Making the 'Call' for a Skewed Options Expiration Day

Let's see what's different about this monthly options expiration Friday and why I expect to see some pressure and possible profit taking; also let's check the producer prices.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Happy Friday for all who celebrate. To be more specific, happy monthly expiration Friday. As today is the third Friday of the month, today is a monthly options expiration Friday. Is today different from any other monthly expiration? Well, yes. Goldman Sachs puts the notional value of this afternoon's expiration at a rough $3.4 billion, which in itself is nothing special. The difference is that the split between puts and calls is skewed rather heavily to call buying this time around.

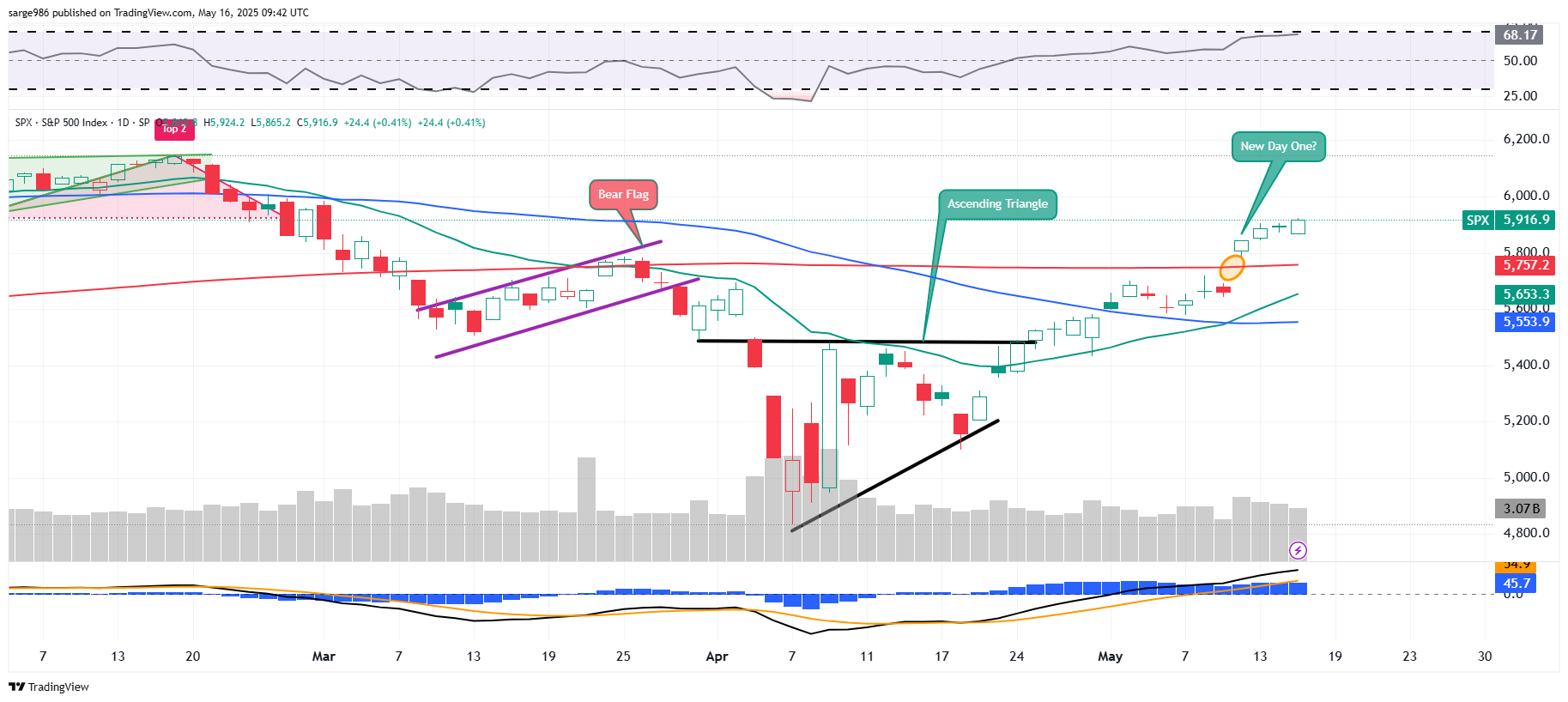

The S&P 500 is now up 6.25% month to date and up 22.4% since the low of the day on April 7. As for the Nasdaq 100, that performance stands at +9.02% for May and up 29% since April's low. The sharp decrease in long-side equity exposure in early April in response to the president's "Liberation Day" tariff announcements was followed by a sharp rally and increase in long-side equity exposure as deals have been made public and this trade policy has rapidly evolved into something far less severe than initially implemented.

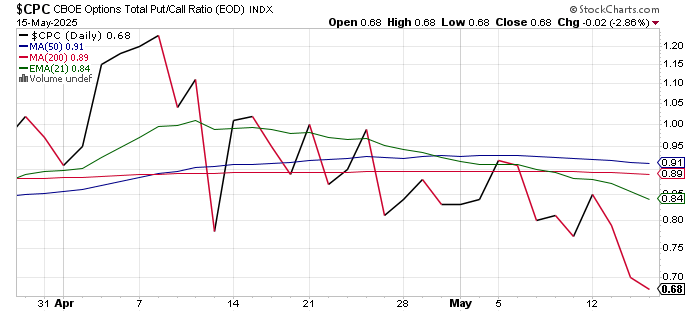

On Thursday, the CBOE Options Total Put / Call Ratio dropped to 0.66, which made a new low for 2025. Just look at what this ratio that measures put buying (bearish options bets) vs. call buying (bullish options bets) has done since those April lows....

It would be safe to assume that options dealers have had to hedge their exposure to a skewed market slanted toward the purchase of calls by purchasing stocks and/or equity index futures in order to protect themselves. The unwinding of this expiration, while at least some portion of these options will expire worthless, will likely pressure equity prices and probably has pressured equity prices to some degree heading into the event.

The unwind of equities held as a hedging mechanism could lead to a sloppy start to next week as well. Definitely not the end of the world. Just something to keep in the back of one's mind should markets inexplicably act erratically headed into this afternoon's closing bells. This may be a reason for traders to act. This is not, in my opinion, a reason for investors to get shaken out of high-conviction long positions.

Marketplace

Equity markets experienced on Thursday what might be seen as a positive day overall after rallying off of session lows that were made in the first 20 minutes after the opening bell. The S&P 500 gained a respectable 0.41% for the day, and that pushed the winning streak for that index to four consecutive days. The Nasdaq Composite, however, posted a loss of 0.18%, ending what had been a six-day winning streak for that index, despite a slight move into the green (+0.06%) by the tech-centric Nasdaq 100.

Small caps ruled the day on Thursday as the S&P 600 gained 0.6% and the Russell 2000 popped for a gain of 0.52%. The semiconductors finally faced some light profit taking as the Philadelphia Semiconductor Index gave back 0.57%. After having sold off through the recent rally across equities, capital flowed back into Treasury debt securities on Thursday as the yield on the U.S. Ten-Year Note dropped 8 basis points to 4.45%. That rally has continued overnight. At last glance, I see the Ten-Year Note paying 4.41%.

Breadth

These numbers are more positive than many probably expected to see on Thursday when I wrote this column twenty-four hours ago. Ten of the 11 S&P sector SPDR ETFs closed out the Thursday session in the green, but the positivity was led by the defensive sectors, which can be a negative signal for stock prices. The Utilities XLU ran 2.13% on Thursday followed by the Staples XLP, and the REITs XLRE. Only the Discretionaries XLY closed out the day in the red as broadline retailers stumbled, led lower by Amazon AMZN and Macy's M.

Winners beat losers by a rough 2 to 1 at the NYSE and by about 4 to 3 at the Nasdaq. Advancing volume took what I thought was a surprising 53% of composite NYSE-listed trade and a 50.3% share of composite Nasdaq-listed activity. However, aggregate trade ebbed further, as it has now for several sessions. Trading volume across NYSE-listings and Nasdaq-listings in the aggregate dropped by 4.6% and 10.2% on a day over day basis. Activity decreased across the membership of the S&P 500 from the day period for the third consecutive session.

In my opinion, the sideways action experienced over the past two sessions that includes a very mild "down" day for the Nasdaq Composite, does count as a pause after Monday's "Day One." This does not mean that stocks will rally today. Though equity index futures are trading higher overnight, I "more than half" expect to see both profit taking and some options-related pressure impact the markets going into this afternoon. Don't get me wrong... I'd take another rally, for I am but a man. That said, I would look at that "gift horse" in the mouth.

The Macro

Several domestic economic data-points printed on the weak side on Thursday. Growth in Retail Sales decelerated sharply in April from March. April Industrial Production "improved" to flat from the month period coming off of the March contraction as capacity utilization dropped a tick to 77.7%. The Empire State (New York) Manufacturing Index printed in contraction for a third month in a row in May, while the Philadelphia Fed Manufacturing Index posted a second straight month of headline decline.

The star of the day, though, economically speaking was the April print for producer prices. Often seen as a harbinger for consumer prices, headline PPI printed at a surprise -0.5% on a month-over-month basis with the so-called experts looking for something more like growth of 0.2%. At the core, PPI hit the tape at -0.1% with Wall Street expecting 0.3%. Clearly, at least the early impact of tariffs on U.S. producers and wholesalers have been greatly exaggerated. May, however, will be the true test. Walmart WMT did warn us on Thursday about May and June.

Even with subdued consumer-level inflation over the past few months and this outright deflationary April at the producer level, futures trading in Chicago are still not pricing in a Fed rate cut until Sept. 17 at this point and just a half percentage point of rate cuts for calendar year 2025 in its entirety.

Economics (All Times Eastern)

08:30 - Housing Starts (Apr): Expecting 1.365M, Last 1.324M SAAR.

08:30 - Building Permits (Apr): Expecting 1.45M, Last 1.467M SAAR.

08:30 - Import Prices (Apr): Expecting -0.4% m/m, Last -0.1% m/m.

08:30 - Export Prices (Apr): Expecting -0.2% m/m, Last 0.0% m/m.

10:00 - U of M Consumer Sentiment (May-adv): Expecting 53.1, Last 52.2.

10:00 - U of M One-Year Inflation Expectations (May-adv): Expecting 6.6%, Last 6.5%.

10:00 - U of M Five-Year Inflation Expectations (May-adv): Expecting 4.5%, Last 4.4%.

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 578.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 474.

1:00 - Long-Term TIC Flows (Weekly): Last $112B.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: RBC (2.70)

At the time of publication, Guilfoyle had no position in any security mentioned.