Low-Energy Computing: Nvidia, CrowdStrike Beat But Underwhelm

NVDA and CRWD topped Wall Street's expectations — but with some warts — and here's my plan for both. Also, let's check the latest in the Fed drama.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

That's it? That was what we all waited for? I should be grateful for the underwhelming response. I went into Thursday evening long both CrowdStrike Holdings CRWD and Nvidia NVDA. Mr. Market appeared to disapprove of what those two names released overnight, but not with much energy at all. Snowflake SNOW is trading nicely higher. Not long that one. Still, somehow, the ole' profit/loss has hung in there.

I expected my screens to exhibit a broad sea of red when I ripped my head away from that pillow at zero dark-thirty this morning. Instead, there's a little red toward the bottom of the screen. Most of the screen, though, and the only truly important number all the way at the bottom of the column at the extreme right are surprisingly green. Not by much, but green. I'll take it. Nvidia is no longer a top 15 holding of mine, but CrowdStrike is still a top five holding. I expected a beating. I am considering adding to both positions this morning. I did not trade after hours as the opportunity I was looking for never materialized.

Both Nvidia and CrowdStrike beat Wall Street's expectations for their respective top- and adjusted bottom-line results. There were some warts. Nvidia's data center-driven revenue fell a smidgen short of what Wall Street was looking for. CrowdStrike guided full year revenue and adjusted EPS above consensus, but guided current quarter revenue below expectations. I am not especially worried about either stock. I'll be back in a few hours with a deep dive in Nvidia's earnings release. Rah.

Musical Chairs

The Wall Street Journal is reporting that Pres. Trump is considering nominating either Stephen Miran or former World Bank Pres. David Malpass to replace Lisa Cook on the Federal Reserve Board of Governors. Cook is the Fed Governor accused of having allegedly committed mortgage fraud by Federal Housing Finance Agency Director Bill Pulte. Cook has sort of been fired for cause by the president but has hired legal counsel and is trying to remain in her position.

Miran has already been nominated to replace Adriana Kugler on the Board of Governors in the wake of her resignation. The president has suggested switching Miran over to Cook's seat as Kugler's term expires in a few months and Cook's term extends all the way to the year 2038. Malpass is a well-known economist who has been openly critical of the Fed's having kept short-term interest rates so high for so long.

At stake is this: The Fed's Board of Governors consists of seven members. Both Christopher Waller and Michelle Bowman have opined publicly in favor of lower interest rates and were nominated to their positions by Pres. Trump during his first term. Should this president replace two Board members in the near-term, he will have chosen a majority of the Board of Governors.

Now, remember, five regional branch presidents on an annually rotating basis, always have voting rights on policy, so this does not exactly hand the president the football on policy, but it does give him a leg up. Especially with Chair Powell's term at the helm (not on the Board) up in May.

What do I think? I think the courts have their work cut out for them. I have no idea whether or not Lisa Cook committed mortgage fraud. I will say this, though. If, as alleged, Cook did indeed fraudulently obtain lower interest rates for herself and then as a policy maker, voted repeatedly against lower rates for the American public... if that is really true, then she has no business working in any position involved in financial regulation. That's not political.

I have no problem, as my colleague Chris Versace has suggested, checking on everyone in a leadership position at the Fed or in either chamber of our legislature. If mortgage fraud is some kind of common practice among "public servants," then those practitioners need to be rooted out.

Wednesday

The past day was a quiet, but positive session one day after a technical confirmation of a bullish change in trend and ahead of a few high-profile earnings releases. The S&P 500 gained 0.24% on Wednesday, making both new all-time intraday and closing highs. The Nasdaq Composite tacked on 0.21%. These majors were outperformed by the small to midcap equity indices. The S&P 600, Russell 2000 and S&P 400 added 0.77%, 0.64% and 0.6% respectively.

Treasuries were quite strong on Wednesday despite a sloppy auction of $70 billion in U.S. Five-Year Notes. While the auction may have stumbled, yields across the slope of the curve moved lower. The Two-Year Note paid 3.62% (-6 bps) by day's end, while the Ten-Year Note paid 4.23% (-3 bps). It really did feel during the day, that there were less traders at their desks. I had not gotten that feeling earlier in the week.

Breadth

Nine of the 11 S&P sector SPDR exchange-traded funds closed in the green on Wednesday. Energy XLE led the way, gaining 1.12%, reinforcing the recent market dominance by the cyclicals. Health Care XLV placed eleventh for the day, which reinforces the recent underperformance by defensive sectors.

Winners beat losers by a rough 5-to-3 margin downtown across the street from George Washington and by about 5 to 4 uptown across the street from the Fighting Chaplain, Father Francis Duffy. Advancing volume took a 63.6% share of composite NYSE-listed trade and a 60.6% share of composite Nasdaq-listed activity. It was quiet, dudes. Have I mentioned that?

Aggregate trading volume dropped 14.9% on a day-over-day basis across NYSE-listings and by 11.5% across Nasdaq-listings.

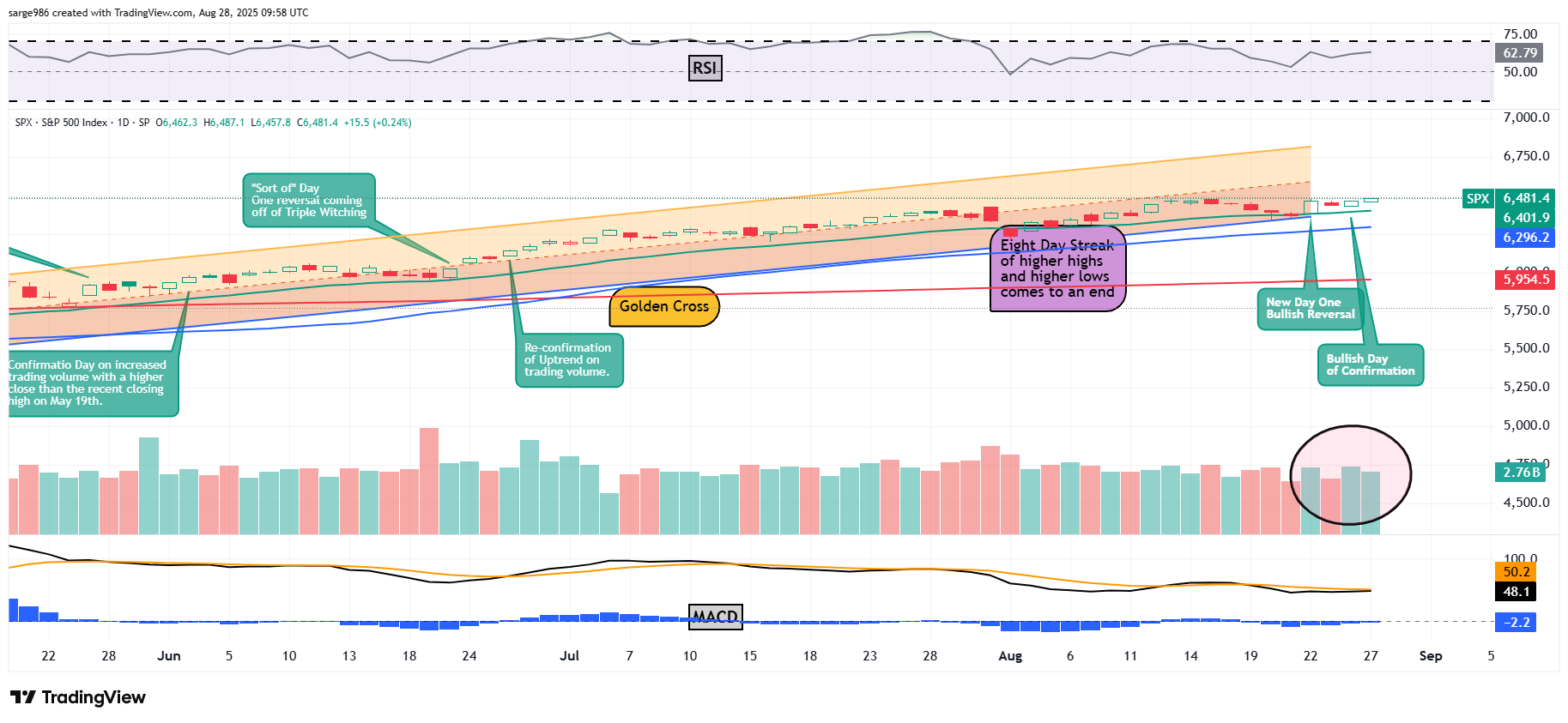

The chart above shows the Day One change of trend on Friday followed by the essential pause on Tuesday followed by the Bullish Day of Confirmation on Tuesday. This is straight out of the textbook, gang. Relative Strength is better than solid, but not technically overbought. Within the daily Moving Average Convergence Divergence, the 9-day Exponential Moving Average is still negative, while the 12-day Simple Moving Average is still (just a smidgen) below the 26-day EMA.

So, the daily MACD is not postured bullishly. The best I can say is that the two most important components of that indicator do appear to be moving in a more bullish direction. The pre-holiday lack of trading volume on Wednesday is illustrated within the circle coming off of a short period of obviously increased trading volumes on green candle days.

The Question

Now, I wonder... with Nvidia now come and gone and followed by a really muted overnight reaction, are traders and decision-makers really off to the beach for the weekend? Financial television will mention the Hamptons, but we all know that the decision makers are really in southern Florida in 2025 and have been for a few years now. Wall Street as an industry has not been physically on Wall Street in New York City for a very long time.

I mean, I am old-school, so I expect a lot from head-traders and strategists. We always gave the junior guys off around holidays because we needed the hitters at work in case certain prices were dislocated on light trading volume. Maybe, I am just from another time and place. That's very likely, but the Bureau of Economic Analysis will release its July data for Personal Income. Personal Spending and personal consumption expenditure price inflation on Friday, tomorrow. Imagine heading to the beach and leaving the office under the control of someone less experienced and maybe with less skin in the game on such a day? Not this cowboy.

Economics

(All Times Eastern)

08:30 - GDP Growth Rate (Q2-rev): Flashed 3.0% q/q SAAR.

08:30 - Initial Jobless Claims (Weekly): Expecting 233K, Last 235K.

08:30 - Continuing Claims (Weekly): Last 1.975M.

08:30 - Pending Home Sales (Jul): Expecting 0.0% m/m, Last -0.8% m/m.

11:00 - Kansas City Fed Manufacturing Index (Jul): Expecting -4, Last -3.

The Fed

(All Times Eastern)

6:00 p.m. - Speaker: Reserve Board Gov. Christopher Waller.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BBY (1.23), BURL (1.29), DKS (4.30), DG (1.57), HRL (.41)

After the Close: AFRM (.43), DELL (2.29), GAP (.55), S (.03), MRVL (5.08)

At the time of publication, Guilfoyle was long S, CRWD, NVDA equity.