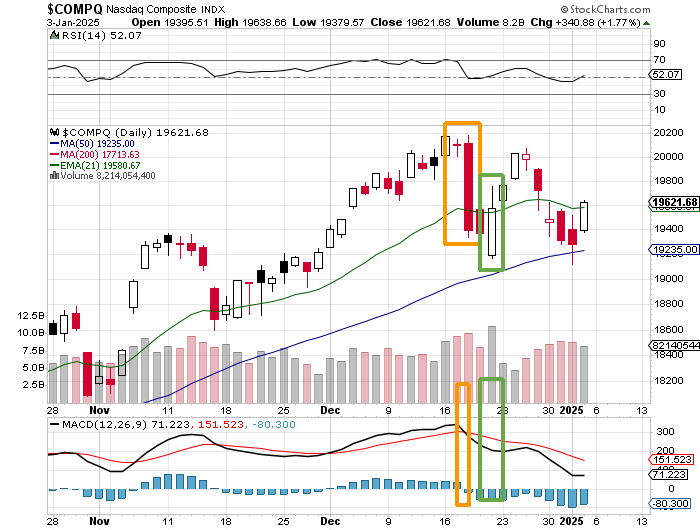

Across the Nasdaq Composite, it is clearer that the pop in aggregate trade required to declare a "Day One" just is not there. That does not mean that stocks cannot rally from here, we just do not have a clear set-up. I have seen that U.S. equity index futures are trading higher, despite higher Treasury yields very early on Monday morning. I'll continue to play the environment in front of me, not the one I hope for, nor the one I expected to see. I did tell you that there would be a late-week rally last week. I, however, was a day late as I thought that rally would kick in on Thursday. Instead, we did see an improvement in market breadth that baked for a day or two prior to upside movement in the headline indexes.

Earnings

With the unofficial kick-off of the fourth quarter earnings season set for next week, it's time to start thinking about corporate profitability and sales growth yet again. According to FactSet, the S&P 500 is expected to have grown earnings 11.9% year over year for Q4 2024 on revenue growth of 5.1%. Still using data provided by FactSet, from Sept. 30 to Dec. 31, the consensus estimate for S&P 500 Q4 earnings dropped from $63.60 to $61.88, or -2.7%.

While this is the 12th-consecutive quarter where earnings estimates contracted during the quarter, this is not an exceptionally large drop-off. The Energy and Materials sectors led the contractions. As for the current quarter (Q1, 2025), consensus is currently for a very similar looking earnings growth of 11.9% on revenue of 5.1%. For the full year 2025, Wall Street sees earnings growth of 14.8% on revenue growth of 5.8%.

On valuation, the S&P 500 went into the weekend trading at 21.4-times 12-month forward looking earnings and 27.5-times 12-month trailing earnings. These ratios are well above their respective five-year averages of 19.7-times and 24.2-times respectively.

So, Stay Long NVDA?

Readers may or may not have noticed that in a blog post on Friday, Microsoft MSFT announced plans to spend about $80 billion on the construction of data centers that can handle the firm's AI workloads in fiscal 2025. Reportedly, more than half of this infrastructure spending will take place in the U.S. Just an FYI, Microsoft reported $20 billion in capital spending and assets acquired under finance leases for the firm's Q1 2025. The company's Azure platform and other cloud services drove sales growth of 33% for that fiscal first quarter with 12 percentage points of that growth provided by AI services.

The GDP Game

This past week, the Atlanta Fed revised their GDPNow model for the fourth quarter down to growth of 2.4 at a quarter-over-quarter, seasonally adjusted annual rate, from 3.1% the week prior. Among other central banks running close to real-time gross domestic product models for the current quarter, the New York Fed's estimate for fourth quarter growth remains 1.9%, while the Cleveland Fed kept its view for Q4 growth at 1.85%. The St. Louis Fed, however, revised their model for Q4 GDP growth down to 1.21% from growth of 1.48%.

The Atlanta Fed is still the upside outlier right now, but that model does appear to be moving toward something more in line with what the other regional Fed models are seeing. As readers well know, New York, Cleveland and St. Louis revise their models on weekends, while Atlanta revises its model daily, if necessary, based upon the macro release schedule. Atlanta will revise that model this week on Tuesday after the BEA published its data for November's U.S. balance of trade.

What's Ahead?

Good question. Aside from the all-week technology shindig in Vegas, this is December jobs week. While markets will take a day off to observe the National Day of Mourning for Pres. Carter on Thursday, and that will move the weekly data on jobless claims up to Wednesday, the release of the two Bureau of Labor Statistics surveys remains set for Friday morning. Right now, I am looking for non-farm payroll growth of 152,000 seasonally adjusted jobs with participation rising, unemployment staying put at 4.2%, but a rise in underemployment. Wage growth should hold steady at 4%.

As far as earnings, the environment will remain quiet until Friday. Though the big banks will kick things off next week, we do expect to hear from Constellation Brands STZ, Delta Air Lines, and Walgreens Boots Alliance WBA this Friday.

Lastly, and I don't really know how important this is, is the amount of Fed speakers who will be out and about on Thursday. The Fed has largely been missing in action over the past two weeks, I guess enjoying the holiday season. We'll hear from Gov. Lisa Cook this morning, Richmond Fed Pres. Tom Barkin tomorrow and then Gov. Chris Waller on Wednesday. Then, the FOMC Minutes from the last meeting will print on Wednesday afternoon.

Finally, with U.S. financial markets closed on Thursday, and very little heard from this group for weeks, we have at least four public appearances lined up. Joining Barkin who will speak on Tuesday and also spoke last week, will be Philadelphia Fed Pres. Patrick Harker, Kansas City Fed Pres. Jeffrey Schmid and Fed Gov. Michelle Bowman. Why would this group come teeming out of their cages on a day that markets are closed after hiding in the hovels for weeks? Maybe it's nothing. Maybe it's something. Keep it in the back of your minds as we progress through the week.

Economics (All Times Eastern)

09:45 - S&P Global Services PMI (Dec-F): Flashed 58.5

10:00 - Factory Orders (Nov): Expecting -0.3% m/m, Last 0.2% m/m.

The Fed (All Times Eastern)

09:15 - Speaker: Reserve Board Gov. Lisa Cook.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CMC (.79)

At the time of publication, Guilfoyle was long NVDA, MSFT equity.