Kass: With Fear Rising, I Could Soon Return to the 'Land of the Living'

Here's why I'm growing less bearish.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Market Is Afraid of Fear Itself

Market Is Afraid of Fear Itself

"Buy to the sound of cannons, sell to the sound of trumpets."

- Baron Nathan Rothschild

In recent weeks, equities have finally begun to reflect my prevailing fundamental, valuation and geopolitical concerns:

The purpose of this missive is to convey that, to me, the times (and markets) they are a-changin':

Come writers and critics

Who prophesize with your pen

And keep your eyes wide

The chance won't come again

And don't speak too soon

For the wheel's still in spin

And there's no tellin' who

That it's namin'

For the loser now

Will be later to win

For the times they are a-changin'

- Bob Dylan, The Times They Are A Changin'

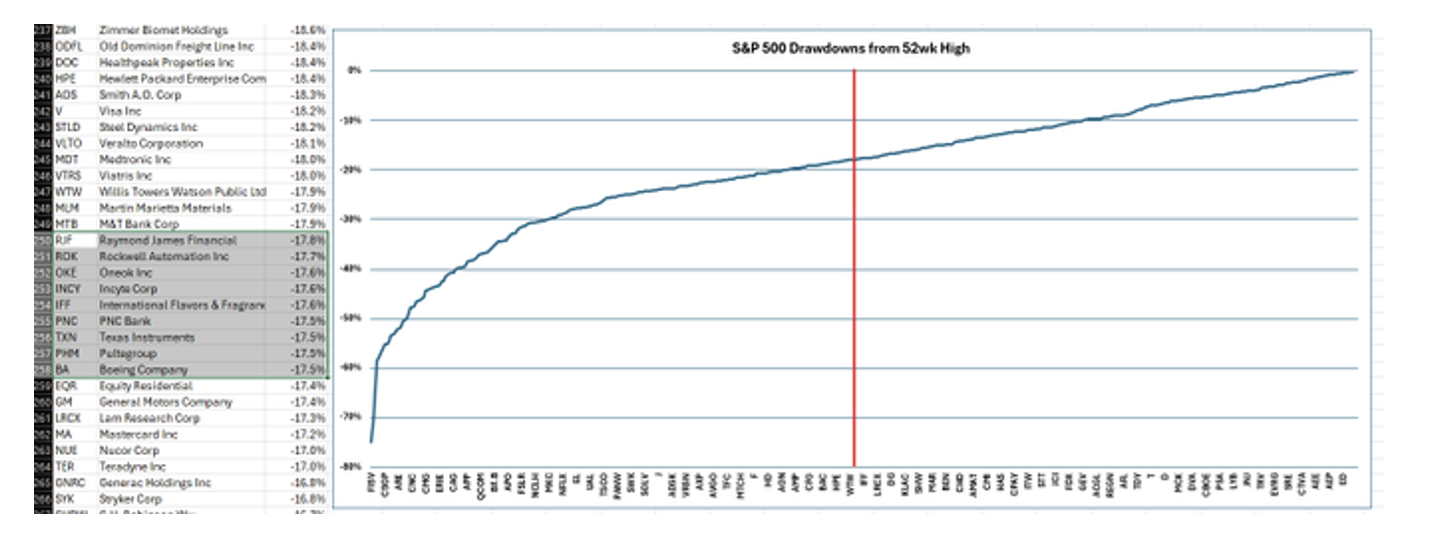

Under the ominous cover of the Iran conflict (and its economic ramifications), many stocks have quickly turned down by -25% or more, creating potential opportunities. The median S&P 500 Index stock drawdown is -18% (from the 52-week high):

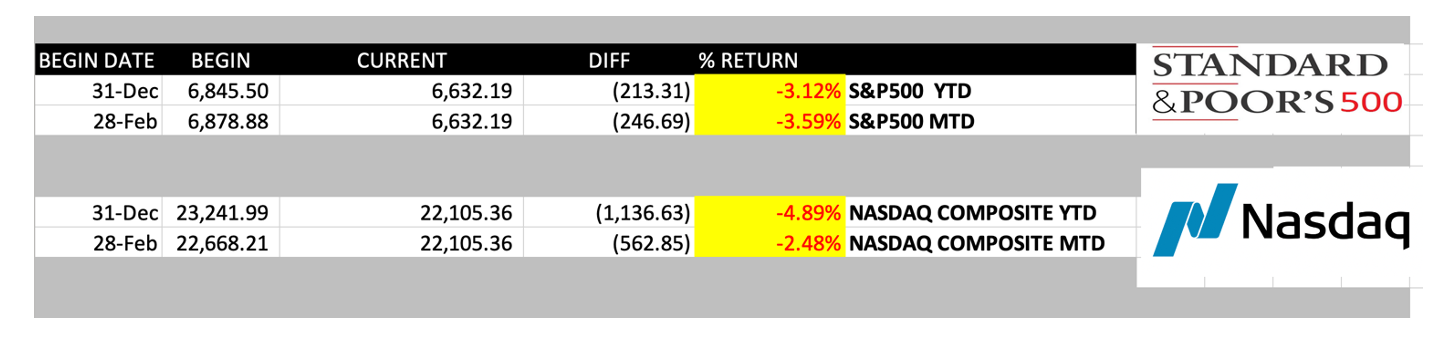

The S&P Index is now -5.4% from its peak in late January 2026. That is the 32nd pullback greater than 5% since the March 2009 Generational Bottom:

The S&P 500 is down 5.4% from its Jan 28 peak, the 32nd pullback >5% since the March 2009 low.

— Charlie Bilello (@charliebilello)

Video: https://t.co/1xWFG0G0KD pic.twitter.com/9fZdbcxEPv

The "league leading" Mag 7 bubble has burst — falling more than -10% below its October record. For the first time since 2022, all seven constituents are negative year to date:

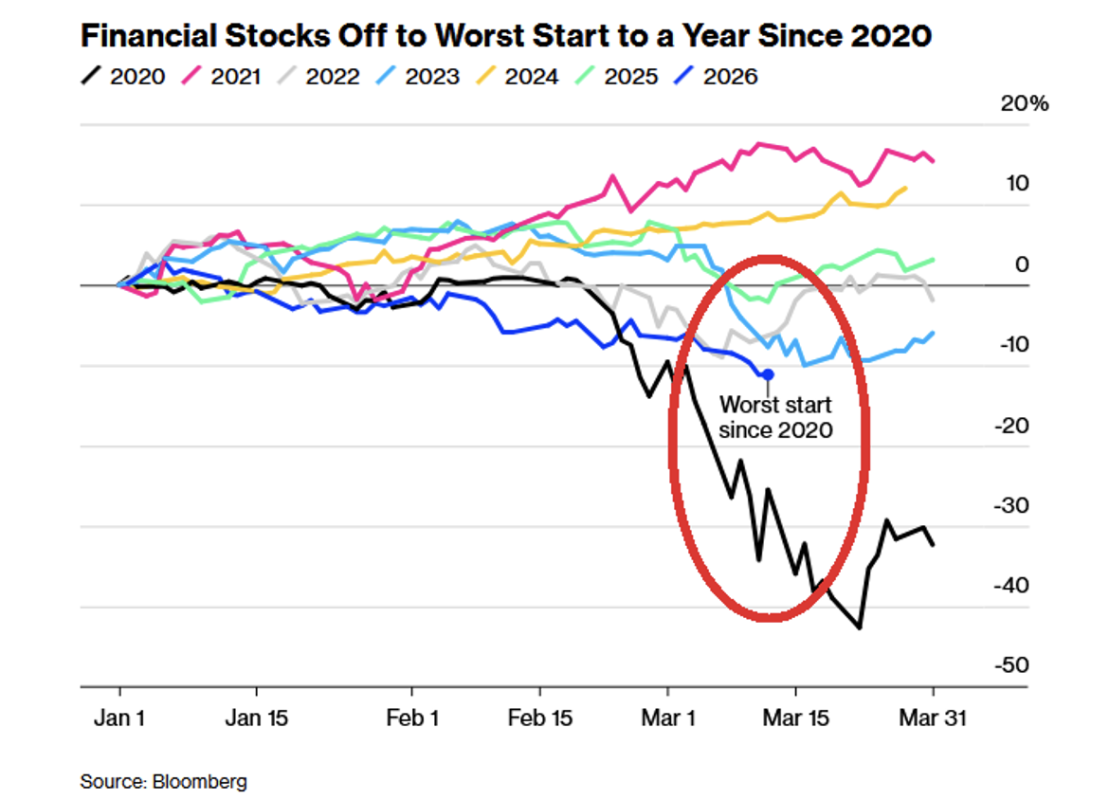

The S&P 500 Financials Index is -12% year to date — on track for the largest quarterly decline since early 2020. Private credit equities are down by over -30% year to date:

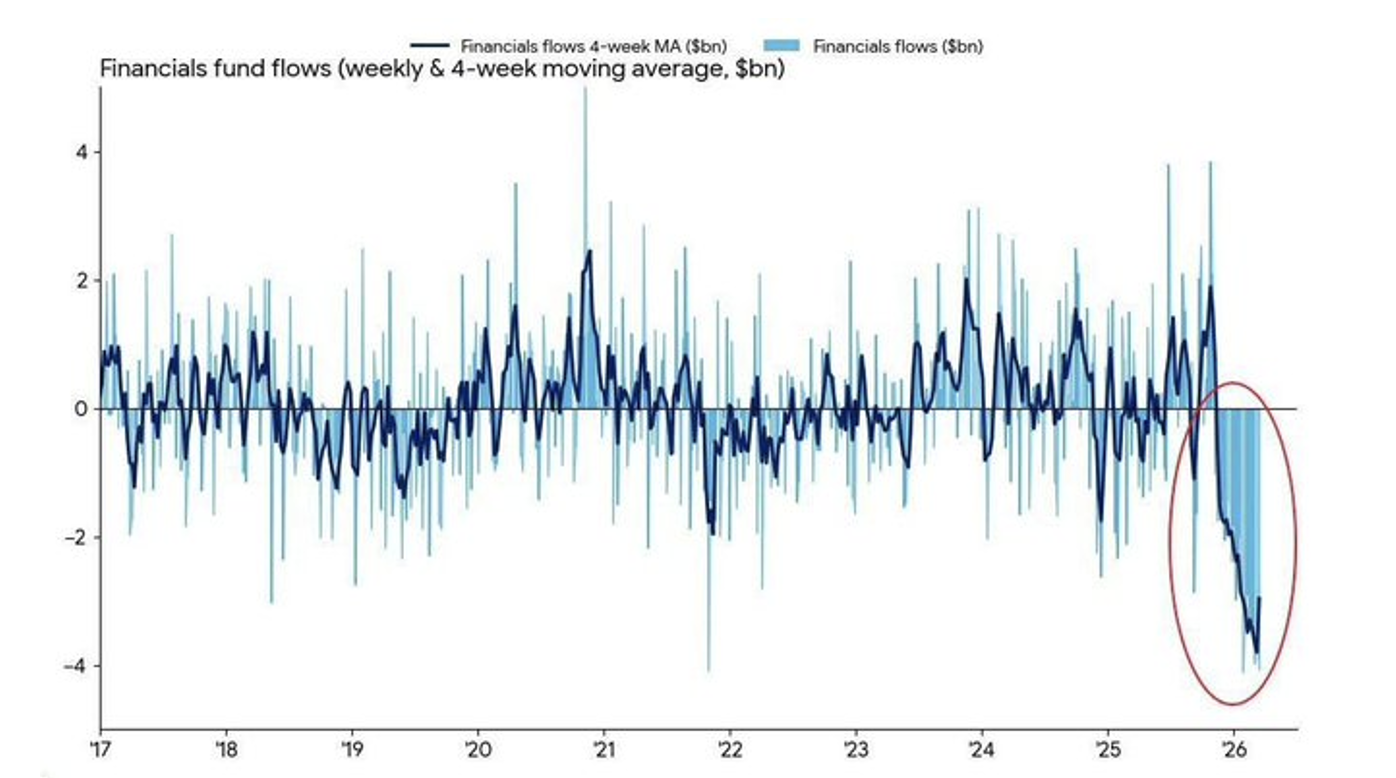

According to Bank of America, financial fund inflows are breaking records:

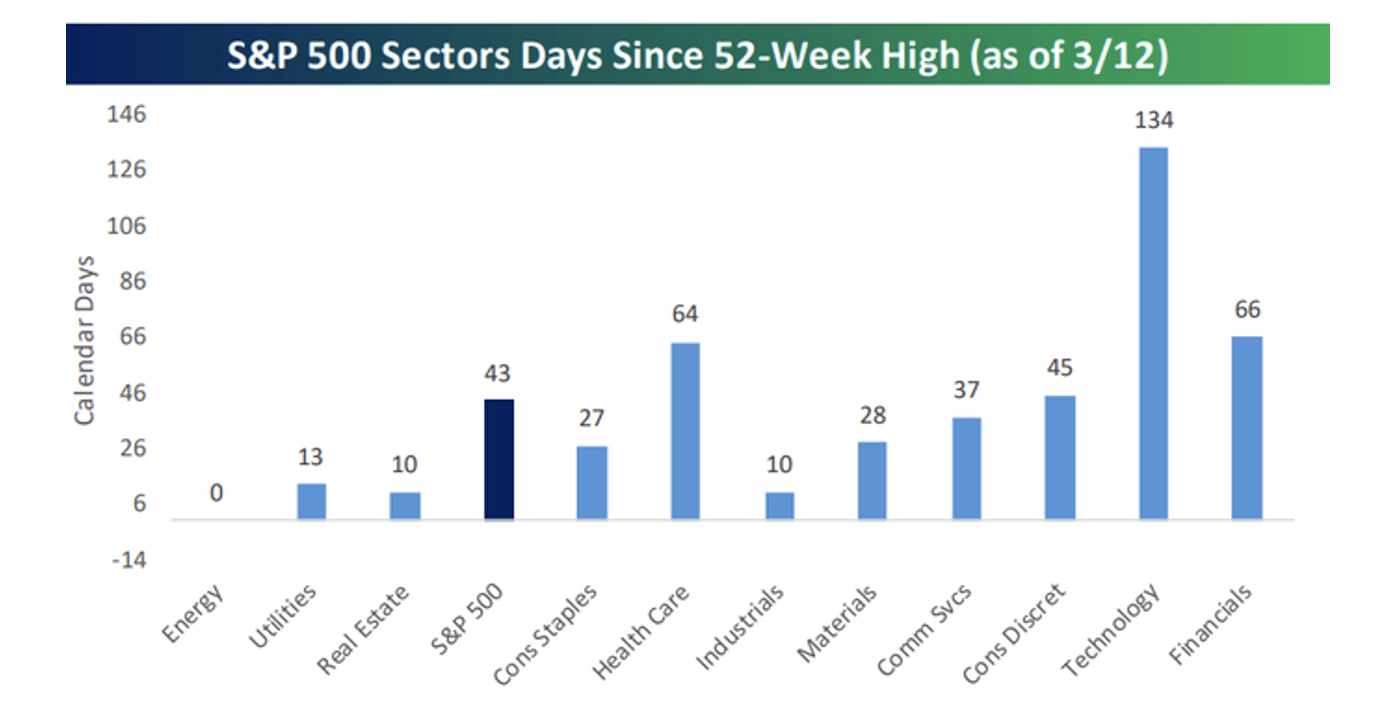

It has been over 40 days since the S&P Index reached its last 52-week high but 134 days since the Tech sectors' last 52-week high:

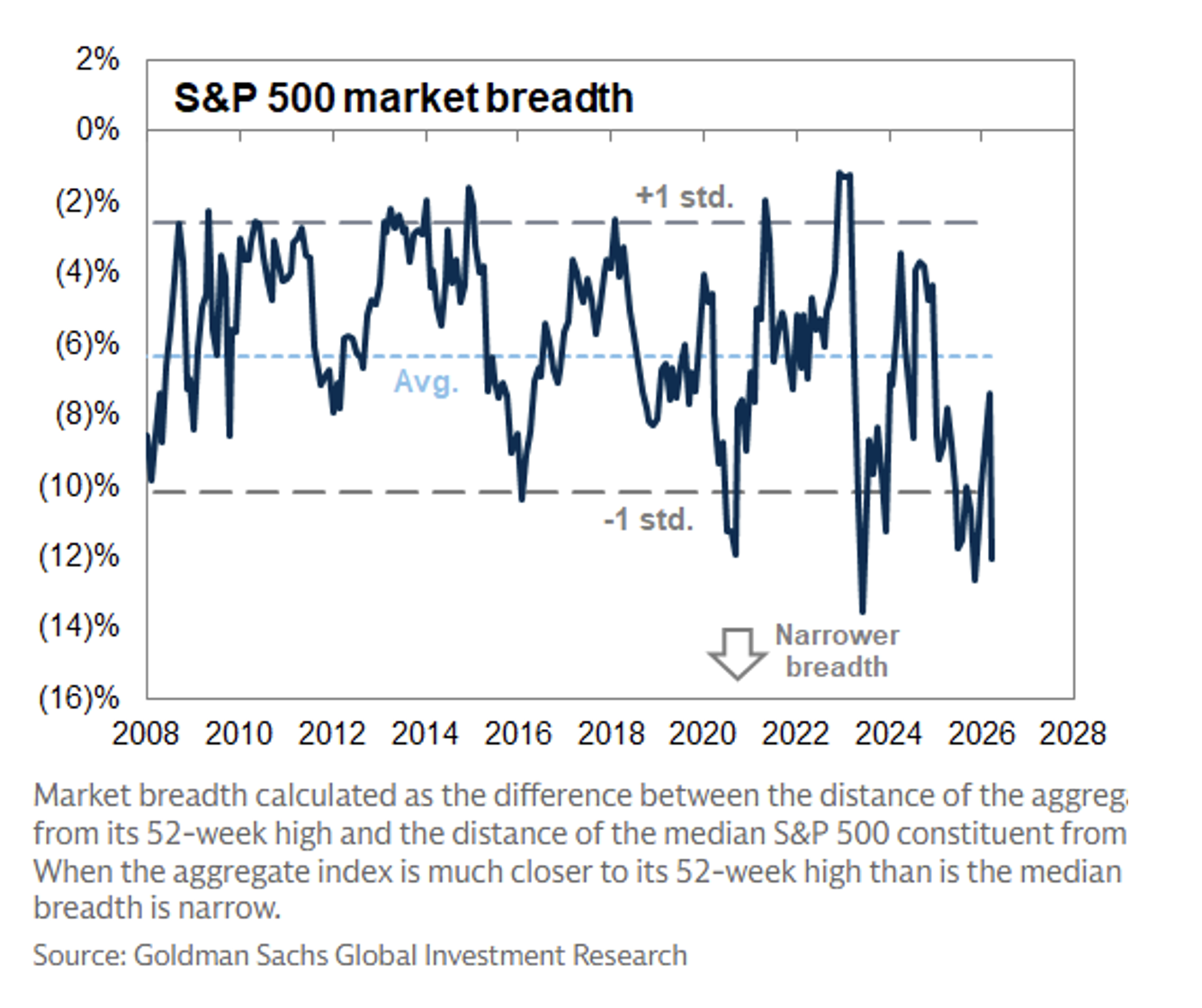

Meanwhile, market breadth (measured below by the gap between the S&P Index and its median stock relative to their 52-week highs) has a foul odor and may be approaching an extreme:

Besides the sharp fall in several market sectors, I am increasingly encouraged by the buildup in fear and that many market participants are coming around to acknowledging our multiple concerns.

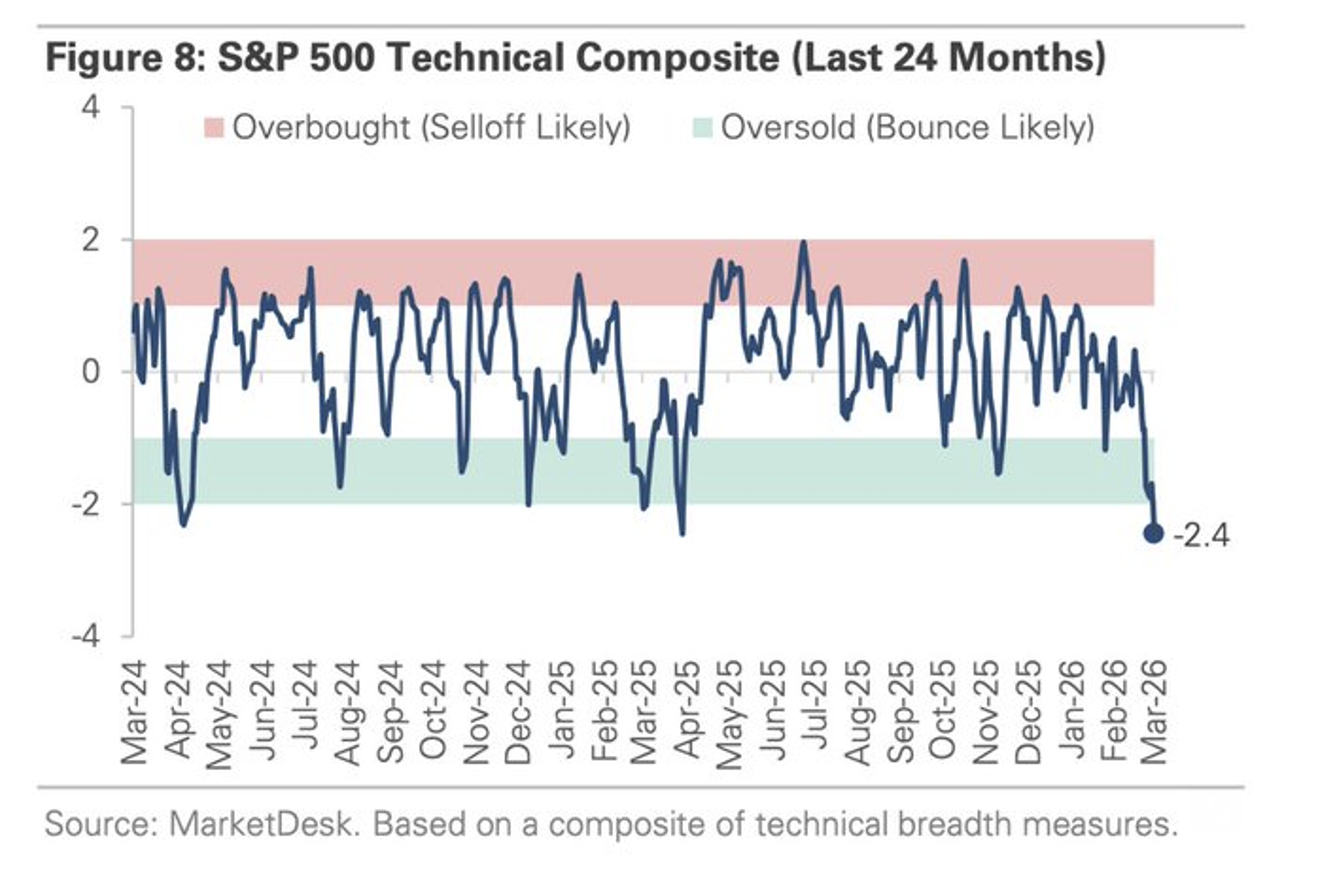

No longer overbought, the S&P Index has hit the most oversold in 24 months (this morning the S&P Short Range Oscillator hit -7.87%):

Money flows into (SPY) (the largest ETF) are nearing a bottoming level seen during the 2018, 2020, 2022, and 2025 crashes (a bottom is near in terms of time, not necessarily in the magnitude of the flush. A bounce must be sustained in the short and long term. See the local bottom of March 2022 for context):

As to Iran, today I am reminded of Baron Nathan Rothschild's famous quote (mentioned earlier):

"Buy to the sound of cannons, sell to the sound of trumpets."

Along with lower stock prices I have turned less bearish. As an example, I recently wrote in a letter to Seabreeze investors (my hedge fund):

In anticipation of a market correction/bear market we have substantially bolstered our cash position in order to take advantage of the possible developing long opportunities.

The purpose of this (mid-month) commentary Is to highlight that while markets have and may continue to move lower — considering the recent pace of decline, better values in the U.S. stock market are likely to emerge.

Accordingly, I have moved from a small net short exposure to a small net long exposure over the last several days. Should equities continue to fall — and subject to macro conditions (inflation, interest rates, economic and corporate profit growth, etc.) — it is increasingly possible that I will be "returning to the land of the living" by sensibly and gradually expanding our long exposure in the weeks and months ahead.

Though fear is elevated, over the short term much will depend on how long the Strait of Hormuz is closed. If the Strait remains closed another two weeks, the price of crude oil will remain high. This makes interest rates very challenging given how elevated P/E multiples are (below). This uncertainty suggests that a strong conviction (either way) does not seem appropriate — and a modestly long net exposure seems appropriate.

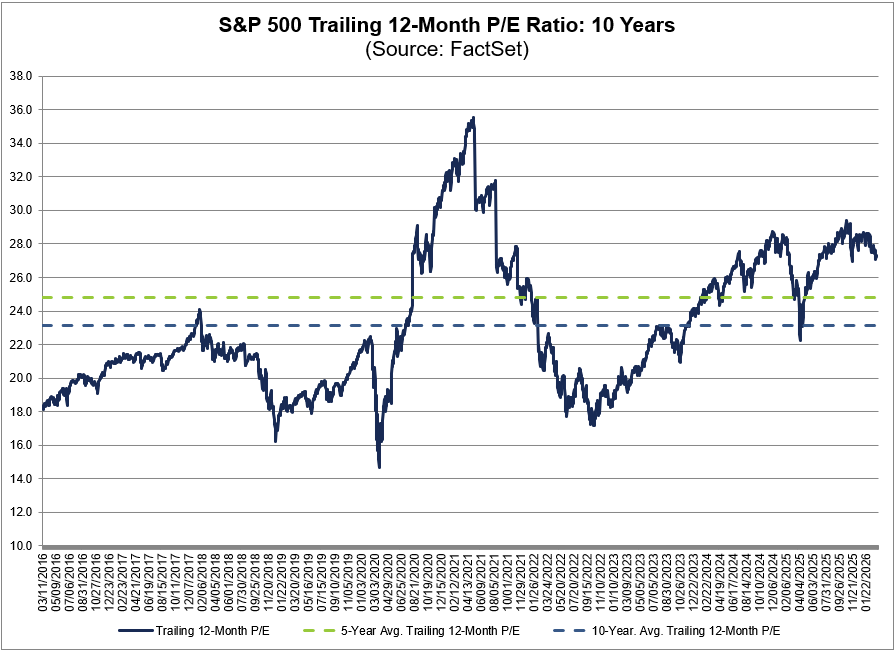

Equities continue to appear overpriced against history — this should be a limiting factor against "V" rallies:

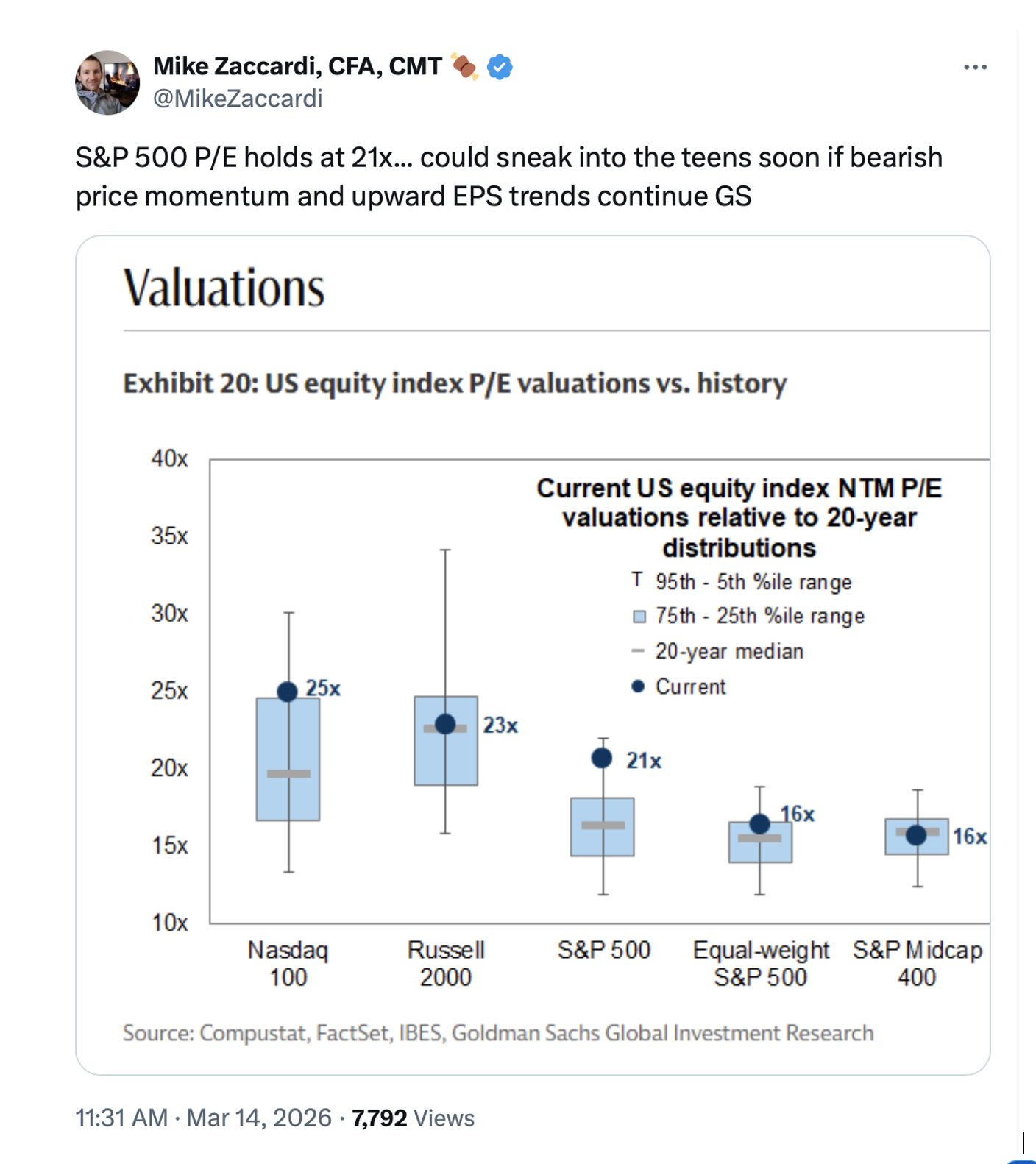

The trailing 12-month P/E multiple for the S&P Index is 27.2x, above the five-year average (24.8x) and above the 10-year average (23.2x):

No "V" Market Bottom Expected

I recognize that buying opportunities since early 2023 have been very brief and short-lived. With the benefit of hindsight, it was important to be prepared and bold to capture previous opportunity sets. This time, given the plethora of multiple challenges and headwinds — that have only recently been acknowledged by many investors — I expect a longer bottoming process that in the past. Accordingly, I will likely proceed in buying on a measured basis, waiting for the "right pitch."

Rarely Have Outcomes Been So Wide

For some time, I have been of the view that investors were underappreciating the risks of adverse geopolitical, economic and/or market outcomes — with many of them not friendly to stock prices and valuations. These concerns existed with valuations at about the 98%-tile and an equity risk premium that was slowly moving in the direction of being an equity risk discount.

Despite elevated valuations as well as reckless fiscal policy and rising geopolitical uncertainty — market participants put all of the concerns on the shelf. Stocks marched higher in 2023-2025. steadily climbing even though the probability of adverse outcomes were multiplying and gaining in probability.

The recent outbreaks of war in Iran (and Venezuela) are examples of adverse geopolitical developments (that I warned about in my 10 Surprises for 2026) that were universally ignored. The more serious U.S. incursion into Iran, in particular, is not an isolated adverse outcome. It is happening at a time in which the U.S. economy is slowing down, the rate of inflation is accelerating, and interest rates are rising:

* Slowing Economic Growth: According to the Commerce Department (on Friday) 4QGDP growth was only +0.7% — revised from the previous estimate of +1.4% and well below the consensus of +1.5%. Moderating domestic economic activity will feed into and weaken consensus S&P 2026-27 EPS expectations which remain too high.

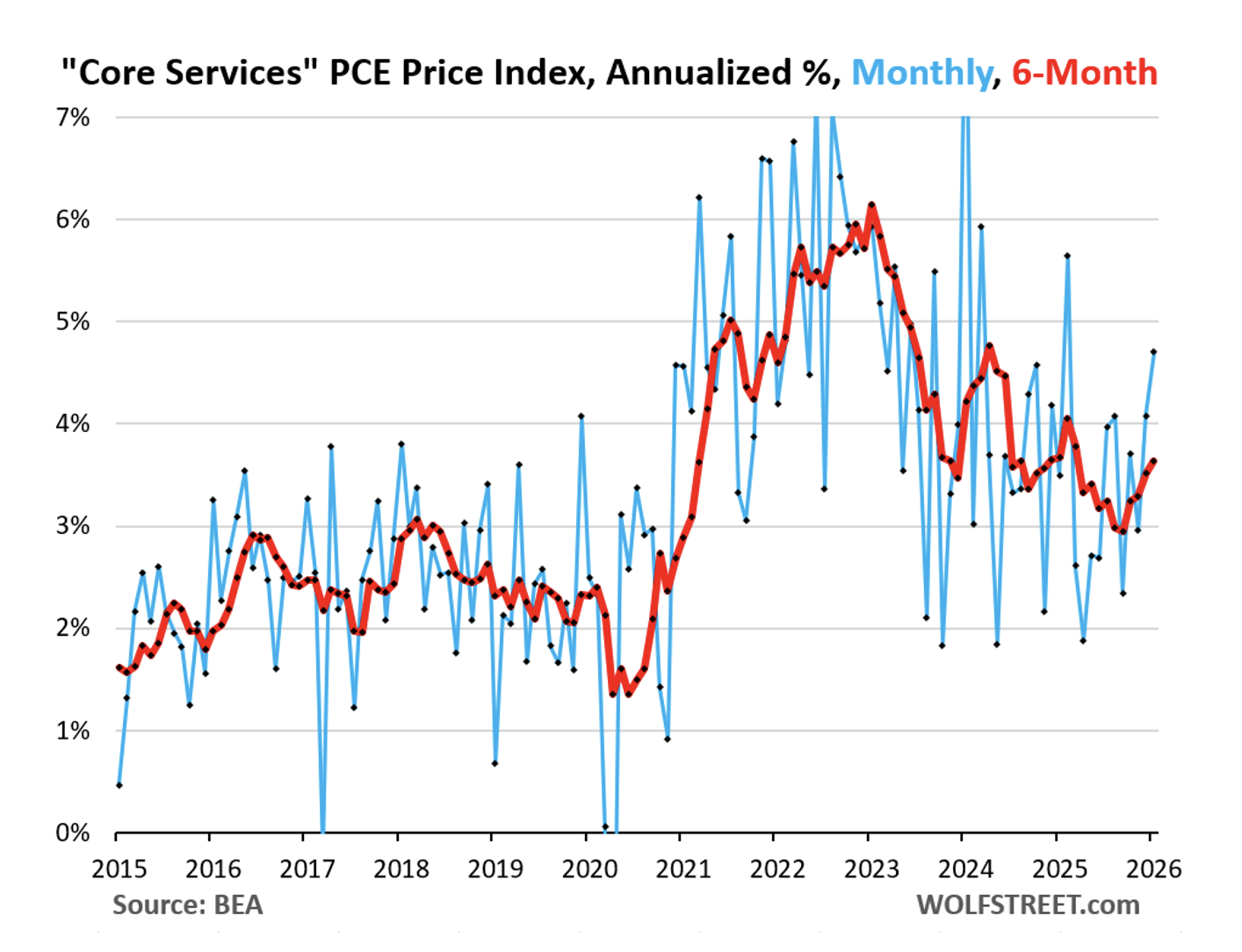

* Prickly Inflation: It was reported on Friday that February’s core PCE inflation rate (the Fed's favored inflation measure) hit 3.15%, the worst in two years — driven principally by core services which account for roughly 60% of the overall PCE price index (the energy spike is still to come).

The previously reported January core services PCE price index accelerated sharply both on a month-to-month basis (+0.38% or +4.7% annualized, blue line in the chart), and a six-month basis (+3.6% annualized, red line). This acceleration in January came on top of the acceleration in December. Year over year, the core services PCE price index accelerated to 3.4%. And it did so despite the deceleration of its housing components:

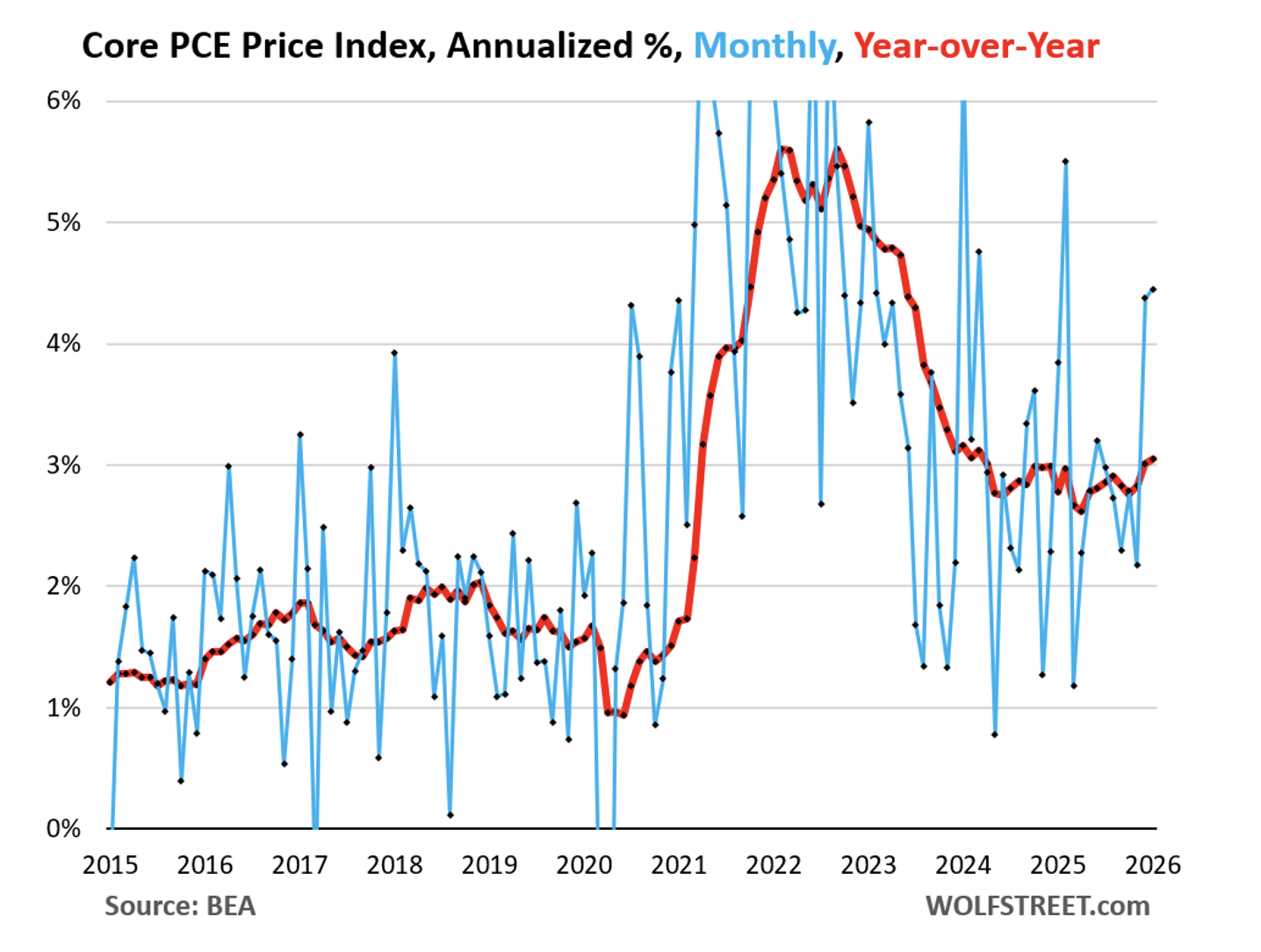

The January core PCE price index, driven by core services, jumped by +0.36% (+4.5% annualized, blue line) in January, after the big jump in December. Year over year (red line), it accelerated to +3.1%, the worst in nearly two years. It has been zigzagging higher and ever further away from the Fed’s 2% target since May 2025:

* Rising Interest Rates: Since the Iran conflict started on February 25, the yield on the 10-year Treasury note has risen by 38 basis points. This has contributed to a sharp rise in mortgage rates (from slightly below 6.00% last month to 6.28% today) and to an expanding equity risk discount.

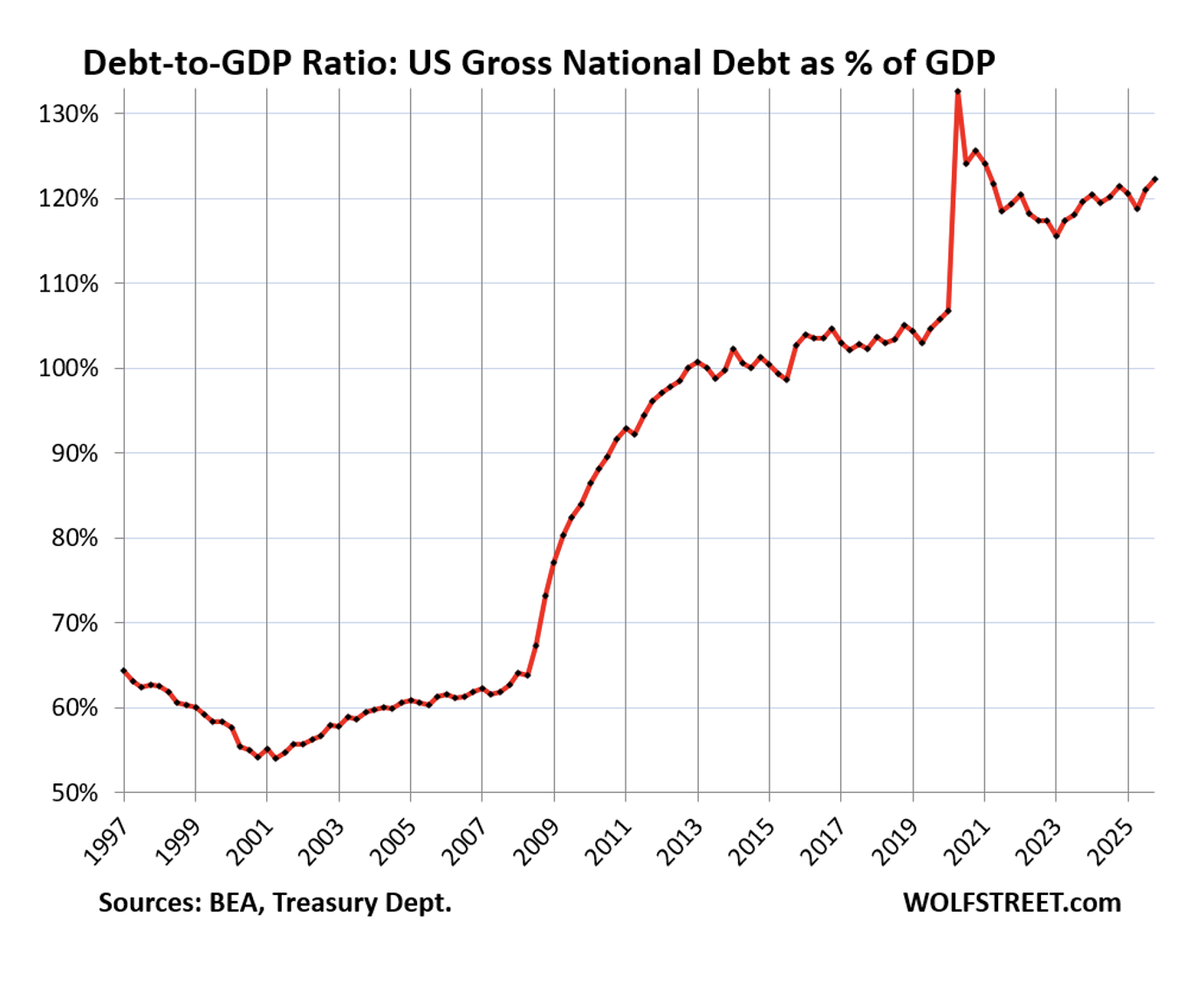

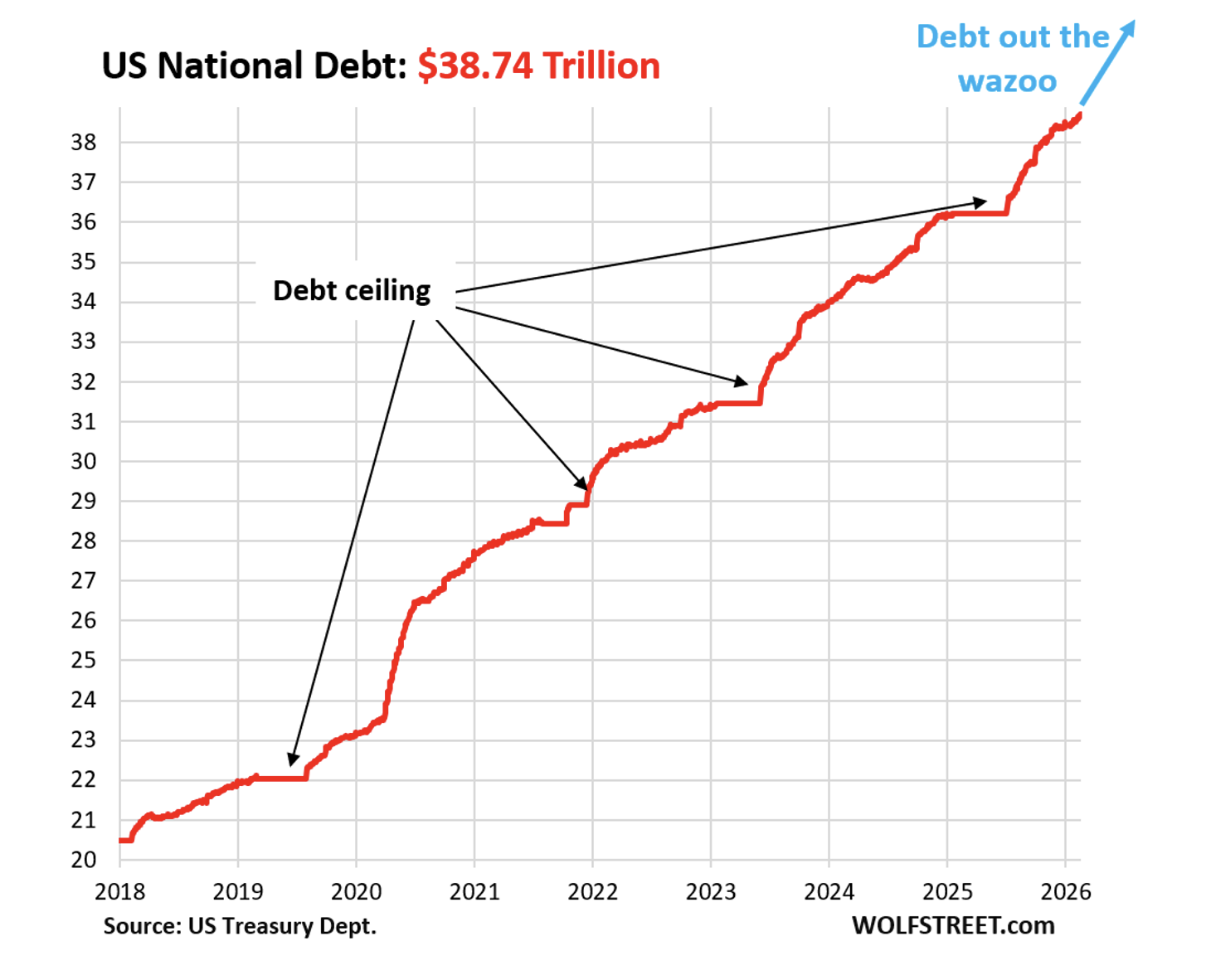

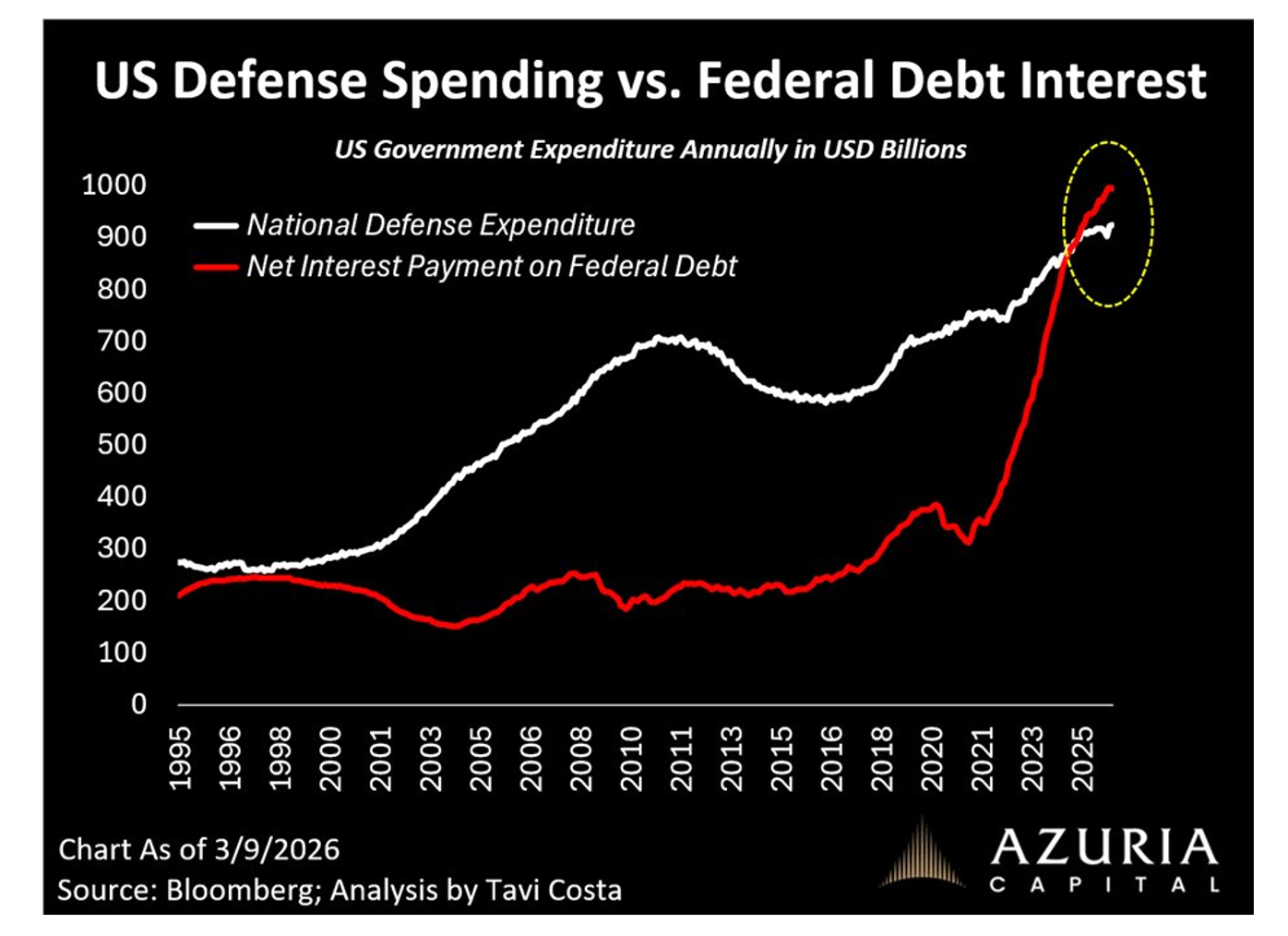

* An Uncontained National Debt and U.S. Deficit.

The war with Iran will ultimately be resolved. From an intermediate-term standpoint it is the cost and amount of U.S. debt that represents a growing existential threat:

* The Federal Reserve's Hands Are Tied: The Fed is now in something of a box as it needs to pay attention to the rise in the core PCE price index (of 3.1% and far from its 2.0% target) — especially with so much fiscal stimulus in the economy (government deficit spending, tax cuts for companies and individuals, bigger tax refunds to consumers now during tax-refund season, massive corporate investments in anything related to AI, too-low interest rates, and too narrow spreads.

Inflation feeds on these combined conditions.

Be Greedy When Others Are Fearful?

While the major indices are down only modestly from all-time highs, many equities are down in excess of -25%.

Until recently, we have seen a Bull Market in Complacency, as over the last year, fear and doubt have left Wall Street.

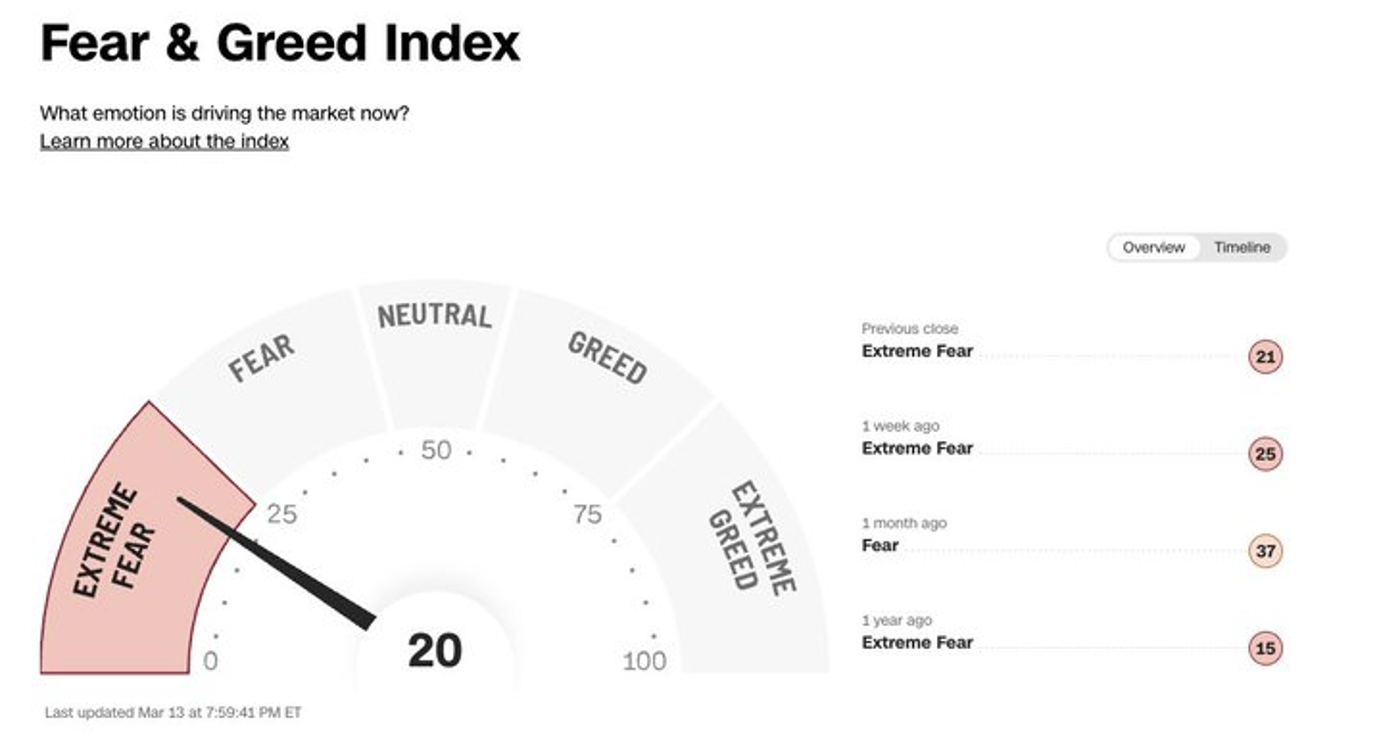

Over the last two weeks, fear has risen sharply and sentiment has flipped negative (as measured by The Fear & Greed Index, the Oscillators (S&P Short Range Oscillator (07.87%) and the Overbought/Oversold Oscillator), and the surveys (Investors' Intelligence, AAII, and NAAIM):

As reported by The Divine Ms M:

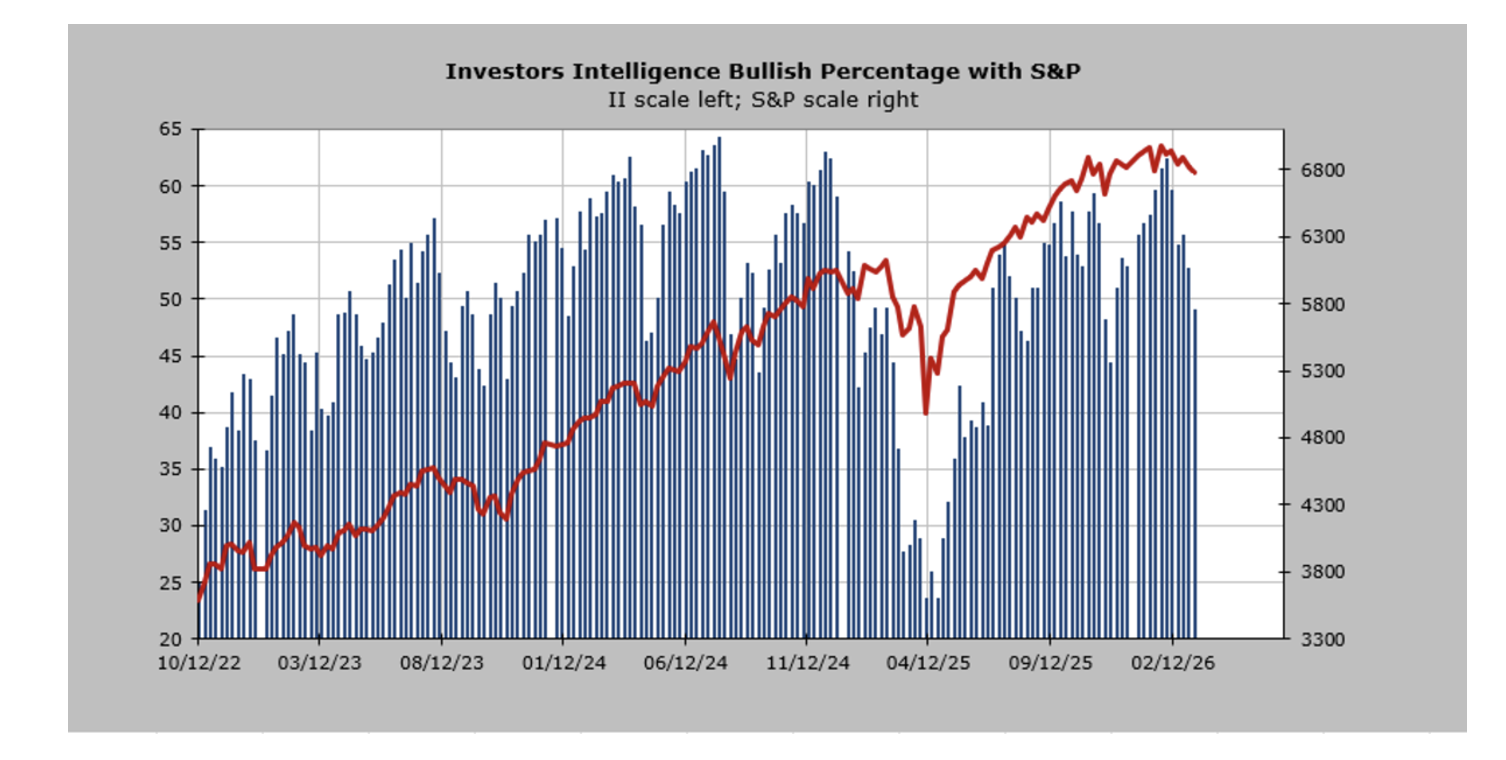

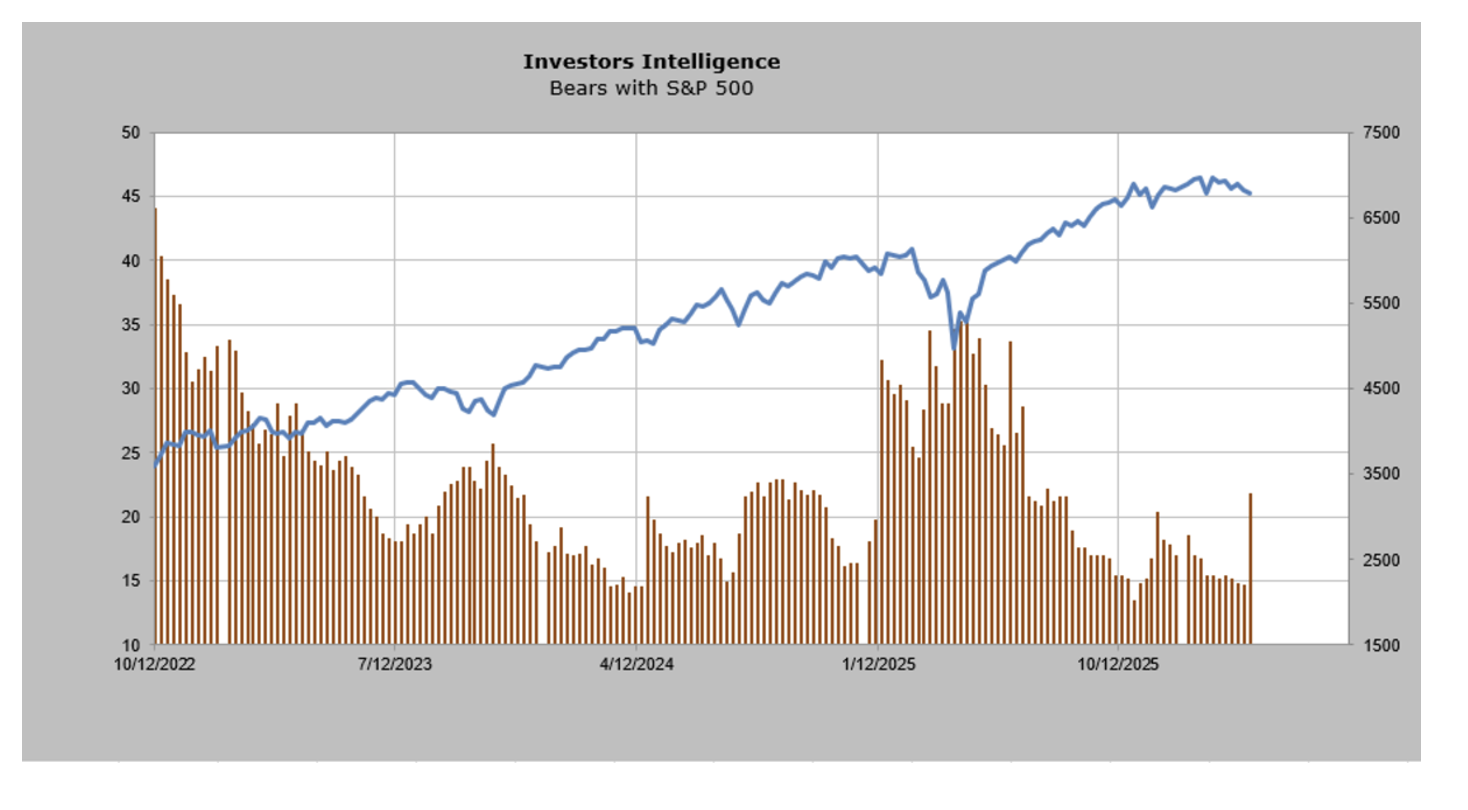

The Investors’ Intelligence Bulls have dropped off to 49% (compared to 63% in early February):

But what has caught our eye has been the large surge in bears — now at 21.8%, the highest reading since last summer:

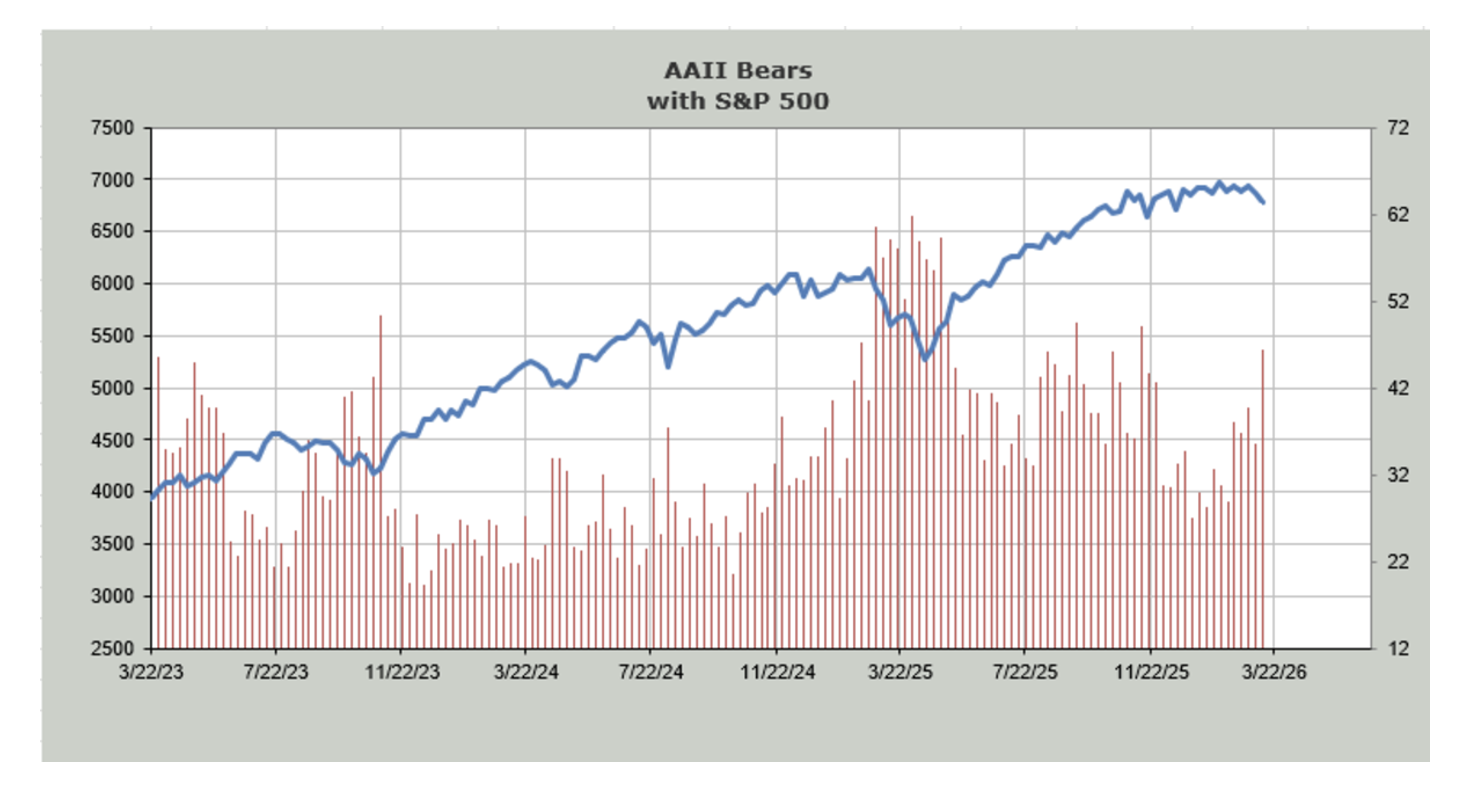

Joining in the pessimism of the Investors' Intelligence survey, is the AAII survey. The AAII folks joined the Investors’ Intelligence folks (shown here yesterday) in pulling back their horns. Like Investors' Intelligence, AAII bulls stayed mostly steady but the bears shot up by eleven points to 46%:

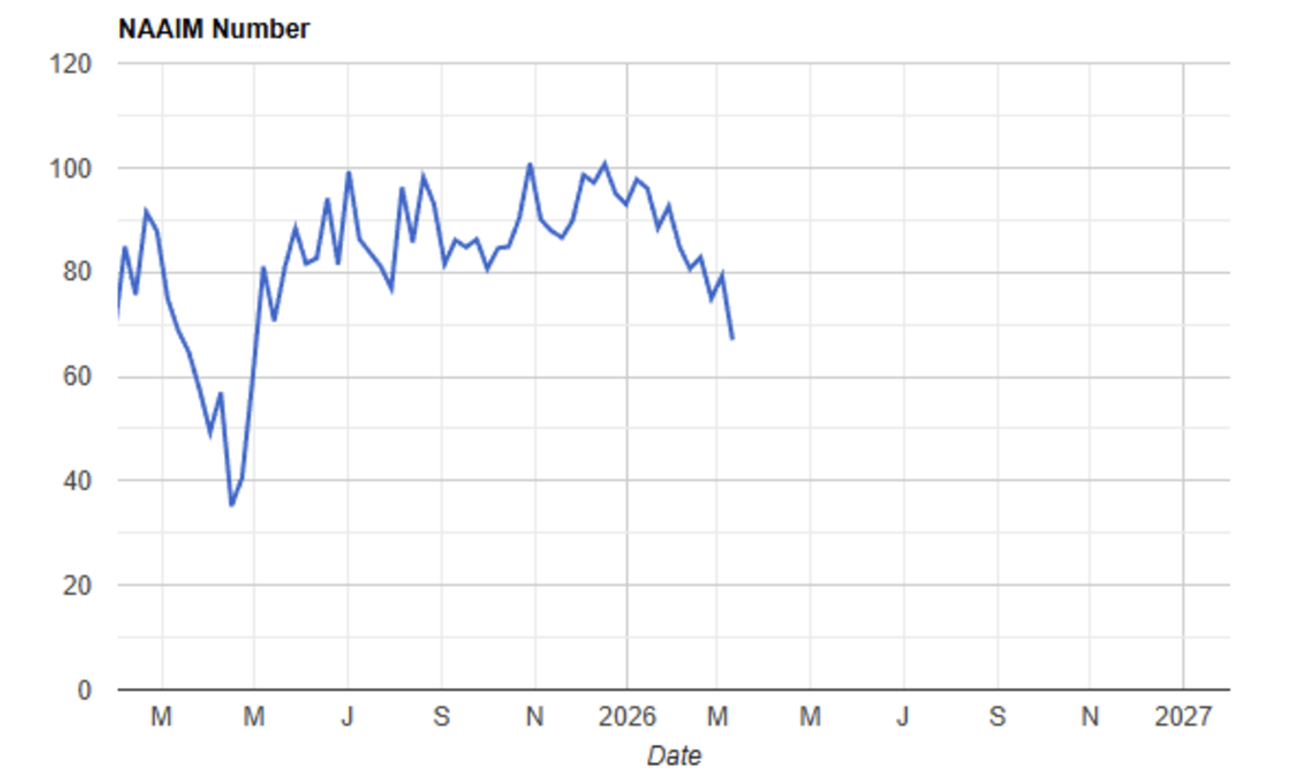

Following the previous surveys, the NAAIM survey also suggests that bulls are falling and bears rising. In December, their exposure was just over 100 (on margin). Now it’s down to 67, which is the lowest since the panic low of April 2025. Again, not extreme, but finally some movement off that complacency we were in for so long:

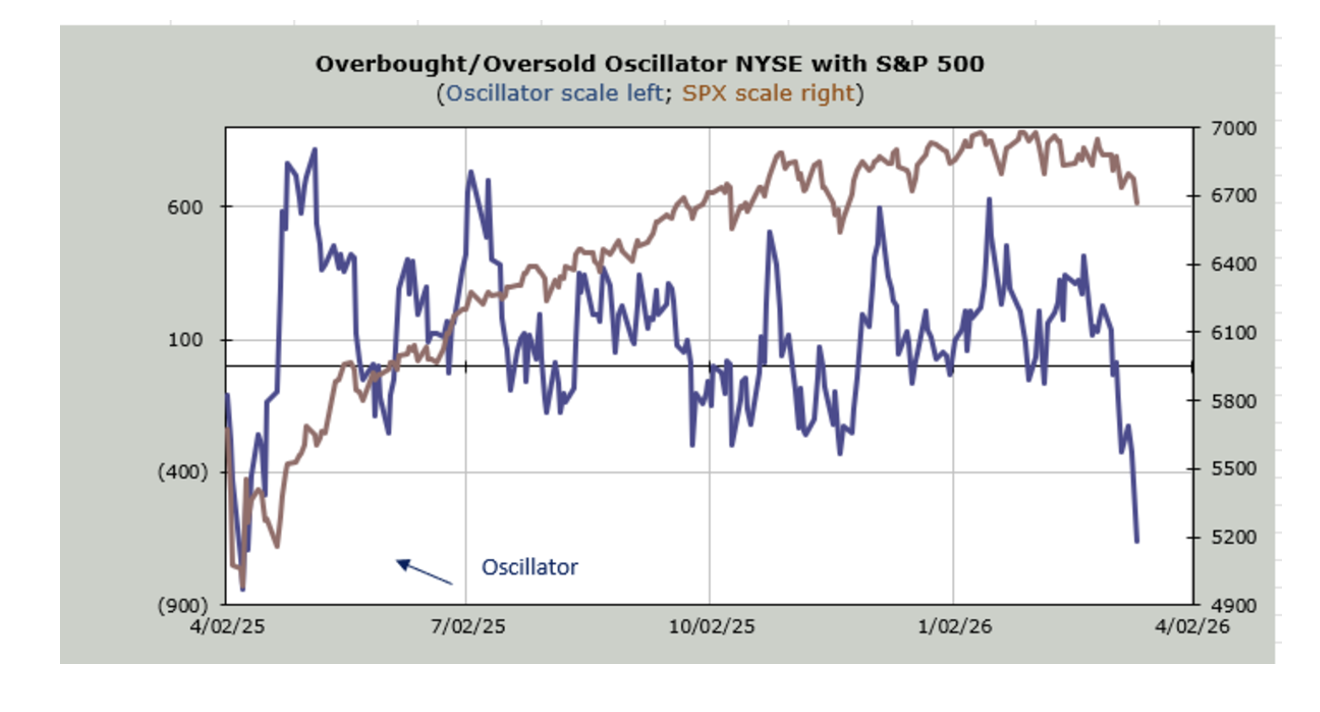

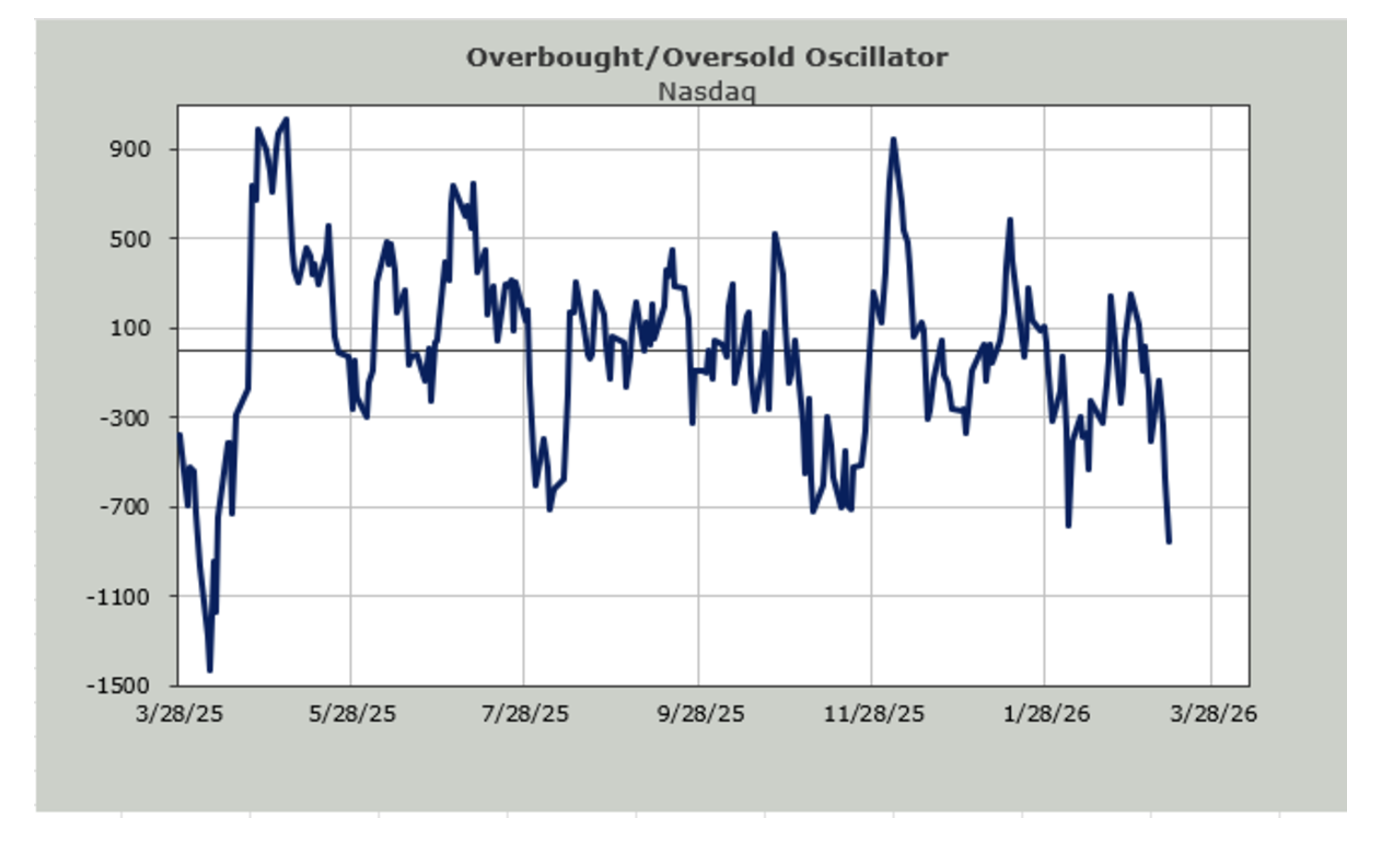

The Overbought/Oversold Oscillator is now nearing the April 2025 lows. (So is the S&P Short Range Oscillator reading near new oversolds). The last six trading days’ breadth has been red. And for seven out of eight, it has been red.

Here is the NYSE Overbought/Oversold Oscillator:

Here is the Nasdaq Overbought/Oversold Oscillator:

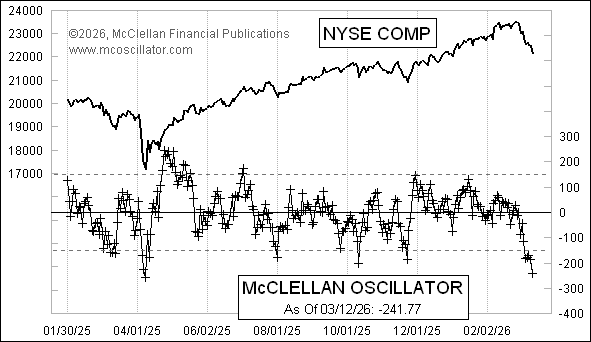

Finally, the NYSE’s McClellan Advance/Decline Oscillator has reached its most oversold levels since last April:

The War in Iran Is Frightening But It Will Likely Create Investing Opportunities

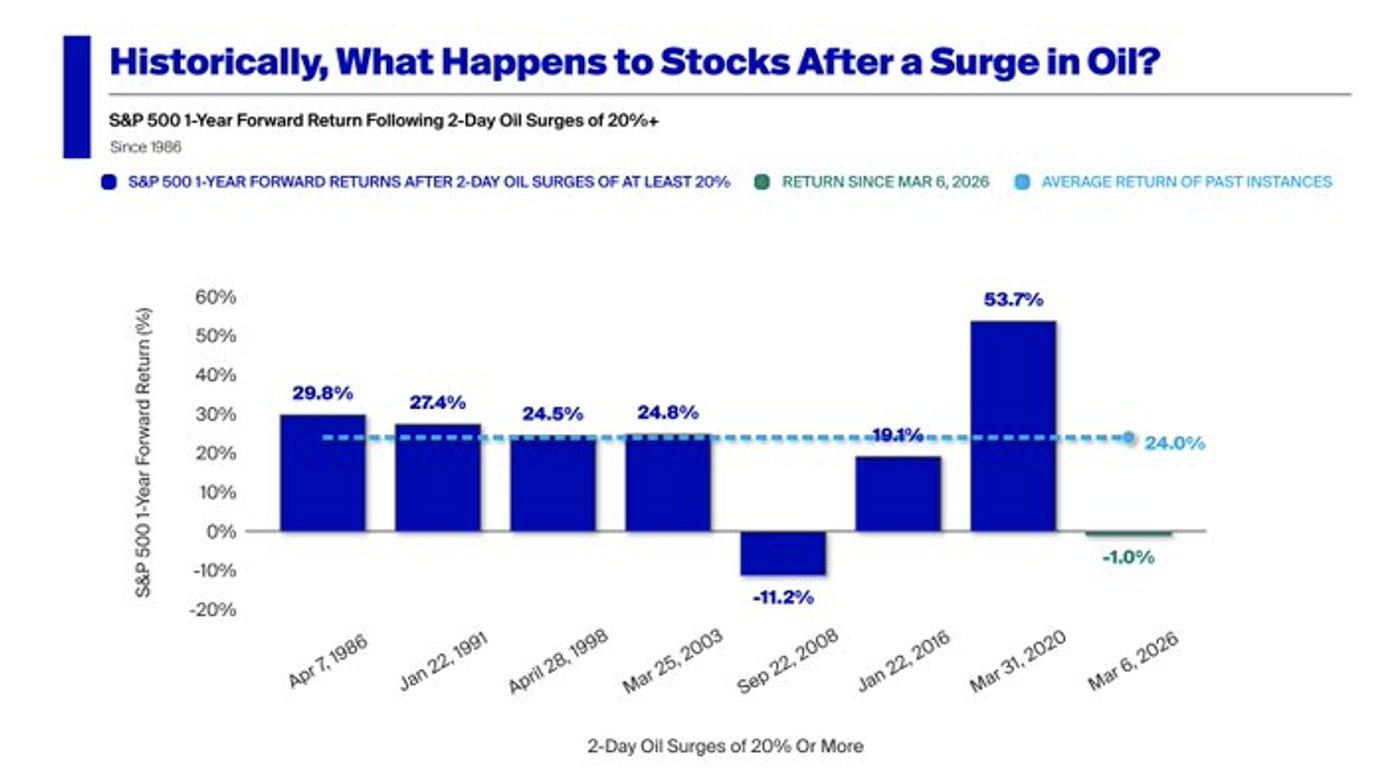

Baron Nathan's Rothschild's quote (mentioned earlier) has some historical weight, as equities usually respond smartly to conflicts that lead to a surge in oil.

There have been eight oil shocks in the last four decades. In seven of those instances, equities were higher one year later, with an average gain of +24%:

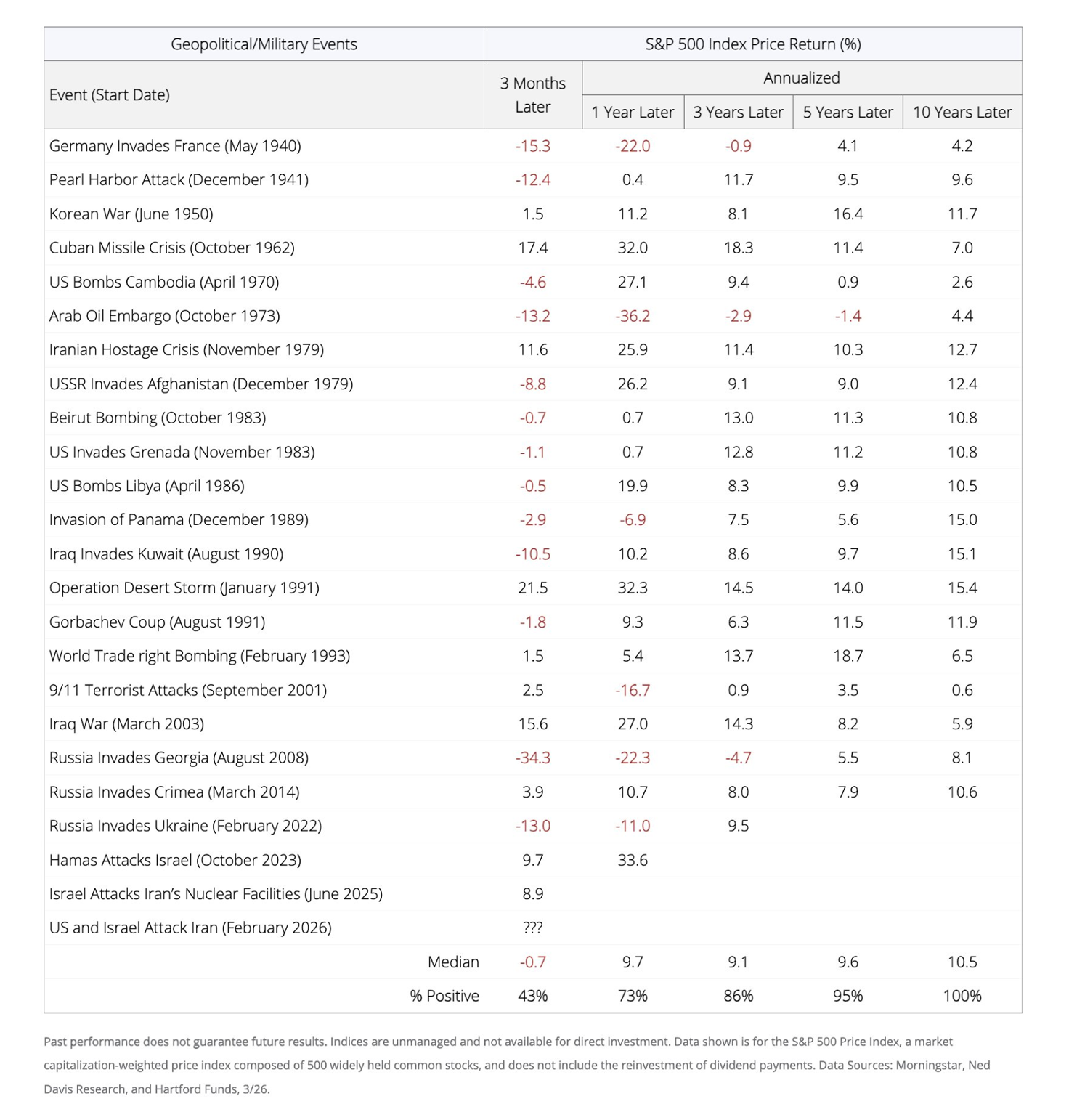

According to Harford Funds, equities generated positive performance 12 months after an act of aggression for 73% of the armed conflicts since World War II:

Bottom Line

* Though P/E ratios remain elevated — investor sentiment has soured, positioning is defensive and many of our concerns are being realized

* Uncertainty remains present and a strong conviction (either way) does not yet seem appropriate

* Given the plethora of multiple challenges and headwinds — that have only recently been acknowledged by many investors — I expect a longer bottoming process than in the past... so the customary "V" market bottoms (made over the last three years) seem unlikely

* We are applying "second-level thinking" today and with many stocks -25% or more, a modestly net long exposure now seems appropriate (a shift from our long standing and slightly net short exposure)

* It is increasingly possible that I will be "returning to the land of the living" by sensibly and gradually expanding my long exposure in the weeks and months ahead

* The S&P Index is down by about -4% year to date — I continue to expect a high-single-digit negative to low-double-digit negative return for the year

* Over the balance of the year (as was the case in January-March), stock picking will be crucial and, when done well, value-added to portfolios

* Always remember: short selling protects capital, long buying creates capital

I have always written that being short protects capital and being long creates capital.

For some time, I have operated defensively at my hedge fund.

Let me make it clear that I am in no rush to buy stocks. But I do plan to move slowly away from defense and towards more offense as sentiment has eroded, positioning has moved far more conservative and many of our concerns are now being acknowledged ("second-level thinking").

Importantly, the war in Iran has rapidly transformed investor optimism to investor pessimism as sentiment and stock prices have fallen.

Coincident with lower stock prices, investors are beginning to acknowledge our fundamental concerns and some investment opportunities have now emerged.

Warren Buffett emphasized that investing requires rational, cold, "no-emotion" decision making, rather than reacting to market fear or greed, to achieve long-term success in the quote below:

"Until you can manage your emotions, don't expect to manage money."

So, as always, I will approach emerging long opportunities dispassionately and with a calculator in hand — calculating upside reward vs. downside risk while adopting the "margin of safety" principle in all of our buys.

Related: 6 Charts Show We Could Be in for a Rude Energy Price Awakening

This commentary was originally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.