Let's Play (Small) Ball ...

Here's how to manage risk in a time of uncertainty; also what kind of tariff plan can we expect now, a look at GDP expectations, and a check on aerospace and military contractors.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Traders and investors can probably expect the trading volume to ebb sharply Monday coming off of Friday's elevated "triple witch" expirations-related burst of activity. Readers will likely recall the "Inside Day" posted by the S&P 500 on Thursday, which signaled reduced volatility. That was exactly what transpired on Friday, despite the surge in trading volumes. It really is incredible how accurate technical analysis has become since trading algorithms took over from human traders several years ago. At least it does make traversing these markets that much easier for those of us who dare to continue to manage money actively.

Rise of the rebellion? More like, perseverance. More like a refusal to conform and let the machines take over everything. Sometimes, the old ways, if one stays motivated, if one stays as sharp as possible, are best. I know that I'm glad that I'm not just watching my portfolios go up and down, passively following the trajectory of the marketplace. I'll take my portfolios where I want them to go, thank you. The old Wall Street machine has defeated itself. By replacing the Irish kid from Queens, the Italian kid from Brooklyn and the Jewish kid from the Bronx with high-speed algorithms with a focus on technical analysis that many of us read the same way, they have made themselves more predictable on a short-term basis than ever before.

What to do when the mid- to long-term outlook becomes more uncertain due to decelerating economic activity, a trade war that may increase or decrease in intensity at any time, and policy makers that don't know which way to go? Shorten one's horizons. Play small ball. Narrow the scope of one's book. If one is usually comfortable managing 35 or 40 core positions, take it down to 20 or 25. Investors and traders can always ramp up the broadness of their exposure. That's not hard to do at all.

Narrowing the book when unsure and playing the short game is simple risk management, keeps some powder dry and is part of being versatile. Who are we if we are unable to adapt to changing environments? The old Wall Street thinks that they outsmarted us. I look at them sort of like the kids who were afraid to take off the training wheels. Afraid to do or think for themselves. Rock on.

Overnight

European equities and U.S. equity index futures are trading higher Sunday night into Monday morning as we traverse the zero dark hours. Bonds are actually selling off a little and that might be the best clue, except the U.S. Dollar Index is not down as much as I would have expected with these moves. The news? While markets appear to still be on edge and could go either way ahead of President Trump's April 2nd "Liberation Day," word is spreading that these reciprocal tariffs might be far narrower than first expected.

The Wall Street Journal reported on the story on Sunday evening. The "new" Trump plan supposedly will target something like "15% of nations with persistent trade imbalances with the US" rather than all nations that the US trades with. The plan will still likely cover the bulk of U.S. cross border trade.

The Numbers

What the major to mid-major U.S. equity indexes did as markets stabilized last week:

- The S&P 500 gained just 0.08% on Friday and 0.51% for the week.

- The Nasdaq Composite gained 0.52% but just 0.17% the week.

- The Nasdaq 100 gained 0.39% and just 0.25% for the week.

- The Russell 2000 gave up 0.56% on Friday but gained 0.63% for the week.

- The S&P Small Cap 600 gave back 0.6% on Friday, gaining 0.6% for the week.

- The S&P Mid Cap 400 gave up 0.51% on Friday, gaining 0.64% for the week.

- The Dow Transports lost 0.2% on Friday and 0.24% for the week.

- The Philly Semiconductors surrendered 0.94% on Friday and 0.89% for the week.

- The KBW Bank Index gained 0.23% on Friday and is an impressive 2.78% for the week.

On Friday, despite headline gains, eight of the eleven S&P sector SPDR ETFs closed in the red, led lower by the Materials XLB and the REITS XLRE, as Communications Services XLC led the winners. For the week, eight of these 11 funds closed in the green as Energy XLE gained 3.07% followed by the Financials XLF at +1.94%. None of these ETF gave up more than 0.23% over the past five trading days.

The GDP Game

The Atlanta Fed left its GDPNow model for the first quarter at a contraction of -1.8% (q/q, SAAR) last week, up from -2.1% prior. Among other regional central bank district branches running close to real-time GDP models for the current quarter, the New York Fed's estimate for Q1 growth stands at 2.72%, while the Cleveland Fed revised its view slightly to 1.86%. The St. Louis Fed's model has been on the rise of late and now stands at 2.25%.

While there is obviously no consensus as of yet on the current pace of economic activity, how deeply negative the estimate out of Atlanta is has to be concerning. While it is a serious model, the other three models produced by regional Federal Reserve district branches are nowhere near Atlanta. In my opinion, St. Louis has a very solid track record.

Where is Hedgeye's Nowcast Model? I don't want to give away their store and if you're a reader of mine, you know that I trust their work. They are almost smack dab in the middle of the range here, leaning just a smidgen to the expansionary side. The private sector consensus is for q/q SAAR growth of about 2.1%.

Military Contractors, Boeing News

On Friday, the president announced that Boeing BA had been selected to build the next-generation F-47 U.S. stealth, manned U.S. fighter jet. The F-47 will replace the F-22 Raptor, which is primarily a Lockheed Martin LMT product. Lockheed had been in direct competition with Boeing for this project, which is worth probably $20 billion up front and likely hundreds of billions over the long-term. Lockheed had been the favorite coming, at least according to my inaccurate sources after famously winning the F-22 and then the F-35 contracts.

The F-35 program has been a lucrative decades-long contract for Lockheed as the B-21 strategic bomber program has been for Northrop Grumman NOC. Boeing, which really had not won one of these large contracts since the F-18 Hornet, needed this win badly and that's what they got. Can this get the aerospace giant back on track after the mishaps regarding its civilian 737 MAX jetliners, the KC-46 mid-air refueling tanker program and the overruns of the Air Force One upgrade program? Investors can only hope.

On that note, Korean Air confirmed on Sunday, a $24.9 billion order placed with Boeing to acquire 50 new aircraft by 2033. The order is composed mostly of 777's and 787's. Along with this deal, Korean Air also signed a $7.8 billion agreement with GE Aerospace GE to provide eight aircraft engines along with the necessary maintenance and support that these engines need.

Marketplace

It was the "witching" hour on Wall Street. None of the major indexes really moved all that much. The S&P 500 and the Nasdaq Composite both posted headline-level wins, albeit just barely for the S&P 500. Both of these indexes did manage to end four-week losing streaks. As mentioned above, Thursday's "inside day" signaled a lack of volatility on Friday that prevailed despite a tremendous surge in trading volume. Just look at the trading volume on this chart of the S&P 500...

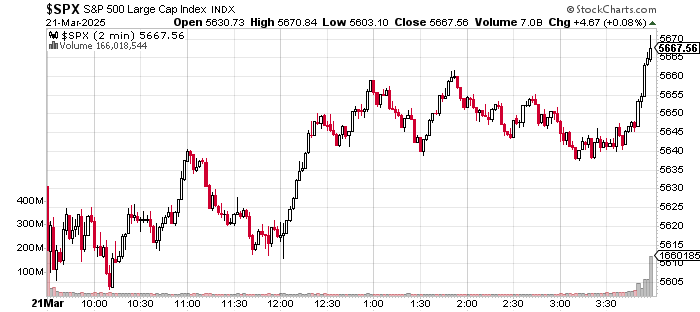

The day got off to a rough start as FedEx FDX, Nike NKE, and Micron MU all reported the quarterly numbers on Thursday evening and opened the session deep in the hole. markets did, however, not stabilize. Just take a look at the algorithmic surge into Friday's closing bell on this one-minute daily chart of the day's action...

Interestingly, despite the headline wins, on Friday, losers beat winners at the NYSE by a rough 9 to 5 and at the Nasdaq by about 7 to 5. Advancing volume took just a 35.3% share of composite NYSE-listed trade and a 45% share of composite Nasdaq-listed activity. The real kicker here was in the trading volume. Aggregate trade was up 100% (Yes, it doubled) on a day over day basis across NYSE-domiciled names and up 45% on a day over day basis across Nasdaq-domiciled names. Aggregate trade across the S&P 500 ran 89% above the 50-day trading volume simple moving average for that index.

Last Week

- While reaffirming for industry insiders, Nvidia's NVDA GTC conference in San Jose and CEO Jensen Huang's keynote address more or less fell flat with investors despite the introduction of several new products. Nvidia stock gave up 3.26% for the week. Is there hope? Of course. Palantir PLTR stock gained 5.47% last week after not reacting all that much in real-time the week prior despite announcing a bevy of new deals at AIPCon 6.

- The Federal Reserve provided a boost to financial markets last week. Though there was no change made to the target range for the Fed Funds Rate, the FOMC did slow down the pace of its quantitative tightening program on Wednesday. This is sort of a back-door way of, if not easing monetary policy, making it ultimately less tight. Fed Chair Jerome Powell also came off less hawkish in his press conference as the committee's economic projections displayed less confidence in where the economy is headed.

What's Ahead?

- Fed speakers are back this week. After the media blackout that had lasted the week prior to last into last week's policy decision, this week we'll hear from at least two Fed officials a day every single day. More will likely come out of the woodwork as well. So, Far, New York Fed Pres. John "Lightning" Williams on Tuesday morning, is the headliner.

- The Macroeconomic calendar is fairly full this week. The main events will be February Durable Goods Orders on Wednesday morning and February Personal Income and Outlays on Friday. The U.S. consumer will also be in focus as the February, the Conference Board will release their Confidence survey on Tuesday and the University of Michigan will release their Sentiment survey on Friday. February PCE data is due Friday as well.

- The earnings calendar will be excruciatingly light this week. Well-known names that are reporting do include McCormick MKC and GameStop GME on Tuesday, Cintas CTAS and Dollar Tree DLTR on Wednesday and Lululemon Athletica LULU on Thursday. That's about it, gang. Nothing to see here, really.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Mar-Flash): Expecting 51.9, Last 52.7.

09:45 - S&P Global Services PMI (Mar-Flash): Expecting 51.2, Last 51.

The Fed (All Times Eastern)

12:45 - Speaker: Atlanta Fed Pres. Raphael Bostic.

2:10 - Speaker: Reserve Board Gov. Michael Barr.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: KBH (1.58)

At the time of publication, Guilfoyle was long LMT, NOC, NVDA, PLTR equity.