Mapping the Market's Ugly Move, My Palantir Plan and Buffett's Pile of Cash

Let's see where we're going, what's ahead and get into the nitty gritty of the Nasdaq and S&P 500's charts.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The bird touched down, and my guys piled on. There were 27 of us. We were heavy with mortars and ammo. Good thing they sent a big bid, one of the old Vietnam War- era CH-53 Sea Stallions. In fact, this one, I still remember, was riddled with bullet holes (as so many of them were back then) straight from that conflict in Southeast Asia that allowed specs of sun to shine upon us as it groaned upon lift-off. I was the section sergeant, and senior Marine among the 27. I knelt between but just behind the pilot and co-pilot. I nodded at the pilot, a major, and pointed.

This was well before the days of GPS. We had to know where we wanted to go, and the chopper crew had to know how to get us there. No computers to help. Just a map, a compass, some guts... and some trust. It was too loud for the pilots and I to speak. I was pointing at a red "X" on my map and pounded my finger on it twice. The pilot understood immediately. A column of M-60A1 main battle tanks were counting on us to hold the high ground as they passed between two ridges in what would have been a dangerous place to be if we were fighting real Soviets.

If the pilot couldn't read a map back, it was as bad as not being able to read a map yourself. In this particular memory, we were fighting fake Soviets (other Marines wearing the plain green uniforms of the Soviet Army of the time), so our lives were not at stake (unless that rickety bird fell out of the sky), but if we did not hold the high ground when we were supposed to, and cover that draw between the two ridges with smoke as the tanks approached, there would still be heck to pay. Plenty of heck to pay. We had to know where we needed to be.

We had to know how to get there, if plan A (the helicopter crew) failed. That meant that we had to be able to identify certain items on the map once we were on the ground and be prepared to walk miles carrying hundreds of pounds of gear per man. We had a radio that we weren't supposed to use (radio silence), but we would have to order the tanks to take up a defensive position and not enter the area if we failed in our mission. Nobody wanted that.

I once served under a super-human, tough as nails Staff Sergeant. He was the one who taught us the tricks of moving swiftly and silently through wilderness and jungle environments, while avoiding ambushes and booby traps. He had been a tunnel rat in Vietnam, and he was a hero to all of us younger guys. He liked to say... "Know where you are, know where you need to go, and have more than one plan on how to get there." Oh, almost forgot, he also used to say... "Know when to get the (hockey puck) out of there."

Where Are We Now?

It wasn't all ugly. Really. Friday was ugly for equities and put a negative pall on the whole four-day workweek. There's no doubt about that. As traders and investors ran from equities ahead of the weekend, however, they did the old "Safety Dance" and bought both U.S. Treasury debt securities and gold. By Friday afternoon, the U.S. Ten Year Note paid just 4.43% after paying as much as 4.58% earlier in the week. As for Gold, the yellow metal ran from $2,907 to $2.972 per ounce last week before late profit taking left it at $2,948.

What happened? For starters, President Trump made remarks on Tuesday where he announced the intention to place 25% tariffs on imports of autos, semiconductors, and pharmaceuticals by April 2. This is on top of the levies already placed upon steel and aluminium, the increased tariffs on Chinese imports and the threats of new tariffs on Canadian, Mexican imports as well as reciprocal tariffs on everyone.

That's not all. As part of this administration's attempt to unwind decades of fiscal abuse that accelerated greatly over the past four years, Secretary of Defense Pete Hegseth wrote a memo to managers within his department to look for ways to cut most budgets by 8% per year starting with 2026. That was at least part of the reason for Palantir Technology's PLTR 15% beat-down last week.

Yes, I added to my PLTR long position after selling some shares on the way down. Yes, I see the potential for these pending budget cuts to benefit a big-data crunching / AI providing / Intelligence gatherer like Palantir greatly as perhaps the aerospace industry purveyors of large ticket items struggle. Yes, in all fairness, I am biased. That doesn't put me at any more or less risk, so my opinion stands.

Then There Was the Macro

Perhaps the selloff on Friday was a mix of human emotion and algorithmic response to several macroeconomic data-points that disappointed on Friday. First up were the preliminary February releases for the S&P Global PMIs for the U.S. The Manufacturing "Flash" was fine and has been for several months now. But the Services "Flash" stunned economists by printing in a headline state of contraction from the prior month. Then January Existing Home Sales (the largest slice of the housing pie) printed not only down 4.9% from December, but also well below consensus view.

That brought us to the University of Michigan's revisions to its February Consumer Sentiment survey. The headline print was revised all the way down to 64.7 from 67.8 earlier in the month, which is an unusually large revision for this series. That was down from 71.1 in January. What may have really rattled a few cages were the inflation expectations within the consumer sentiment survey. One year out, according to this survey, consumers now see inflation at 4.3%, unrevised from the preliminary number that many economists thought might have been incorrect and up from 3.3% in January. That, my friends, is awful.

The GDP Game

This past week, the Atlanta Fed left their GDPNow model for the first quarter unrevised at growth of 2.3% (quarter-over-quarter, seasonally adjusted annual rate). Among other regional central bank district branches running close to real-time GDP models for the current quarter, the New York Fed revised that estimate for Q1 growth down to 2.95% from 3.02%, while the Cleveland Fed still kept its view for Q1 growth at 1.85%. The St. Louis Fed, however, revised their model for Q1 GDP growth much lower, from 2.11% to 1.77%.

While there is no consensus as of yet on the current pace of economic activity, the trend of the first quarter does seem to be slowing down from where it was. New York, Cleveland and St. Louis all revise their models once a week, on weekends. Atlanta revises its model within hours of the release of GDP impacting data. This week, Atlanta will revise its model on Friday morning after the Bureau of Economic Analysis publishes its January data for Personal Income and Spending

A Whole Lotta Ugly...

Among the major to mid-major US equity indexes:

- The S&P 500 gave up 1.71% on Friday, and 1.66% for the week.

- The Nasdaq Composite gave up 2.2% on Friday, and 2.51% for the week.

- The Nasdaq 100 gave back 2.06% on Friday and 2.26% for the week.

- The Russell 2000 gave up 2.94% on Friday and 3.71% for the week.

- The S&P Small Cap 600 gave up 2.7% on Friday and 3.58% for the week.

- The S&P Mid Cap 400 gave up 2.4% on Friday and 3.02% for the week.

- The Dow Transports gave back 2.62% on Friday and 3.45% for the week.

- The Philly Semiconductors gave up 3.28% on Friday, but just 0.47% for the week.

- The KBW Bank Index gave up 1.83% on Friday and 3.49% for the week.

On Friday, nine of the 11 S&P sector SPDR exchange-traded funds closed in the red, led lower by Technology XLK and the Discretionaries XLI as four of these funds gave up at least 2% for the session. Interestingly, the top four performing sectors for the day were the four defensive sectors left by the Staples XLP. That's a sign of a nervous marketplace.

For the week, just six of the eleven S&P sector SPDR ETFs closed in the red, but all six of those funds gave up at least 1.97% over the four-day period. Interestingly, for the week, four of the top five performing sector funds were defensive in nature, again led by the Staples.

The Nitty Gritty

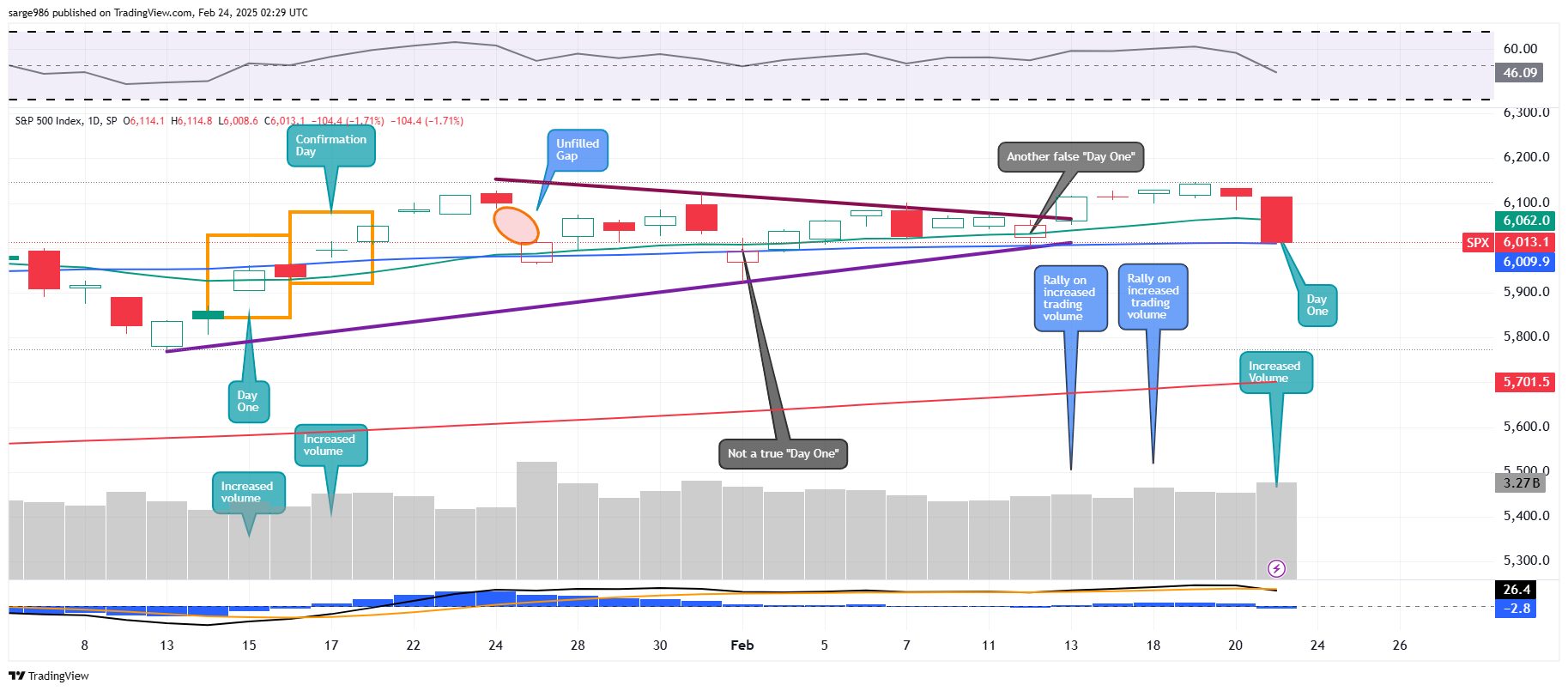

Friday presents a possible problem. For the day, losers beat winners by almost 3 to 1 at the NYSE and by greater than 3 to 1 at the Nasdaq. Advancing volume took just a 22.6% share of composite NYSE-listed trade for the session and a 35.9% share of composite Nasdaq-listed activity. Most importantly, on a day-over-day basis, aggregate trading volume increased by 12.9% for NYSE-listings, and by 15.4% for Nasdaq-listings. Trading volume also grew day over day across the membership of the S&P 500. That makes Friday a true "Day One" of a potential bearish change in trend. Now, we look for a "Confirmation Day" that must have some separation between itself and the "Day One" so they are not to be considered one large move.

Readers will see that the bullish breakout from the closing pennant formation started to fail on Thursday and then produced the actual "down" day on increased trading volume on Friday. There must be a break between this day and another higher volume "down" day that would serve as confirmation of a change in trend. This break can be just one day, or several days long. One positive take-away from the action for the S&P 500 on Friday is the fact that support showed up precisely at the 50-day simple moving average. This implies that at least some professional managers bought the dip late Friday.

Readers will see that the Nasdaq Composite is in a technically more fragile place than is the S&P 500.

While both indexes suffered a higher volume "down" day on Friday, the Nasdaq Composite failed to find any help at its 50-day simple moving average, which could prove significant, especially with Nvidia NVDA reporting this week.

Berkshire Hathaway Reports

Warren Buffett's conglomerate Berkshire Hathaway BRK.A, BRK.B reported fourth- quarter financial results on Saturday. Over the final three months of the year, Berkshire generated an operating income of $14.527 billion, which was up 71% from the year-ago period. This growth was led by a 302% gain in insurance underwriting, which ran to $3.409 billion, as insurance investment gained 50% to $4.088 billion.

But investment gains slowed from $29.574 billion for the year-ago comparison to "just" $5.167 billion. This put unadjusted net income attributable to Berkshire shareholders at $19.694 billion (-47.6%). Net earnings per "A" share worked out to $13,695 versus the year ago comp of $26,043, while net earnings per "B" share came to $9.13 versus $17.63.

The real news for the weekend may have been in the size of Warren Buffett's cash pile, which is now a whopping $334.2 billion, up from $325.2 billion. Is this the reflection of the market's elevated overall valuation? Is it just more difficult to find opportunity without Buffett's long-time co-pilot, Charlie Munger? Buffett did try to reassure investors in his annual letter:

"Berkshire shareholders can rest assured that we will forever deploy a substantial majority of their money in equities – mostly American equities, although many of these will have international operations of significance. Berkshire will never prefer ownership of cash-equivalent assets over the ownership of good businesses, whether controlled or only partially owned."

What's Ahead?

At least we have five full days to try to make a living this week. We do have that going for us. No holidays to interfere....

... The Fed will be quite active again this week. I am currently tracking 10 public speaking appearances by our central bankers this week from just Tuesday through Thursday. We have five scheduled at this time for Thursday alone and that number can still grow. The headliners this week from a markets' perspective will be Fed Gov Michael Barr who will speak on both Tuesday and Thursday and Fed Gov Michelle Bowman who is now considered the leader of the Fed's hawkish camp as inflation has been accelerating over recent months. Barr, by the way, has announced that while he will be stepping down from his role as Vice Chair for Banking Supervision, he will continue on as a member of the Reserve Board of Governors.

... The Macroeconomic calendar will heat up this week. The Conference Board will publish their Consumer Confidence survey for February on Tuesday. Traders, investors and economists will be watching to see if this survey shows the same collapse that the University of Michigan's survey did. On Thursday, the Census Bureau will release its January data for Durable Goods Orders. The key print within that print will be the core capital goods number as that is considered by most of us to be a proxy for business investment. Lastly, on Friday, we'll see January numbers for Personal Income & Spending as well as personal consumption index inflation. We'll also see January wholesale inventories, which matter more than many folks think.

... The earnings calendar is kind of light this week, but Nvidia NVDA, which may be the most important stock in our stock market, reports on Wednesday evening. That one release is probably the most important thing in either economics or business that will happen this week. Among other well-known names reporting this week are Domino's Pizza DPZ, Zoom Communications ZM, Home Depot HD, Lowe's LOW, Salesforce CRM, Snowflake SNOW and Rocket Lab USA RKLB.

Economics (All Times Eastern)

10:30 - Dallas Fed Manufacturing Index (Feb): Expecting 18, Last 14.1.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DPZ (4.91)

After the Close: CLF (-.67), FANG (3.38), ZM (1.31)

At the time of publication, Guilfoyle was long PLTR, NVDA, BRK.B, CRM, RKLB equity.